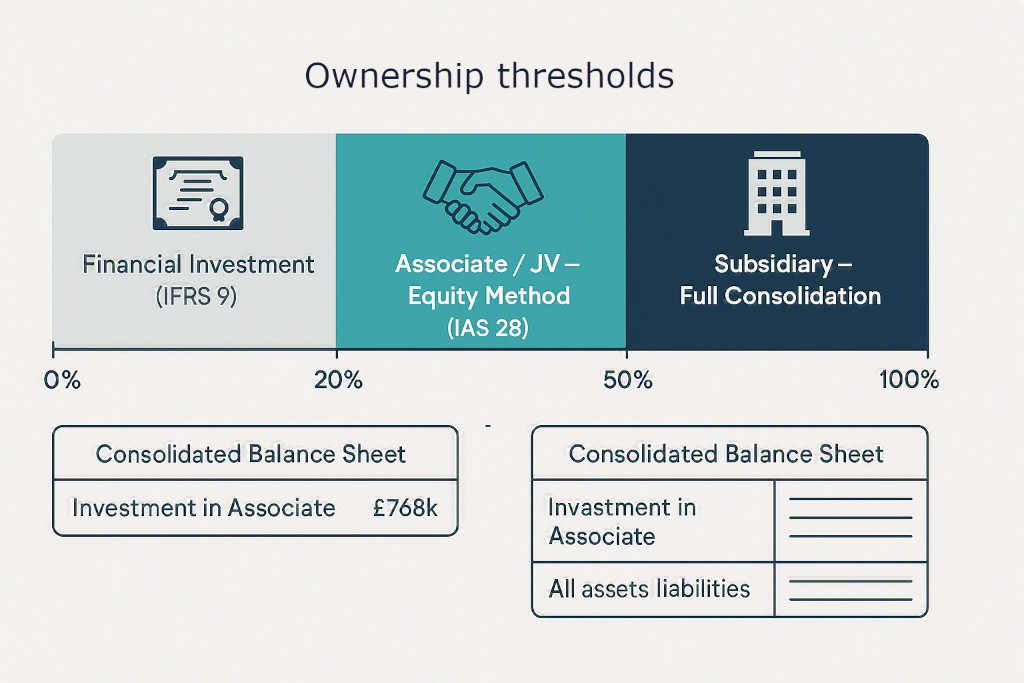

Not every company a group controls or invests in gets fully consolidated. When a parent holds a stake of between roughly 20% and 50% in another entity — enough to exercise significant influence over its operating and financial policies, but not enough to control it outright — a different accounting treatment applies. Instead of bringing all of the investee’s assets, liabilities, revenues, and costs into the group accounts line by line, the group recognises a single asset on its balance sheet: the carrying value of the investment, adjusted each period to reflect the group’s share of the investee’s results.

This treatment is the equity method, and it applies to two categories of investment: associates (governed by IAS 28 under IFRS, or FRS 102 Section 14 under UK GAAP) and jointly controlled entities that qualify as joint ventures under IFRS 11. Understanding how the equity method works — and how it differs from full consolidation — is essential for any group finance team that holds interests in entities it does not fully control.

What Is the Equity Method?

The equity method is sometimes called the “one-line consolidation”. Instead of consolidating an associate’s revenue, costs, assets, and liabilities into the group accounts, the investor recognises:

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

- On the balance sheet: a single asset line — “Investment in associates” — initially measured at cost and subsequently adjusted for the investor’s share of the associate’s post-acquisition profits, losses, and other comprehensive income.

- In the P&L: a single line — “Share of profit of associates” — representing the investor’s proportionate share of the associate’s profit or loss for the period.

The method is described as “one-line” because, however large or complex the associate may be, its contribution to the group accounts is compressed into these two entries. A fully consolidated subsidiary might contribute hundreds of individual account balances; an associate under the equity method contributes one balance sheet line and one P&L line.

When Does the Equity Method Apply?

