Sarah is the group controller for a nine-entity professional services firm. On the last working day of each month, she and a junior accountant open a shared spreadsheet labelled “Month-End Journals — DO NOT EDIT.” Over the next two and a half days, they post 58 manual journals across Xero, QuickBooks and MYOB: intercompany loan interest, management fee charges, dividend eliminations, and a handful of reclassification entries that never quite make it into the right account first time. They have been doing this for three years. Last October, one journal was posted to the wrong entity. The error surfaced in the audit six months later.

Sarah’s situation is not unusual. For most multi-entity groups, automated intercompany journals remain an aspiration rather than a reality — even as every other part of the accounting function becomes more automated. This article explains why, walks through what journal automation actually involves at consolidation, and sets out what to look for in software that solves the problem properly.

Why Manual Journal Entry Is Still the Default at Month-End Close

The persistence of manual journals in group accounting is not a technology gap — the tools exist. It is a workflow problem. Most multi-entity groups use different accounting platforms for different subsidiaries. When the platforms are not directly connected to a consolidation layer, there is no mechanism for an intercompany transaction posted in one ledger to automatically generate the corresponding elimination entry in another. The accountant fills the gap manually.

This pattern becomes entrenched quickly. Once a manual process has been running for twelve months, it has a year of custom logic embedded in it: rounding conventions, posting order, account code quirks in each ledger, sub-entities that are handled differently for historical reasons. The prospect of replacing that with automation feels risky. The manual process continues.

The problem scales with the group. A three-entity group might manage with 12 monthly journals. A nine-entity group with multiple intercompany relationships generates 50 or more — each one a potential source of error, each one requiring reconciliation before the consolidated accounts can close. Understanding what financial consolidation software does is the first step toward recognising where that automation gap lives and what it costs.

The Four Journal Types That Consume Group Close

Not all intercompany journals carry the same risk profile. The four categories below account for the majority of manual month-end journal work in a typical group.

Intercompany loan interest and balance eliminations

Where entities lend to or borrow from each other, the loan balance, accrued interest income, and corresponding interest expense must all be eliminated in the consolidated accounts. A mismatch between the lender’s receivable and the borrower’s payable — common where entries are posted independently — will cause the consolidated balance sheet to fail to balance. These mismatches are among the most common errors found in group audit fieldwork.

Management fee charges

A holding company that charges management fees to operating subsidiaries must ensure that the fee income in the holding company and the fee expense in each subsidiary are eliminated on consolidation. If the holding company posts the fee in one period and the subsidiary accrues it in another, the elimination will not net to zero and the consolidated P&L will carry a residual balance.

Dividend eliminations

Dividends paid by a subsidiary to a parent must be eliminated from the consolidated income statement and equity movement. Where NCI (non-controlling interest) exists, the portion of the dividend attributable to minority shareholders must be calculated separately. Both the elimination and the NCI allocation require precise journal entries that reference the exact ownership percentages at the date of declaration.

Reclassification and reclass journals

Subsidiary ledgers frequently use account codes that do not map neatly to the group chart of accounts — particularly where acquisitions have brought in entities with different accounting platforms or historical conventions. Reclassification journals adjust the subsidiary trial balance to conform with group reporting requirements before consolidation runs. Without automation, these journals are recreated from scratch each month.

What Automated Intercompany Journals Actually Look Like

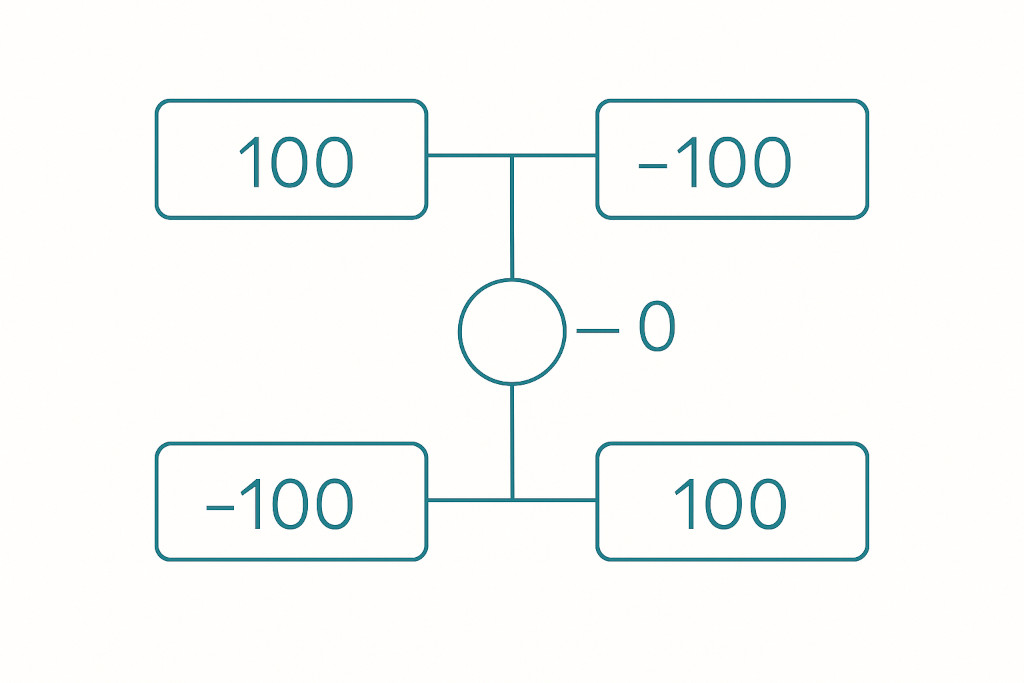

Automation does not mean the journals disappear. It means they are generated, matched, and posted by the system rather than by a human. Here is what that looks like in practice for a group with a management fee arrangement.

