If you manage the finances of a group with two or more entities, you already know the frustration. Each subsidiary runs its own accounting software, and each one was set up independently, often at different times, by different accountants, with different naming conventions and account structures. One entity codes rent as “Office Lease Expense.” Another calls it “Occupancy Costs.” A third splits it across three separate accounts. None of them match. And every month, when you try to pull together a consolidated view of the group, your finance team spends hours manually mapping, reconciling, and cross-referencing accounts before a single meaningful number can appear in a report. This is not an edge case. It is the default reality for most growing multi-entity businesses, and it is entirely solvable. The solution is a Common Chart of Accounts, or CCOA: a shared account structure that sits above your individual entity charts and gives every entity in your group a common financial language. When designed well, a CCOA transforms consolidation from a manual, error-prone ordeal into a streamlined, repeatable process. This guide walks you through exactly how to design one, from the first principles through to practical implementation.

What Is a Common Chart of Accounts and Why Does It Matter

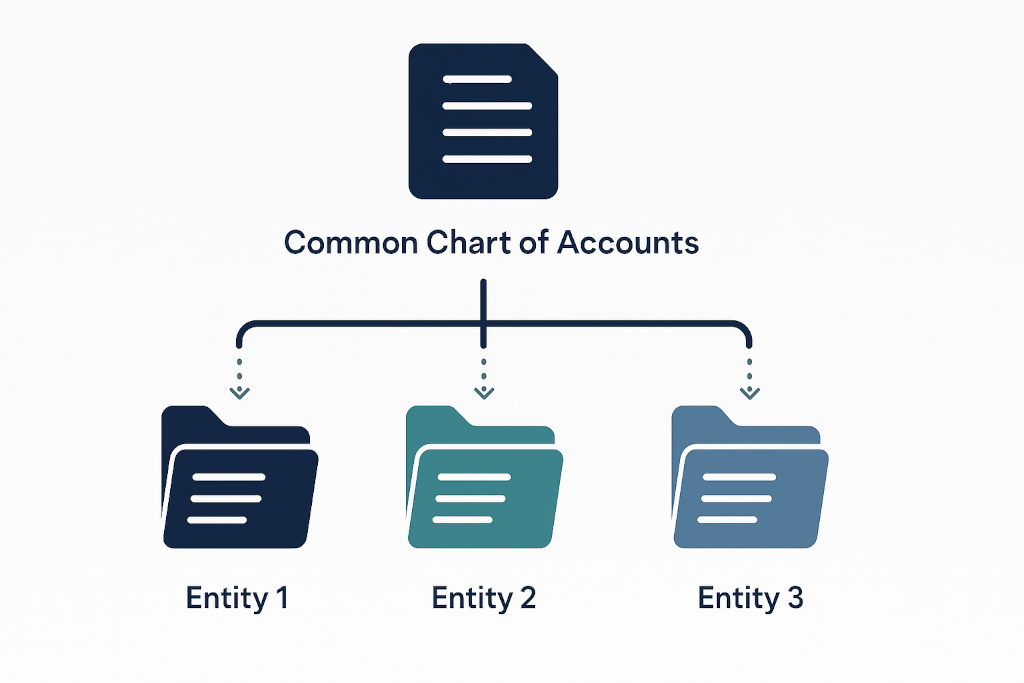

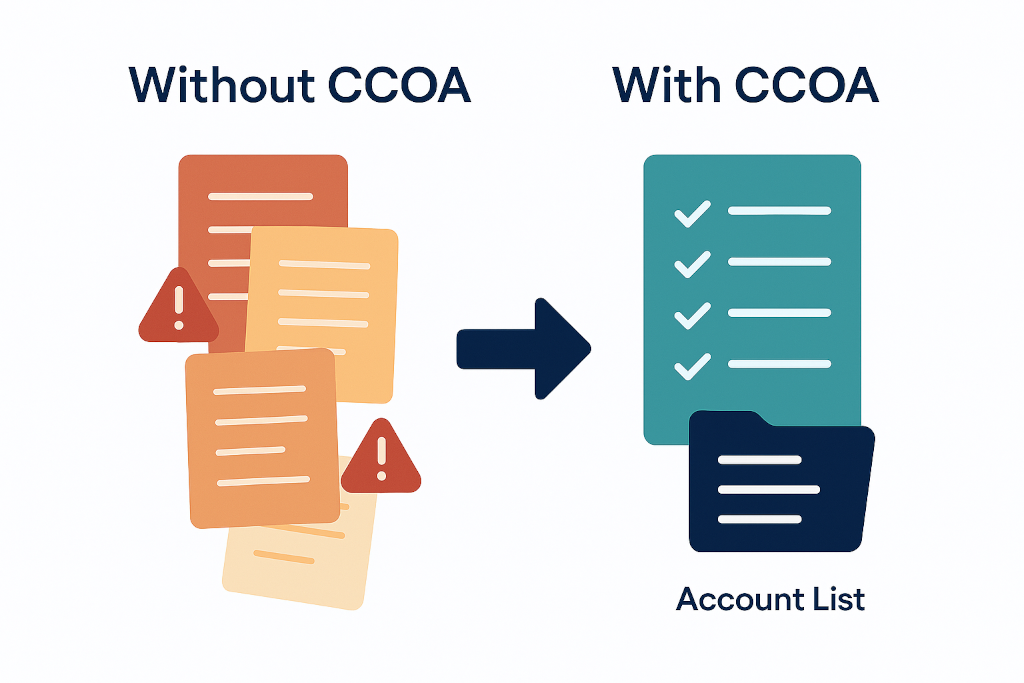

A Common Chart of Accounts is a standardised set of account categories and codes that is applied consistently across all entities in a group, regardless of what accounting software each entity uses or how its local chart of accounts is structured. It is not a replacement for the local chart of accounts that each entity uses for day-to-day bookkeeping. Instead, it sits above those local charts as a mapping layer. Each local account is linked to a corresponding CCOA account, and when financial data is pulled into your consolidation process, it is translated into the common structure automatically. The reason this matters so much is that consolidation is fundamentally a comparison and aggregation exercise. To add two numbers together, they need to represent the same thing. If Entity A and Entity B both have revenue, but one codes it as account 4000 and the