The equity method applies when an entity has significant influence over, but does not control, an investee. The key categories are:

Associates (IAS 28)

An associate is an entity over which the investor has significant influence. IAS 28 creates a rebuttable presumption that if an investor holds 20% or more of the voting power of an investee, it has significant influence — unless the contrary can be clearly demonstrated. Conversely, if the investor holds less than 20%, it is presumed not to have significant influence — unless it can be clearly demonstrated otherwise.

Shareholding percentage alone is not determinative. The following factors are evidence of significant influence regardless of the exact stake held:

- Representation on the board of directors or equivalent governing body.

- Participation in policy-making processes, including decisions about dividends.

- Material transactions between the investor and investee.

- Interchange of managerial personnel.

- Provision of essential technical information.

A group with a 15% stake and two board seats almost certainly has significant influence. A group with a 25% stake and no board representation, no material transactions, and no other involvement may not. The assessment requires judgement, and the conclusion should be documented.

Joint ventures (IFRS 11)

Under IFRS 11, a joint arrangement is one in which two or more parties have joint control — contractually agreed sharing of control such that unanimous consent is required for decisions about relevant activities. IFRS 11 distinguishes between joint operations (where the parties have rights to the assets and obligations for the liabilities — accounted for by recognising each party’s share directly) and joint ventures (where the parties have rights to the net assets of the arrangement — accounted for using the equity method).

The old IAS 31 approach of proportionate consolidation for joint ventures — bringing in a pro-rata share of the JV’s revenues, costs, assets, and liabilities — is no longer permitted under IFRS. All joint ventures must use the equity method. This change affects construction groups, infrastructure investors, and any other business where JV structures are common.

“The equity method applies when you have influence but not control. Full consolidation applies when you have control. For everything else — financial investments below 20% without significant influence — IFRS 9 applies, and you are accounting for a financial asset, not an investment in a business.”

How the Equity Method Works: Year-by-Year Movement

The mechanics of the equity method are straightforward once the initial recognition is established. The investment is initially recognised at cost on the acquisition date. After that, the carrying amount moves up or down with the investor’s share of the associate’s results:

- Share of profit: increases the carrying amount (Dr Investment in associate / Cr Share of profit of associates in P&L).

- Share of loss: decreases the carrying amount (Dr Share of loss in P&L / Cr Investment in associate). The carrying amount cannot fall below zero unless the investor has guaranteed obligations for the associate’s losses.

- Dividends received: decrease the carrying amount — they represent a return of the investment, not income (Dr Cash / Cr Investment in associate). This is one of the most frequently misunderstood aspects of the equity method: dividends received from an associate do not go through the investor’s P&L.

- Share of other comprehensive income (OCI): if the associate recognises items in OCI (for example, pension actuarial gains and losses, or foreign currency translation differences on its own overseas operations), the investor includes its proportionate share in its own OCI.

