The board meeting is in four days. The CFO has four entities to consolidate. Three of them have closed their books; the fourth is still reconciling. The intercompany management fees need to be eliminated. The Australian entity’s figures need to be translated to sterling. And somewhere in the resulting spreadsheet, a formula is pulling from the wrong tab.

This is not an unusual situation for finance directors managing multi-entity groups. Board reporting is the destination that the entire month-end close process is working towards — and yet for most groups, the consolidation process is still slow and manual enough that the board pack arrives late, reflects a position that is already several days old, and leaves the CFO unable to answer detailed questions without going back to the data.

Effective board reporting for multi-entity groups requires more than assembling numbers: it demands a consolidation process fast enough to deliver timely data, and a reporting layer flexible enough to give the board the view they need without a week of preparation. This post covers what a group board pack should contain, where the process tends to break down, and what good looks like.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

What a Group Board Pack Should Contain

The content of a board pack varies by group size and industry, but the core elements are consistent for any multi-entity structure:

- Consolidated P&L vs budget and prior year. The headline numbers: group revenue, gross profit, operating costs, EBITDA, and profit before tax — with variance columns showing movement against the approved budget and the prior year equivalent period. This is the table the board turns to first.

- Entity-by-entity P&L breakdown. A second layer showing the same P&L structure split by entity or business unit. When group revenue is down, the board needs to see where. This is the view that requires consolidation to work correctly — it is not available until intercompany eliminations have been applied.

- Consolidated balance sheet summary. Key metrics: net assets, debt position, working capital, and significant balance sheet movements since the prior period. Not always presented in full in the board pack, but the key drivers should be.

- Cash and liquidity summary. Cash balances by entity, net debt position, and headroom against facilities. Boards focus on cash at least as much as profitability.

- KPI dashboard. The three to seven metrics most relevant to the business model — revenue per employee, gross margin by product line, customer retention, or whatever the group tracks as leading indicators of performance.

- Narrative commentary. The CFO’s interpretation of the numbers: what drove the variances, what actions are underway, what the outlook is for the remainder of the period. This is the part that turns data into insight.

Why Multi-Entity Board Reporting Is Harder Than It Looks

Single-entity reporting is straightforward: the accounting system produces a P&L, the CFO formats it, the board reads it. Multi-entity board reporting adds several layers of complexity that each take time and introduce error risk.

Consolidation must come first

The board pack cannot be produced until the consolidation is complete. And the consolidation cannot be complete until intercompany transactions have been identified, matched, and eliminated. A board P&L that includes management fees charged by the holding company to subsidiaries, or intercompany loans sitting in both entities’ balance sheets, is not a group P&L — it is an aggregation of entity accounts, which is a different thing. The board pack is only as reliable as the consolidation process that precedes it.

Timing compounds the problem

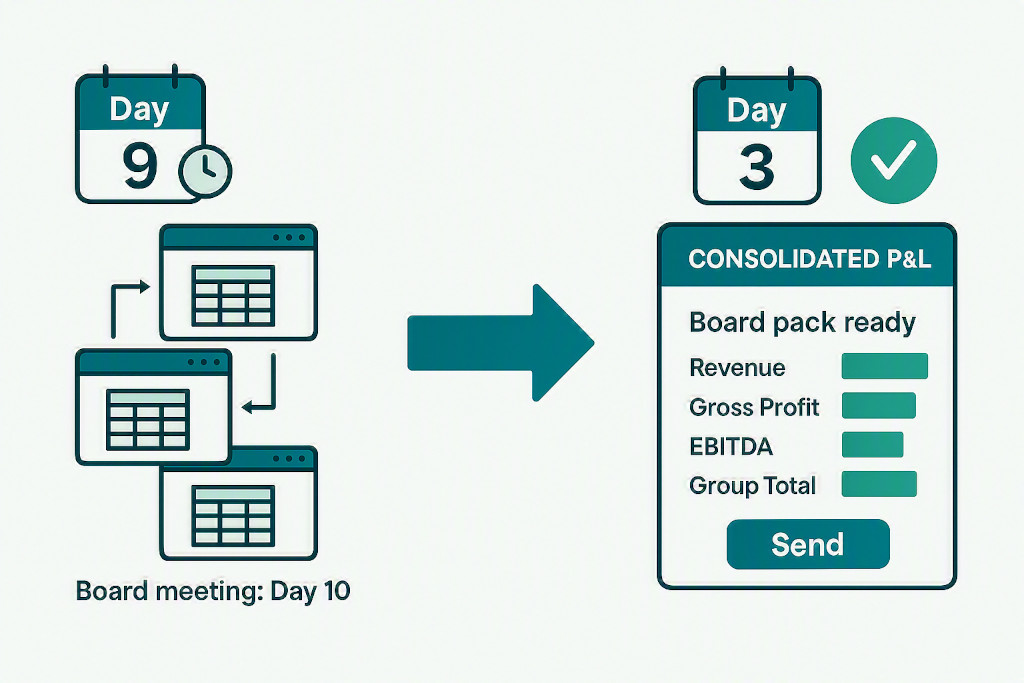

If the group consolidation takes eight days to complete, the board pack reflects a position that is already over a week old by the time directors receive it. In a fast-moving business, that lag matters. Reducing the consolidation timeline — from eight days to three or four — is one of the highest-value improvements a group finance team can make, both for board reporting quality and for management decision-making speed. The post on the multi-entity month-end close checklist covers the steps involved in tightening that timeline.