other as a mix of accounts 5100, 5200, and 5300, you cannot simply sum them. You need a mapping that says: here is what revenue means across the whole group, and here is how every entity’s local revenue accounts roll up to that definition. Without a CCOA, that mapping has to be rebuilt manually every reporting period, which is slow, inconsistent, and highly prone to error. With a CCOA in place, the mapping is done once, validated, and reused automatically every single month. Reporting becomes faster. Consolidations become more reliable. And your finance team gets to focus on analysis rather than data wrangling.

Step 1: Audit What You Already Have

Before you can design a CCOA, you need to understand the raw material you are working with. Start by exporting the full chart of accounts from every entity in your group. For each entity, note the total number of accounts, the account numbering convention used, the categories and subcategories in use, and any accounts that appear to be duplicates or that are rarely used. At this stage you are not trying to fix anything. You are simply mapping the terrain. What you will almost certainly find is that there is significant variation across your entities, even if they are in the same industry and use the same accounting software. Different bookkeepers make different choices. Different accountants set things up differently. And over time, entities accumulate accounts that were created for specific transactions and then never cleaned up. A typical multi-entity group might find that two entities have 150 accounts each, but only 60 of those accounts are genuinely distinct categories when you strip away the naming differences. The audit phase surfaces this clearly. It also helps you identify which entities have the most complex or idiosyncratic account structures, because those are the ones that will require the most thought when you get to the mapping stage. Document everything in a spreadsheet. You want columns for entity name, account code, account name, account type (asset, liability, equity, income, expense), and any notes about how the account is used. This audit document will become the foundation for everything that follows.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