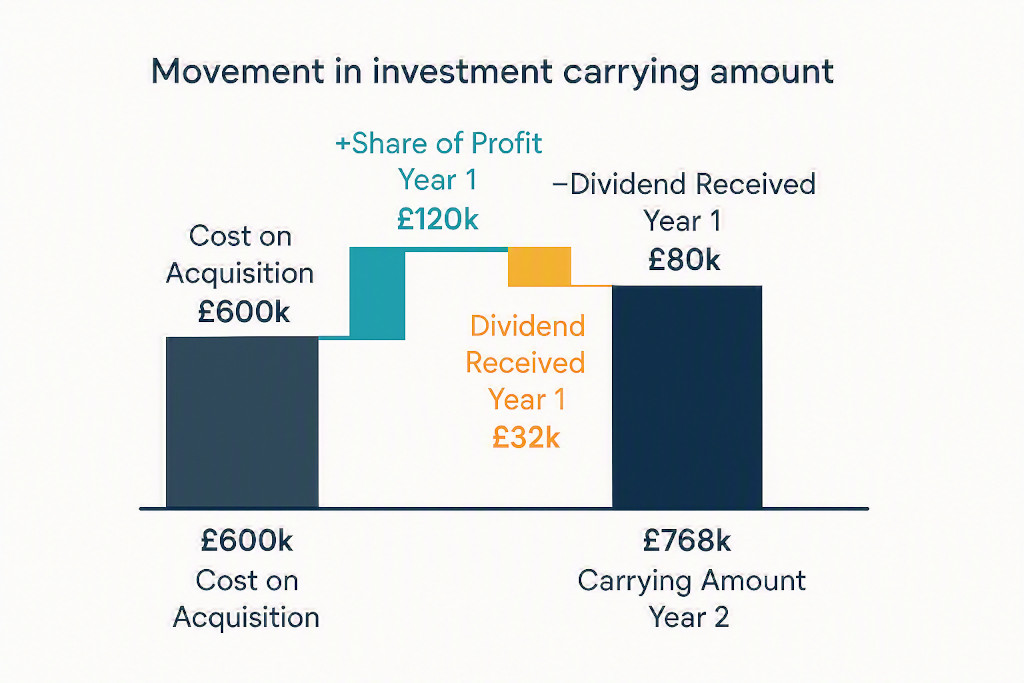

A Practical Example: InvestCo’s 40% Stake in PartnerCo

InvestCo Ltd acquires a 40% stake in PartnerCo Ltd on 1 January Year 1 for £600,000 cash. InvestCo has two seats on PartnerCo’s board and is involved in key operating decisions: this clearly constitutes significant influence, so the equity method applies.

| Period | Event | Amount £ | InvestCo 40% Share £ | Carrying Amount £ |

|---|---|---|---|---|

| 1 Jan Year 1 | Acquisition at cost | — | — | 600,000 |

| Year 1 | PartnerCo profit for year | 300,000 | +120,000 | 720,000 |

| Year 1 | Dividend paid by PartnerCo | 80,000 | −32,000 | 688,000 |

| Year 2 | PartnerCo profit for year | 200,000 | +80,000 | 768,000 |

| Year 2 | No dividend paid | — | — | 768,000 |

| Investment in associate — balance sheet (end Year 2) | 768,000 | |||

The consolidation journal for Year 2 is simply:

Dr Investment in associates £80,000

Cr Share of profit of associates (P&L) £80,000

Being InvestCo’s 40% share of PartnerCo’s Year 2 profit of £200,000.

In Year 1, a second journal was also required when the dividend was paid:

Dr Cash / Bank £32,000

Cr Investment in associates £32,000

Being InvestCo’s 40% share of PartnerCo’s dividend of £80,000. No P&L entry — the dividend reduces the investment carrying amount, not income.