Variance answers require drill-down

Every board meeting produces questions. Revenue is £300k below budget — which entity, which product line, which customer? Gross margin has contracted by 1.8 percentage points — is it a mix issue or a pricing issue? A CFO who cannot answer these questions in the room, or who has to say “I’ll come back to you on that”, loses credibility and board confidence. The ability to drill from the group P&L down to entity, account, and transaction level is what separates board reporting that informs decisions from board reporting that merely reports history.

A Practical Example: Board Pack for a Four-Entity Retail Group

Consider RetailGroup Holdings Ltd, a UK-based group with four trading entities:

| Entity | Description | Revenue (Month) |

|---|---|---|

| RetailGroup Holdings Ltd | UK holding company | — |

| Retail UK Ltd | UK retail trading | £1,840,000 |

| Retail AU Pty Ltd | Australian retail (AUD) | A$960,000 (≈ £510,000) |

| Wholesale UK Ltd | UK wholesale trading | £620,000 |

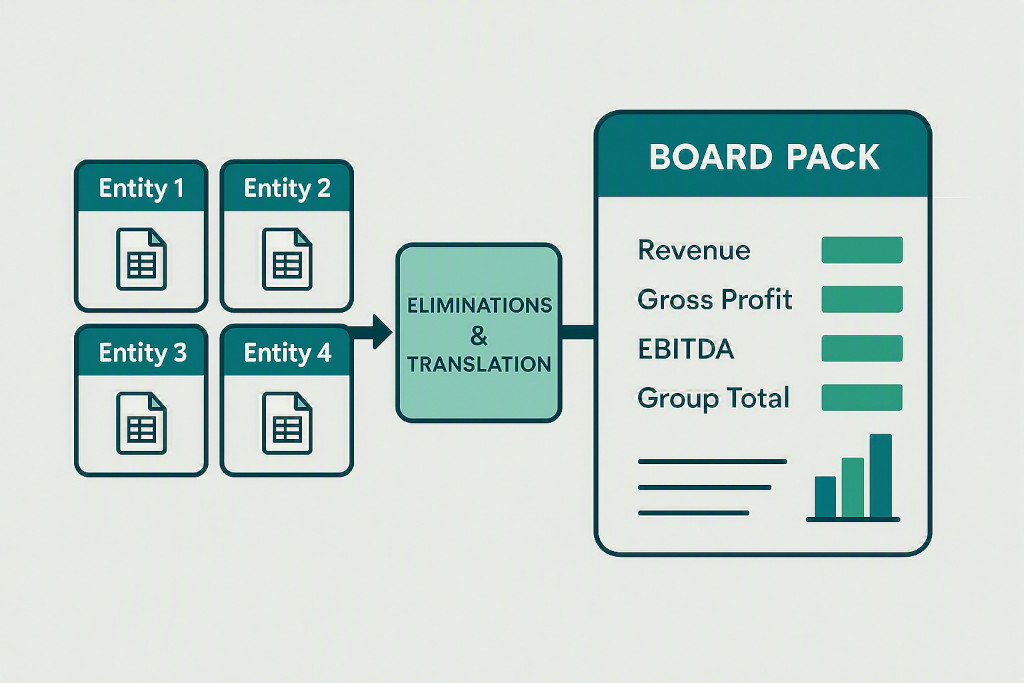

The holding company charges a £25,000 management fee to each trading entity each month. At consolidation, £75,000 of management fee income (in Holdings) and £75,000 of management fee expense (across the three trading entities) are both eliminated — they net to zero at the group level and must not appear in the board P&L.

The consolidated group P&L for the board pack looks like this:

| £000s | Retail UK | Retail AU | Wholesale UK | Eliminations | Group Total |

|---|---|---|---|---|---|

| Revenue | 1,840 | 510 | 620 | — | 2,970 |

| Cost of sales | (1,104) | (306) | (434) | — | (1,844) |

| Gross profit | 736 | 204 | 186 | — | 1,126 |

| Operating costs | (480) | (165) | (140) | — | (785) |

| Management fees (interco) | (25) | (25) | (25) | 75 | — |

| EBITDA | 231 | 14 | 21 | 75 | 341 |

This is the table the board needs: a consolidated group view with the entity breakdown visible. Producing it requires the intercompany management fee elimination to have been applied correctly, and the Australian entity’s AUD figures to have been translated to GBP at the average rate for the month. Neither of these steps is automatic in a spreadsheet-based process.

“The board does not want to see four separate P&Ls. They want to see one group P&L — and then, when they have a question about a specific entity, they want to be able to get to that entity’s numbers in seconds. That combination is what a good consolidation tool provides.”

