The group financial controller of a mid-sized UK manufacturer laid out the problem simply. His group had four legal entities — a UK holding company, two manufacturing subsidiaries (one in the UK, one in Germany), and a UK distribution company. The factories sold finished goods to the distribution entity at transfer prices, and the distribution entity sold to customers. Every month, he spent three days building the group consolidation in Excel: adjusting the intercompany sales, eliminating the unrealised profit on stock that sat in the distribution company’s warehouse at month-end, translating the German entity’s euro financials into sterling, and reconciling the whole thing back to a consolidated P&L that the board could rely on.

Manufacturing groups create some of the more demanding consolidation scenarios in practice. The combination of intercompany goods transfers, transfer pricing, multi-currency overseas factories, and often misaligned chart of accounts between sites means that financial consolidation for manufacturing groups demands a more systematic approach than a spreadsheet can reliably provide.

This guide explains why, works through a realistic example, and covers what to look for in group reporting software built to handle it.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

Why Manufacturing Group Structures Create Consolidation Complexity

A single manufacturing entity is straightforward. The consolidation challenge grows in proportion to the number of entities, currencies, and intercompany flows. Manufacturing groups typically include:

- A parent or holding company that may hold IP, provide financing, or act purely as a treasury and governance entity

- One or more manufacturing subsidiaries — often in different jurisdictions, with different functional currencies, running on accounting systems chosen locally

- A distribution or sales entity that purchases finished goods from the factories and sells to end customers

- Potentially an IP holding entity that licences brand, patent, or process IP to the manufacturing subsidiaries

Each of these creates intercompany transactions that are real within individual entity accounts but must be eliminated at group level. The more entities, the more flows — and the more opportunities for errors to compound across months.

The Four Biggest Consolidation Headaches in Manufacturing

1. Intercompany Goods Transfers and Unrealised Profit

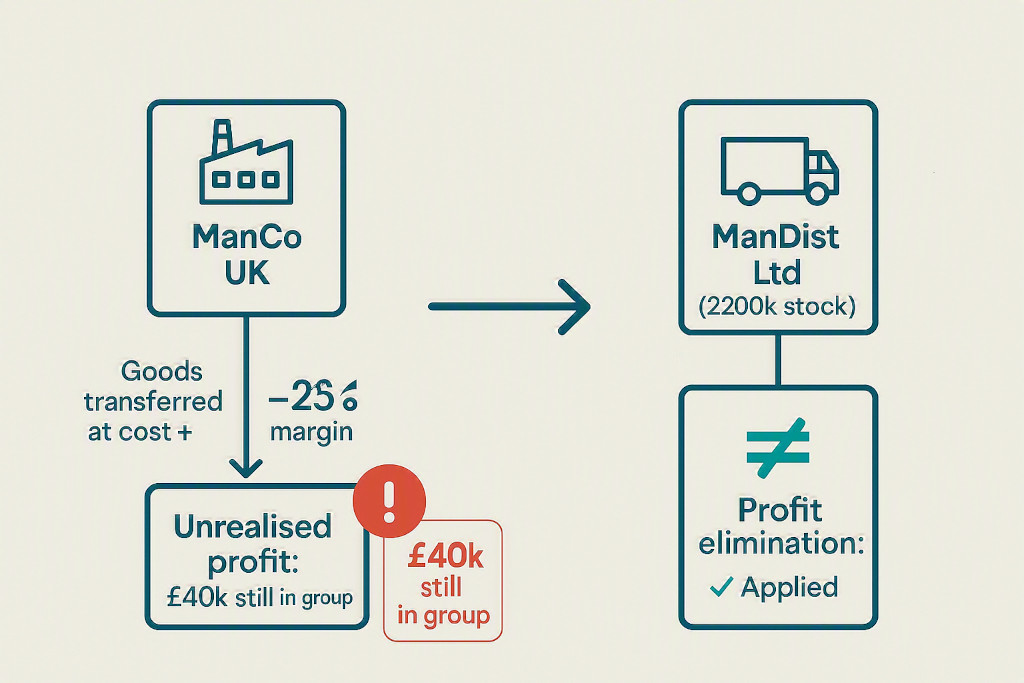

When one entity within a manufacturing group sells goods to another — the factory sells to the distribution company, for example — those goods are recorded as revenue in the factory’s accounts and as a cost (and eventually inventory) in the distribution company’s accounts. At the group level, neither the revenue nor the cost should exist: it is an internal transaction.