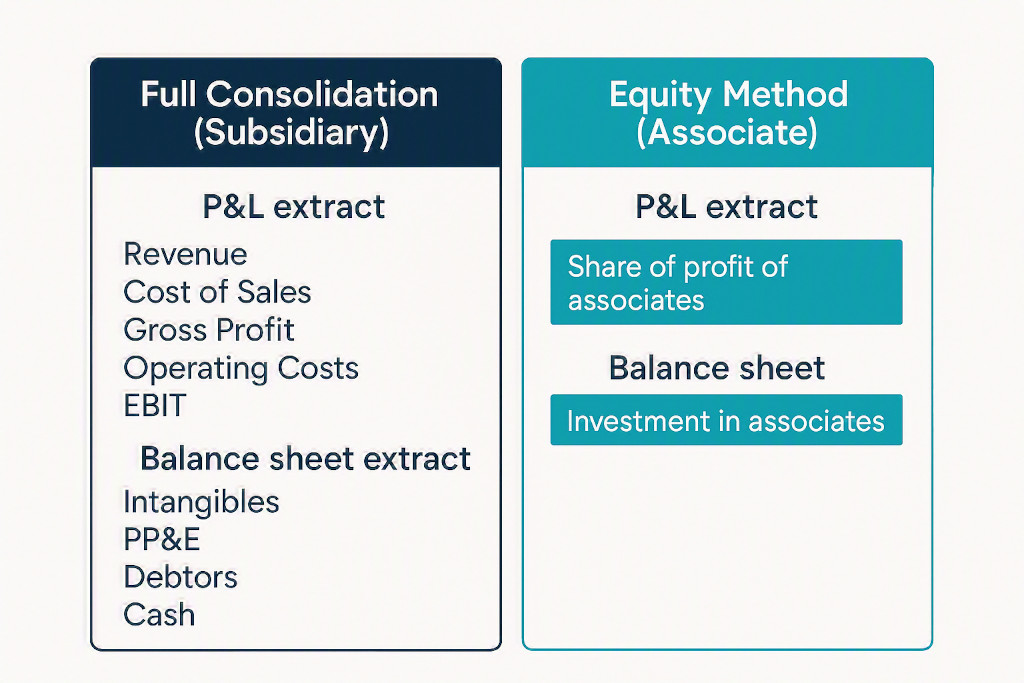

Equity Method vs Full Consolidation: What Appears in the Group Accounts

The difference between full consolidation and the equity method is significant for how the group accounts read — and for what the group consolidation process has to do each period.

| Item | Full Consolidation (Subsidiary) | Equity Method (Associate / JV) |

|---|---|---|

| Revenue | 100% of subsidiary’s revenue included line by line | Not included — nil contribution to group revenue |

| Operating costs | 100% of subsidiary’s costs included line by line | Not included |

| P&L contribution | Net of all revenues and costs, with NCI deducted below the line | Single line: “Share of profit of associates” |

| Balance sheet — assets | All subsidiary assets included line by line | Single line: “Investment in associates” |

| Balance sheet — liabilities | All subsidiary liabilities included | Not included (except investor’s obligations under guarantees) |

| Intercompany eliminations | Required for all intercompany balances and transactions | Partial elimination required for upstream/downstream transactions only |

| Goodwill recognition | Goodwill recognised separately on acquisition | Goodwill included within the carrying amount of the investment — not separately disclosed on the group balance sheet |

| NCI in equity | Non-controlling interest recognised in group equity | No NCI — the investor’s share only is recognised |

A practical consequence of the equity method is that the associate’s revenues do not form part of group revenue. This matters for groups where the associate is significant: a 40% stake in a business generating £10 million of revenue contributes nothing to the group’s top line — only a share of profit appears. Finance directors preparing group accounts for lenders or investors who focus on revenue metrics need to communicate this clearly.

Transactions Between the Group and the Associate

When a group entity sells goods or services to an associate (downstream) or buys from an associate (upstream), any unrealised profit remaining in the closing inventory or assets of the purchasing entity must be partially eliminated to the extent of the investor’s ownership interest.

This is similar in principle to the intercompany eliminations required for fully consolidated subsidiaries — covered in detail in the intercompany eliminations guide — but the elimination is partial rather than full, reflecting the fact that the investor is effectively selling to itself only to the extent of its ownership percentage.

Downstream example (group sells to associate)

InvestCo (40% stake in PartnerCo) sells goods to PartnerCo at cost plus 25%. During Year 2, InvestCo sells £240,000 of goods to PartnerCo. At the year end, PartnerCo holds £80,000 of these goods in closing inventory.

The unrealised profit embedded in PartnerCo’s closing inventory:

- Gross margin in the £80,000 closing stock = £80,000 × (25 ÷ 125) = £16,000

- InvestCo’s share of this unrealised profit = 40% × £16,000 = £6,400

The consolidation journal eliminates InvestCo’s share of the unrealised profit:

Dr Share of profit of associates (P&L) £6,400

Cr Investment in associates £6,400

Being elimination of InvestCo’s 40% share of unrealised profit in PartnerCo’s closing inventory. The investment carrying amount is reduced; the share of profit recognised from PartnerCo is reduced by the same amount.