Scenario: Holdco charges a £20,000 monthly management fee to OpCo. Holdco posts the fee income to its Xero ledger. OpCo posts the corresponding expense to its QuickBooks ledger. At consolidation, both entries must be eliminated.

| Entity | Account | Dr / Cr | Amount (£) |

|---|---|---|---|

| Holdco | Management fee income | Dr (Eliminate) | 20,000 |

| OpCo | Management fee expense | Cr (Eliminate) | 20,000 |

Elimination journal generated automatically by BrizoConsol from the matched intercompany transaction pair.

In a manual process, an accountant identifies the matching transactions, calculates the elimination, posts the journal, then reconciles to confirm the net consolidated balance is zero. In an automated process, the consolidation platform identifies the intercompany pair, generates the elimination journal, posts it, and flags any unmatched balances for review — all without human intervention.

The same logic applies to intercompany loans: the consolidation engine reads the loan balance from the lender’s ledger, matches it against the borrower’s liability, and generates the elimination and any accrued interest journals automatically. For a detailed breakdown of how these entries work across different transaction types, see our practical guide to intercompany eliminations.

The Risk of Getting Intercompany Journals Wrong

Audit risk alert: Intercompany mismatches are one of the top five findings in group audit fieldwork. A single unreconciled intercompany balance can require restatement of prior-period consolidated accounts if it is material.

Manual journals introduce three categories of risk that automated intercompany journals eliminate.

Timing mismatches. Where one entity posts its side of an intercompany transaction in a different period from its counterparty, the mismatch creates a spurious balance in the consolidated accounts. These timing differences are easy to miss in a large group and notoriously difficult to untangle retrospectively.

Version control failures. Manual journal processes typically involve shared spreadsheets. When two accountants post journals from different versions of the same workbook, duplicate or contradictory entries result. The discovery usually happens during the close, when the consolidated trial balance fails to reconcile.

No audit trail. A journal posted manually in a subsidiary ledger carries the posting accountant’s name and date. The logic behind the journal — why this amount, which intercompany transaction it corresponds to, who approved it — lives in the accountant’s memory or in an email thread. When an auditor asks, neither is satisfactory.

“Every manual journal is a decision made under time pressure. Automate the decision — keep the review. That is what good consolidation software gives you: the judgment stays with the accountant, the mechanical work moves to the machine.”

How BrizoConsol Automates the Journal Cycle

BrizoConsol connects directly to Xero, QuickBooks, MYOB and Zoho Books via live API — no CSV exports, no manual data pulls. This live connection is the foundation that makes journal automation possible. Because the consolidation engine has real-time access to every entity’s trial balance, it can identify intercompany pairs, calculate eliminations, and generate the required journals without waiting for an accountant to intervene.

The key capabilities for multi-entity journal automation include:

- Automatic intercompany matching — the platform scans every entity’s receivables and payables, matches intercompany pairs, and flags unmatched balances before the close runs.

- Elimination journal generation — matched pairs generate elimination journals automatically, with the amounts, accounts, and entities pre-populated from the source ledger data.

- AI Auto-Map for chart of accounts — where entities use different account codes, the AI mapping engine aligns them to a common group chart of accounts, reducing reclassification journals to a first-time setup task rather than a monthly burden.

- Full audit trail — every consolidation adjustment, elimination, and journal entry is logged with a timestamp, source transaction reference, and the logic that generated it.

- Multi-currency journals — where intercompany transactions cross currencies, the platform applies the correct exchange rates and generates the corresponding CTA entries automatically.

For groups already using BrizoConsol for consolidation, the journal automation is part of the same workflow — not a separate module. You can see how this fits into the broader close process in our overview of how consolidation software cuts month-end close time for multi-entity groups.

What to Look For in Journal Automation Software

Not all consolidation platforms handle journal automation at the same depth. When evaluating options for multi-entity journal automation, these are the questions that separate a genuine solution from a reporting tool with a consolidation toggle:

| Capability | Why it matters |

|---|---|

| Direct API to all source ledgers | Automation breaks down if data must be exported and re-imported manually. All your entities’ ledgers — whatever platform they run on — need to be connected live. |

| Intercompany matching engine | The platform should identify counterparty pairs automatically, not require you to map them manually in a setup spreadsheet. |

| Audit trail on every adjustment | Your auditors will ask for the source of each elimination journal. The platform must provide a full log, not just a summary. |

| Multi-currency support | Groups with foreign subsidiaries need currency translation and CTA journals generated alongside intercompany eliminations — not separately. |

| Mismatch detection and alerts | Automation is only valuable if it catches timing mismatches before the close runs, not after the consolidated accounts have been filed. |

| Chart of accounts mapping | Reclassification journals should be a one-time setup, not a monthly task. Look for AI-assisted mapping that learns from your group’s account structure. |

For most groups moving from a manual process to automated intercompany journals, the first month on a proper consolidation platform produces two things: a faster close and a list of mismatches that the manual process had been silently tolerating for months. Both outcomes are worth having.