The complication arises when the selling entity has added a margin to the transfer price. If ManCo UK transfers goods to ManDist Ltd at cost plus 25%, and ManDist still holds some of those goods in inventory at the month-end reporting date, the group balance sheet includes inventory valued at the inflated transfer price rather than the group’s actual cost. The margin embedded in the unsold stock — the unrealised profit — must be eliminated from both inventory and group profit. This is one of the most commonly missed adjustments in manual consolidations.

For a broader grounding in how intercompany eliminations work across different transaction types, the guide on intercompany eliminations for multi-entity groups covers the underlying principles and journal entries in detail.

2. Transfer Pricing Consistency

The price at which one entity within the group sells to another has both accounting and tax implications. For consolidation purposes, any margin included in the transfer price creates an intercompany profit that must be tracked and eliminated. When transfer prices are set inconsistently — or change between periods — the elimination calculation becomes considerably more complicated.

3. Fixed Asset Transfers Between Entities

Manufacturing groups occasionally move plant, equipment, or tooling between entities. When one entity sells an asset to another at a gain, that gain is unrealised from the group’s perspective and must be eliminated, with depreciation adjustments applied going forward. This is another adjustment that is straightforward in principle but easy to overlook in a busy month-end close.

4. Mixed Accounting Systems Across Sites

Manufacturing subsidiaries often run on accounting platforms chosen for their local market or historical preference. A UK factory might use Xero or QuickBooks. A continental European subsidiary is more likely to run on a locally preferred platform. The UK distribution entity might use MYOB or Zoho Books. Consolidating across platforms without a dedicated tool means exporting trial balances from each, reformatting them, and mapping across different charts of accounts before the consolidation even begins. The guide on designing a common chart of accounts for multi-entity groups covers the practical approach to standardising account structures across disparate entities.

A Practical Example: Consolidating a Four-Entity Manufacturing Group

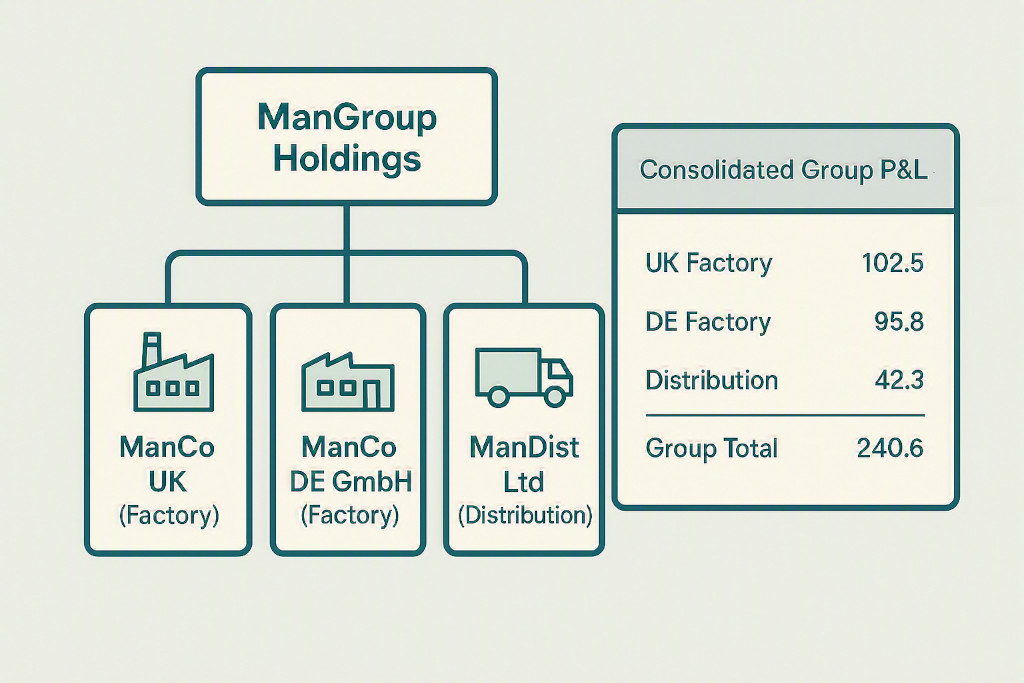

Consider ManGroup Holdings Ltd, a UK-based manufacturing group with the following structure:

| Entity | Country | Functional Currency | Role | Annual Revenue |

|---|---|---|---|---|

| ManGroup Holdings Ltd | UK | GBP | Holding company | — |

| ManCo UK Ltd | UK | GBP | UK manufacturing | £6.4m (to group) |

| ManCo DE GmbH | Germany | EUR | European manufacturing | €3.2m (to group) |

| ManDist Ltd | UK | GBP | UK distribution & sales | £11.8m (to customers) |

The group’s key intercompany flows each month are:

- ManCo UK Ltd sells finished goods to ManDist Ltd at cost plus 25% margin — approximately £533k per month (£6.4m per annum)

- ManCo DE GmbH sells components to ManDist Ltd at cost plus 20% margin — approximately €267k per month (€3.2m per annum), invoiced in EUR and translated to GBP

- ManGroup Holdings Ltd charges a management services fee of £15,000 per month to ManCo UK Ltd

At the April month-end close, ManDist Ltd holds £800,000 of inventory purchased from ManCo UK during the month. Of that, the intercompany margin element is £160,000 (£800k × 25% ÷ 125%). That £160,000 of unrealised profit must be eliminated from both the group P&L and the group inventory balance on the consolidated balance sheet.

“Every month, the unrealised profit calculation changes depending on how much stock ManDist is holding at the close date. In a good month you might eliminate £120k. In a high-stock month it could be £250k. Getting that figure wrong by even £50k moves the group gross margin by nearly half a percentage point.”

Eliminating Unrealised Profit on Intercompany Inventory

The elimination journal for the ManCo UK / ManDist scenario looks like this at group level:

Elimination — Unrealised profit in ManDist inventory (April)

Dr Cost of Sales £160,000

Cr Inventory (ManDist balance sheet) £160,000

Being: elimination of unrealised profit on intercompany goods held in ManDist inventory at period end

This journal reverses next month (since the opening stock position is unwound) and is recalculated based on the closing stock balance each period. When this is tracked manually in a spreadsheet, a missed update or incorrect stock figure can flow silently into the consolidated accounts for months before someone notices.

The broader challenge of staying on top of intercompany reconciliations at month-end is covered in detail in the post on why multi-entity groups lose days to manual reconciliation — and what the alternative looks like.

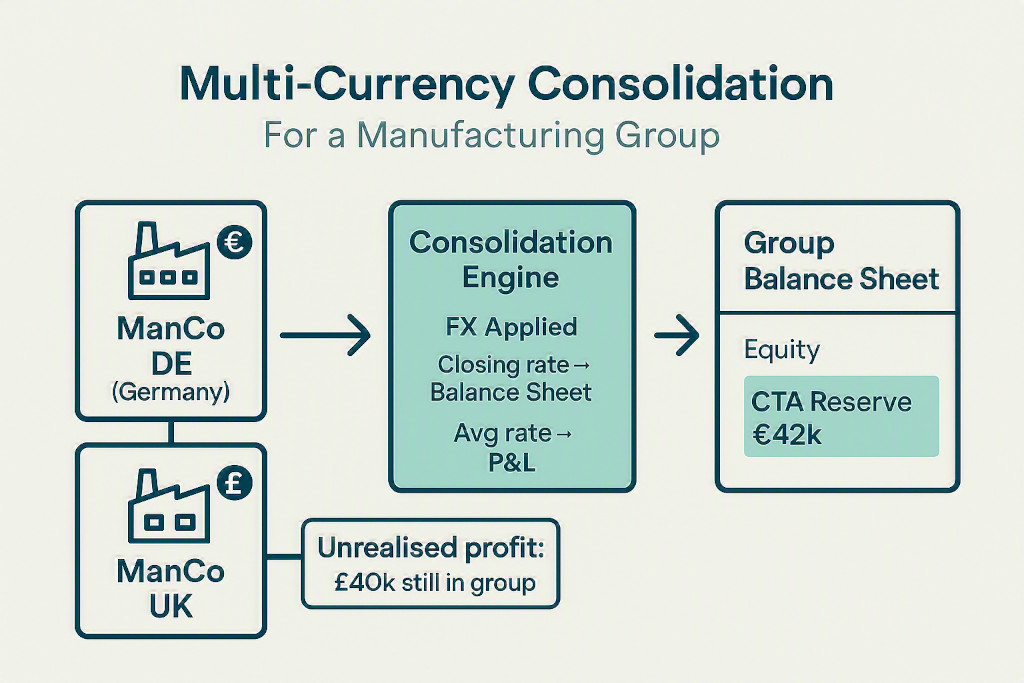

Currency Translation for International Manufacturing Entities

ManCo DE GmbH presents the group with a EUR functional currency entity whose financials must be translated into GBP for group consolidation. The rules under IAS 21 (or ASC 830 for US GAAP groups) are straightforward in principle:

- Balance sheet items translate at the closing rate on the last day of the reporting period

- P&L items translate at the average exchange rate for the period

- The difference between translating assets and liabilities at the closing rate versus the rate at which equity was originally recorded accumulates as the cumulative translation adjustment (CTA) in group equity

For ManGroup, with a EUR/GBP closing rate of 0.856 and an average rate of 0.851 for April, the translation difference on ManCo DE’s net assets produces a CTA movement of approximately £42,000 for the month. That figure grows or shrinks with exchange rate movements and must be tracked cumulatively. If the group later disposes of ManCo DE, the cumulative CTA is recycled through the group P&L at that point — which makes accuracy over time particularly important.

In a spreadsheet, applying the correct rates consistently every month, adjusting for prior-period corrections, and ensuring the CTA reconciles to the group equity section is a significant manual burden. In a consolidation tool with built-in FX handling, it runs automatically once the rates are entered for the period.

How BrizoConsol Handles Financial Consolidation for Manufacturing Groups

BrizoConsol connects directly to Xero, QuickBooks, MYOB and Zoho Books via API — no CSV exports, no manual data re-entry. For a group like ManGroup Holdings, live trial balance data flows from all entities into a single consolidation environment, updated as the books are maintained.

Key capabilities for manufacturing groups:

- Automatic intercompany eliminations. Define the intercompany relationships once — the ManCo UK to ManDist goods flow, the management fee from the holding company — and BrizoConsol eliminates them at every close. For unrealised profit on inventory, the elimination is driven by the intercompany margin rate and the closing stock balance.

- Multi-currency with automatic CTA. Set the closing and average FX rates for each period, and BrizoConsol applies the correct translation to ManCo DE GmbH’s accounts, producing the CTA reserve in group equity without a separate manual step.

- Consolidated P&L, Balance Sheet and Cash Flow on demand. The group controller can pull a consolidated view at any point in the close, not just at the end — enabling early visibility of where the numbers are heading.

- Virtual Groups for segment reporting. A manufacturing group that wants to report UK production versus European production separately, or to see the distribution entity’s contribution in isolation, can create virtual reporting groups without additional legal entity structures.

- AI Auto-Map for chart of accounts differences. When ManCo DE GmbH uses a German chart of accounts (SKR03, for example), BrizoConsol’s AI Auto-Map normalises account mappings to the group’s standard structure automatically.

- Full audit trail on all consolidation adjustments. Every elimination, currency adjustment, and journal entry is logged, making the group close defensible to auditors and straightforward to review internally.

What to Look for in Consolidation Software for a Manufacturing Group

Manufacturing groups evaluating multi-entity accounting software should prioritise the following:

- Native API connections to your accounting platforms. Manufacturing subsidiaries often run on different systems. A tool that requires manual CSV exports between platforms introduces both a data lag and a human error point at the most critical stage of the close.

- Intercompany elimination with unrealised profit handling. Not all consolidation tools support elimination of unrealised profit on intercompany inventory. This is non-negotiable for any manufacturing group where entities sell goods to each other.

- Multi-currency with automated CTA calculation. Any group with an overseas entity needs a tool that applies the correct translation method and accumulates the CTA correctly under IAS 21 or ASC 830.

- Flexible chart of accounts mapping. Manufacturing subsidiaries in different countries frequently use locally preferred account structures. Look for tools with intelligent mapping that normalises these into the group standard without requiring all entities to change their local setup.

- Segment reporting by factory, product line, or geography. Manufacturing groups typically need more granular visibility than a single group P&L provides. Virtual group functionality — where you define reporting segments independently of legal entity structure — is particularly valuable.

- IFRS, US GAAP and UK GAAP support. Groups with both UK and overseas statutory reporting requirements may need to tag accounts against different standards for local versus group purposes.

Financial consolidation for manufacturing groups is not inherently more difficult than consolidation in any other multi-entity structure — but the specific combination of intercompany goods flows, unrealised profit on inventory, multi-currency overseas subsidiaries, and mixed accounting platforms means that a spreadsheet-based approach carries compounding risk at every close. A purpose-built group consolidation tool handles each of these automatically, and turns a multi-day month-end exercise into something the finance team can run — and trust — in hours.

See How BrizoConsol Handles Manufacturing Group Consolidation

Connect your entities across Xero, QuickBooks, MYOB and Zoho Books, set up intercompany eliminations including unrealised inventory profit, and produce a consolidated group P&L — without the spreadsheet. Start Free Trial