When PartnerCo subsequently sells the goods to a third party, the profit is realised and the elimination reverses. This adjustment is required each period whenever material intercompany trading exists between the investor and the associate.

Goodwill Within the Investment Carrying Amount

When InvestCo acquired its 40% stake in PartnerCo for £600,000, it may have paid more than 40% of PartnerCo’s fair value net assets — a premium for significant influence, brand, or expected synergies. Under the equity method, any excess of the cost of the investment over InvestCo’s share of the fair value of PartnerCo’s net identifiable assets at the acquisition date is goodwill. This goodwill is not separately recognised on the group balance sheet; it is subsumed within the investment carrying amount.

The practical consequence is that the investment in associate balance is tested for impairment as a whole — if there is objective evidence that the carrying amount exceeds the recoverable amount, an impairment loss is recognised through the group P&L. Unlike goodwill on full consolidation, there is no separate annual impairment test for the goodwill component; the entire carrying amount is assessed together.

FRS 102 difference: Under FRS 102, the equity method is also required for associates, but the detailed rules differ in some respects from IAS 28 — in particular around goodwill within the investment and disclosure requirements. Groups reporting under UK GAAP should apply FRS 102 Section 14 rather than IAS 28, though the practical outcomes are similar for most straightforward associate relationships.

Joint Ventures in Construction and Infrastructure Groups

Joint ventures are particularly common in construction, civil engineering, and infrastructure, where two or more contractors combine to bid for and deliver a large contract that neither could handle alone. A formal JV agreement gives each party joint control — neither can direct the relevant activities without the other’s consent.

Under IFRS 11, such arrangements are typically classified as joint ventures (rather than joint operations) when the parties have rights only to the net assets of the arrangement — which is most commonly the case for separately incorporated JV vehicles. The equity method applies: each party recognises its share of the JV’s net assets as an investment on its balance sheet and its share of the JV’s profit in the P&L.

For a construction group with, say, a 50% stake in a project JV that generates £2,000,000 of profit over a three-year contract, the group’s contribution to its consolidated P&L over those three years is £1,000,000 of “share of profit of joint ventures” — not £4,000,000 of revenue and £3,000,000 of costs. Where the JV is material, this can significantly affect reported revenue and headline profitability compared with a fully consolidated entity delivering the same commercial outcome.

Equity Method Accounting in BrizoConsol

BrizoConsol supports equity method accounting as a standard feature of the group consolidation configuration. Associates and joint ventures are defined separately from fully consolidated subsidiaries, and the investment carrying amount is maintained within the system — updated each period for the group’s share of profit or loss, dividends received, and OCI items. The “Share of profit of associates” line appears in the group P&L automatically, and the “Investment in associates” balance reflects the cumulative movement from the acquisition date.

For groups that mix fully consolidated subsidiaries with equity-accounted associates — which is the common structure for holding companies, investment groups, and businesses that have grown through both wholly owned acquisitions and minority partnership arrangements — BrizoConsol handles both treatments within the same consolidation run, eliminating the need to maintain a separate workbook for the associate calculations outside the main consolidation model. The post on how to calculate non-controlling interest in financial consolidation covers the related topic of NCI in fully consolidated subsidiaries, which often arises alongside equity method investments in groups that hold a range of ownership stakes.

For finance directors managing a portfolio of interests at different ownership levels — some subsidiaries, some associates, some JVs — the ability to handle all three accounting treatments in a single platform, connected directly to the entities’ accounting systems, is what financial consolidation software should deliver as a baseline capability.

Handle Associates and JVs Alongside Your Fully Consolidated Group

BrizoConsol supports equity method accounting within the same consolidation run as your fully consolidated subsidiaries — no separate workbooks, no manual journals each period. Start Free Trial