Step 2: Define Your CCOA Structure and Numbering Convention

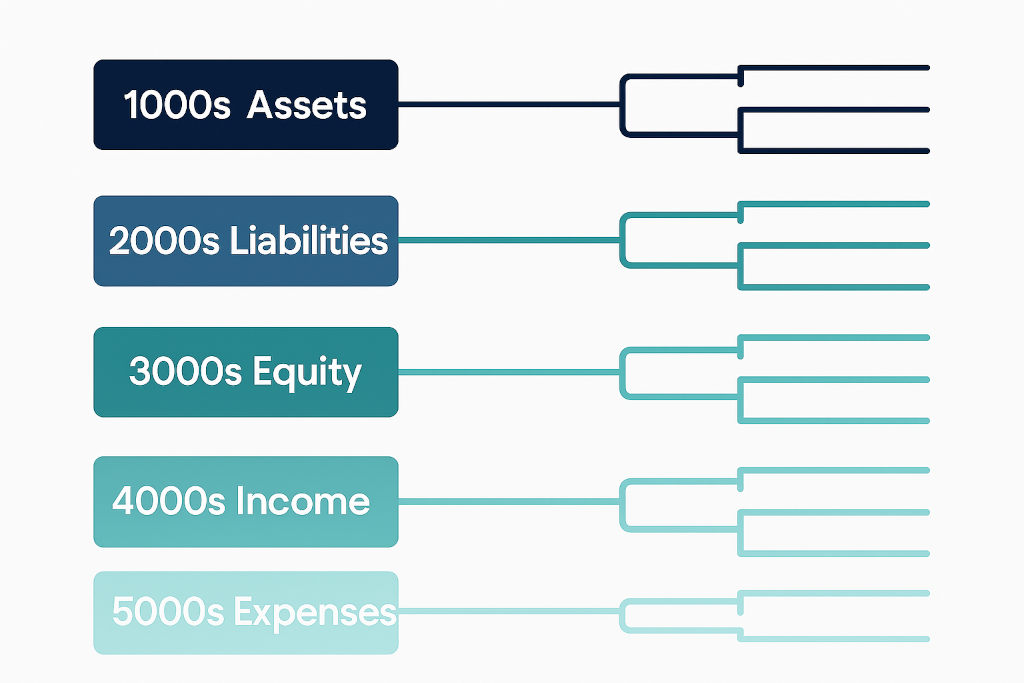

With your audit complete, you can start designing the CCOA itself. The goal is a structure that is detailed enough to give you meaningful reporting, but not so granular that it becomes difficult to maintain. Most well-designed CCOAs for mid-sized groups have between 80 and 150 accounts. Anything significantly more than that tends to create mapping complexity without adding proportional reporting value. Start with the five fundamental account types: assets, liabilities, equity, income, and expenses. Within each type, work from the broadest categories down to the level of detail you genuinely need in your consolidated reports. For income, for example, you might have Product Revenue, Service Revenue, Other Operating Income, and Interest Income as your top-level categories. If you need to report product revenue by region or product line, you can add subcategories. But keep asking: do we actually need this level of detail in our group reports, or is this only relevant at the entity level? Your numbering convention matters too. A widely used approach is a four or five digit numbering system where the first digit indicates the account type: 1000s for assets, 2000s for liabilities, 3000s for equity, 4000s for income, and 5000s onwards for expenses. Within each block, leave gaps in the numbering so that new accounts can be inserted later without disrupting the overall structure. For example, if Revenue from Products is 4100 and Revenue from Services is 4200, you have room to add 4150 for a new revenue category in future without renumbering everything. Document the purpose of each CCOA account clearly. Every account should have a plain-English description of what belongs in it and, equally important, what does not. This documentation becomes the reference guide for bookkeepers and accountants across all your entities when they are doing the local-to-CCOA mapping.