Segment Reporting and Virtual Groups in the Board Pack

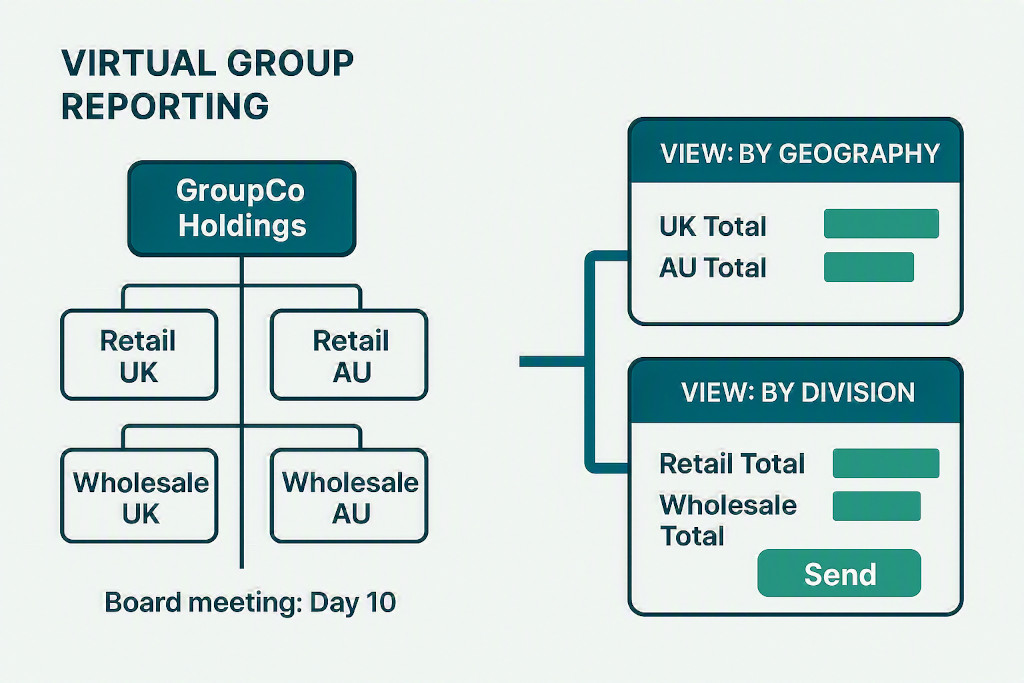

Many boards want to see performance cuts that do not map neatly onto legal entity structure. A retail group with entities in two countries and two business divisions wants a view by geography (UK total vs Australia total) and a separate view by division (Retail total vs Wholesale total) — in addition to the entity-by-entity breakdown.

In a spreadsheet, each additional reporting cut requires a new tab and a new set of formulas. When the underlying data changes, every tab must be updated. The risk of inconsistency between views grows with each additional cut.

BrizoConsol’s Virtual Groups feature addresses this directly. Virtual Groups allow the finance team to define reporting segments — by geography, brand, product line, or any other dimension — independently of legal entity structure. The same underlying consolidation data powers every view, and each Virtual Group updates automatically when the entity data is refreshed. For the RetailGroup board pack, the CFO can present a geography view, a division view, and an entity view from a single consolidated data set, without maintaining three separate reconciliation files.

Controlling which views different stakeholders can access — board members, entity managers, external investors — is covered in the post on controlling who sees what in group reporting.

What Good Board Reporting Software Does for Multi-Entity Groups

Effective board reporting for multi-entity groups depends on the consolidation layer that sits beneath it. The board pack is only as good as the data it draws from — and that data is only reliable if the consolidation has been done correctly, completely, and on time.

BrizoConsol supports the full chain from entity data to board pack:

- Direct API connections to Xero, QuickBooks, MYOB and Zoho Books. No CSV exports, no manual trial balance imports. Entity data is live and consistent across all platforms simultaneously.

- Automatic intercompany eliminations. Management fees, intercompany loans, and intercompany sales are eliminated at every close once configured, removing the most error-prone step in the consolidation process.

- Multi-currency translation with automatic CTA. International entities are translated to the group’s presentation currency at the correct rates, with the cumulative translation adjustment calculated and posted to group equity automatically.

- Consolidated P&L, Balance Sheet and Cash Flow available on demand. The group financial statements are available as soon as the entities have closed — not after an additional assembly step. A board pack can be produced on day three of the close rather than day nine.

- Virtual Groups for segment reporting. Report by geography, division, brand, or any other dimension without additional consolidation work. Each view draws from the same validated data set.

- Drill-down from group to entity to account. When the board asks why gross margin moved, the CFO can reach the entity-level and account-level answer without leaving the system. The group variance analysis post covers how this works in practice for common board questions.

- Audit trail on all consolidation adjustments. Every elimination, currency adjustment, and consolidation journal is logged, which matters both for board confidence and for year-end audit.

Board reporting for multi-entity groups does not have to mean a week of spreadsheet assembly before every meeting. With the right consolidation infrastructure in place, the data the board needs is available within days of the close — accurate, consistent across every reporting view, and deep enough to answer the questions that follow.

Deliver Your Board Pack in Days, Not a Week

Connect your entities, automate intercompany eliminations, and produce a consolidated group P&L with entity breakdown — ready for the board before the close has even finished. Start Free Trial