Step 3: Map Each Entity’s Local Accounts to the CCOA

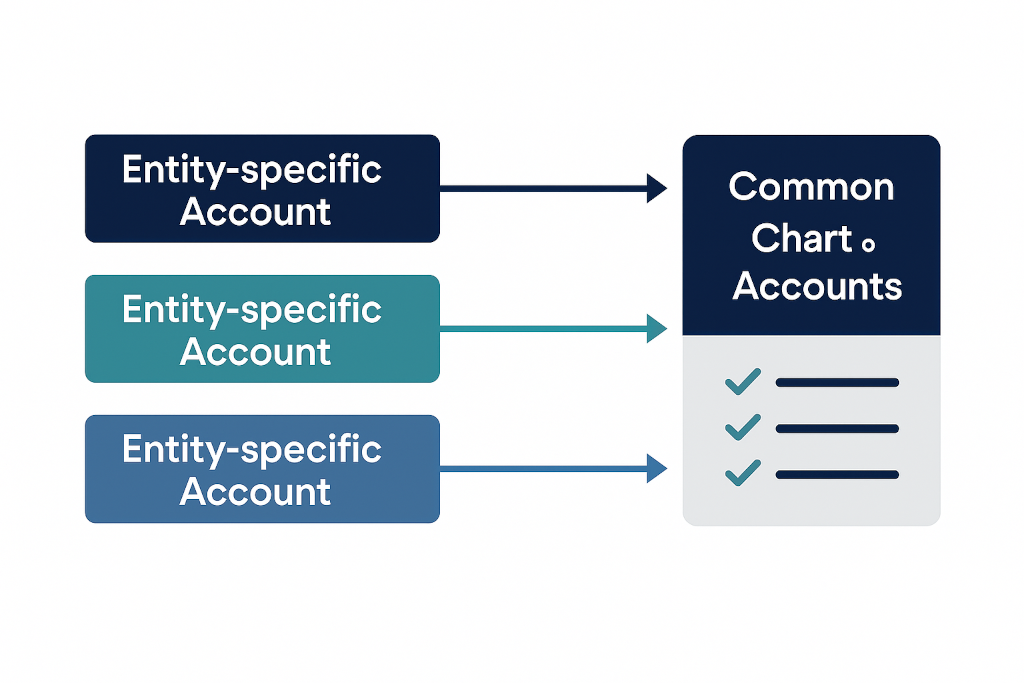

With the CCOA designed, the next step is mapping. For every local account in every entity, you need to define which CCOA account it maps to. This is often the most time-consuming part of the process the first time around, but it is a one-time investment that pays dividends for years. Work through each entity systematically. For most accounts, the mapping is straightforward: local account “Salaries and Wages” maps to CCOA account “Employee Costs.” For others, you will need to make judgement calls. An account called “Marketing and Entertainment” might need to be split across two CCOA accounts if the amounts are material, or mapped to whichever category is more relevant. Record all of these decisions, because they will need to be applied consistently going forward and may need to be explained to auditors. Pay particular attention to accounts that exist in some entities but not others. If one entity has an “R and D Expense” account because it runs a product development function, you need a CCOA account for that even if no other entity uses it. The CCOA must be comprehensive enough to accommodate all the entities in your group, including any you plan to add in future. Also think carefully about intercompany accounts. Many of the eliminations you will perform at the consolidation stage depend on intercompany balances being clearly identified. Consider creating dedicated CCOA accounts for intercompany receivables, intercompany payables, intercompany revenue, and intercompany expenses. This makes the elimination process much cleaner and reduces the risk of items being missed.

Step 4: Validate with a Test Consolidation

Before rolling out your CCOA to the whole group, run a test consolidation using historical data. Take the last three to six months of data from all entities, apply your CCOA mappings, and produce a consolidated trial balance. Then sense-check it against what you know. Does the total revenue look right? Do the intercompany balances net to zero before eliminations? Does the consolidated balance sheet balance? Does the expense breakdown reflect the actual cost structure of the business? If something looks wrong, trace it back. Either there is a mapping error (a local account has been assigned to the wrong CCOA category), or there is a data quality issue in one of the entity trial balances, or there is a gap in your CCOA that needs to be filled. This validation step is invaluable precisely because it happens before you go live. Catching a mapping error on historical data is a ten-minute fix. Catching it six months into production use, when it has affected multiple reporting periods and been presented to your board, is a much bigger problem. Run the test consolidation at least twice, once with the initial mapping and once after any corrections you identified in the first run. Only when you can produce a consolidated trial balance that makes sense and that you can stand behind should you consider the CCOA ready for production use.

Step 5: Govern and Maintain the CCOA Over Time

A CCOA is not a set-and-forget exercise. Businesses change. New revenue streams emerge. New entities are acquired. Regulations change the way certain transactions must be reported. Your CCOA needs to evolve alongside the business, and that evolution needs to be governed carefully. Appoint a single person or team as the owner of the CCOA. That person is responsible for reviewing any requests to add, modify, or retire CCOA accounts, ensuring that changes are documented and communicated to all entities, and updating the mapping for any entities affected by a change. Without a clear owner, the CCOA tends to drift over time as different people make informal changes that are not communicated across the group, and eventually you are back to the inconsistency you started with. Establish a process for handling new local accounts. When a bookkeeper at one of your entities creates a new account in their local chart, there should be a clear step that asks: which CCOA account does this map to? If no existing CCOA account is appropriate, the CCOA owner should be notified so a decision can be made. This does not need to be bureaucratic. A simple form or shared document can handle it. The key is that the mapping is always kept up to date so that consolidations never produce surprises. Review the CCOA in full at least once a year. Ask whether the level of detail still reflects what the business needs from its group reports. Accounts that were once relevant may now be immaterial. New reporting requirements may make new categories necessary. An annual review keeps the CCOA lean and purposeful.

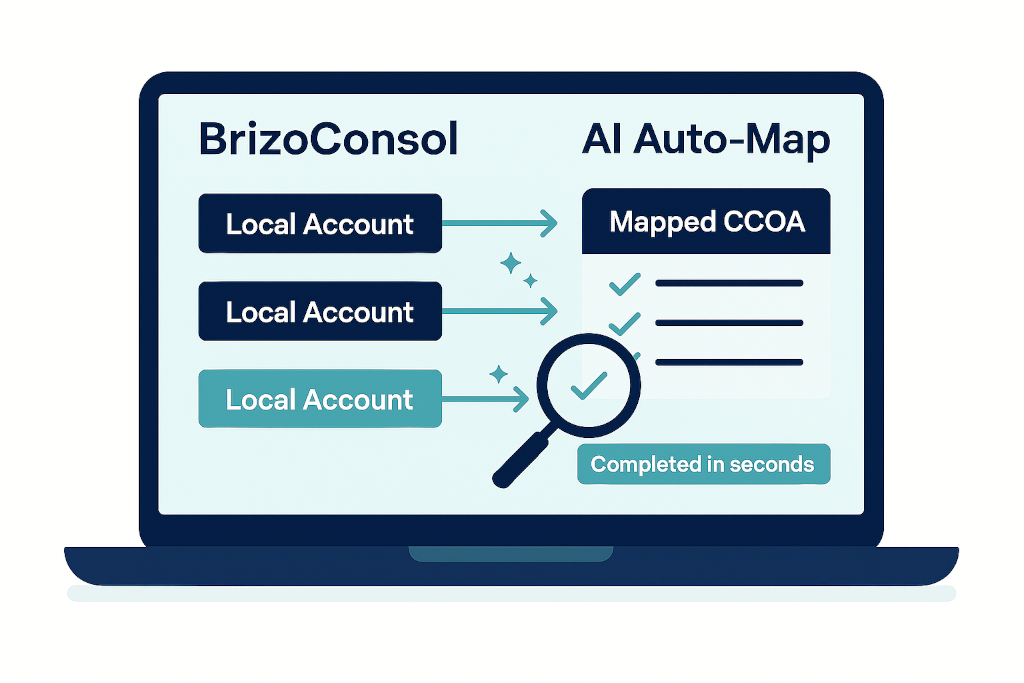

How BrizoConsol Makes the CCOA Process Faster and More Reliable

All of the steps described above are achievable with manual effort and a well-organised spreadsheet. But if you are managing a group of three or more entities, or if your entities report in multiple currencies, or if you are adding new entities regularly through acquisition or organic growth, the manual approach quickly becomes a bottleneck. BrizoConsol is built to handle exactly this. When you connect your entities to BrizoConsol, the platform’s AI Auto-Map feature analyses your local charts of accounts and suggests mappings to a common structure automatically. What would take a finance team days of careful, manual work is done in minutes, with the suggested mappings presented for your review and approval rather than applied blindly. You retain full control while the heavy lifting is handled for you. Once your mappings are in place, they are stored and applied automatically every time data is updated. There is no need to re-do the mapping each month. When a new entity joins the group, its local chart is mapped once and then it flows into the consolidated reports seamlessly. BrizoConsol also handles the intercompany elimination process that depends so heavily on a well-structured CCOA, automatically identifying intercompany balances and eliminating them in the consolidation, with a full audit trail so you can see exactly what was eliminated and why. For groups that report in multiple currencies, BrizoConsol applies the correct translation method for each account type and currency, producing consolidated financials that are both accurate and easy to review. The result is a consolidation process that is faster, more reliable, and far less dependent on manual effort than anything you can achieve with a spreadsheet-based approach.

Conclusion: Build the Foundation Once, Benefit Every Month

A well-designed Common Chart of Accounts is one of the highest-leverage investments a multi-entity finance team can make. The work happens once: auditing your existing charts, designing the common structure, building the mappings, validating with historical data, and setting up the governance process. But once that foundation is in place, every single consolidation cycle benefits from it. Reports are produced faster. Numbers are more reliable. Auditors have a cleaner, more consistent dataset to review. And your finance team spends less time on manual reconciliation and more time on the analysis and insight that actually drives business decisions. If your group is still running consolidations without a CCOA, or if you have a CCOA that was set up informally and has drifted over time, this is the moment to address it. Start with the audit. Take stock of what you have. Then design a structure that reflects how your business actually needs to be reported at the group level. The effort is front-loaded, but the payoff compounds every month from the moment it goes live.