Construction holding groups are structurally complex almost by design. The standard mid-market model — a holding company sitting above a collection of project SPVs, a trading entity or two, and a central plant or services company — creates a consolidation challenge that generic accounting software is not built to handle. Each entity has different revenue profiles, different balance sheet characteristics, and a web of intercompany charges that must be eliminated before the group accounts mean anything.

Add in IFRS 15 revenue recognition across contracts at different stages of completion, retention balances that sit in debtors for twelve months or more, and the occasional international entity bringing a foreign currency into the mix, and you have a group that requires a structured consolidation process every single month — not a spreadsheet that gets rebuilt from scratch each quarter.

This post covers the specific consolidation challenges that arise in construction groups, with a worked example showing how the key adjustments flow through to the group P&L and balance sheet.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

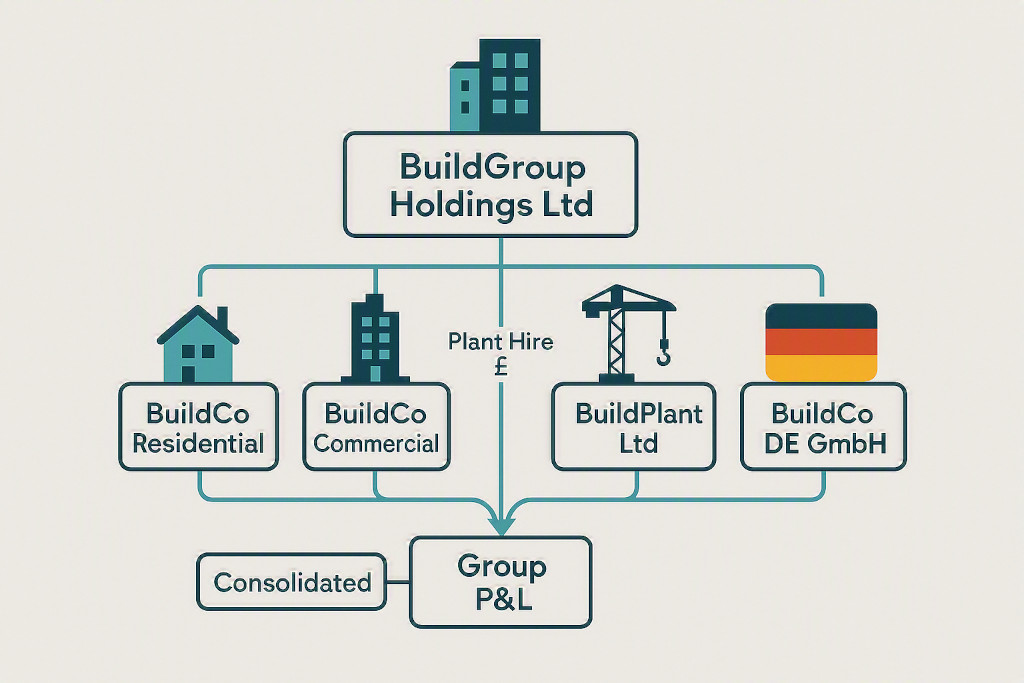

How Construction Groups Are Typically Structured

The most common structure for a UK construction holding group looks like this:

- Holding company. Owns the shares in all subsidiaries, may charge a management fee, holds the group’s banking facilities and any external debt.

- Trading entities. One or more companies that win and deliver contracts — residential, commercial, civil engineering, fit-out, or specialist subcontract work. Each may trade in a different sector with different margin profiles.

- Project SPVs. Larger developments (particularly residential or mixed-use) are often ring-fenced into separate special purpose vehicles — one company per development. This limits liability, satisfies funder requirements, and creates a clean audit trail per project.

- Central plant and equipment company. Groups that own significant plant — excavators, cranes, scaffolding, concrete pumps — often hold these assets in a separate entity and charge hire to the operating entities. This protects assets from project risk and allows the plant pool to be managed centrally.

- International entities. Larger groups operate in Europe, the Middle East, or further afield through locally incorporated subsidiaries, introducing foreign currency translation into the consolidation.

Each layer of this structure creates consolidation work: intercompany balances to eliminate, transactions to cancel out, and financial statements in different currencies to translate. Consider the worked example below — BuildGroup Holdings Ltd, a UK mid-market construction group.

| Entity | Type | Currency | Accounting System |

|---|---|---|---|

| BuildGroup Holdings Ltd | UK holding company | GBP | Xero |

| BuildCo Residential Ltd | Residential construction trading | GBP | Xero |

| BuildCo Commercial Ltd | Commercial & fit-out trading | GBP | QuickBooks |

| BuildPlant Ltd | Central plant & equipment | GBP | Xero |

| BuildCo DE GmbH | German commercial construction | EUR | QuickBooks |

Revenue Recognition Under IFRS 15: The Construction Group Challenge

IFRS 15 requires that revenue on construction contracts be recognised as performance obligations are satisfied — which for most construction contracts means over time, using the stage-of-completion (percentage of completion) method. Each contract has its own completion percentage, measured either by costs incurred as a proportion of total estimated costs, or by surveys of work performed.

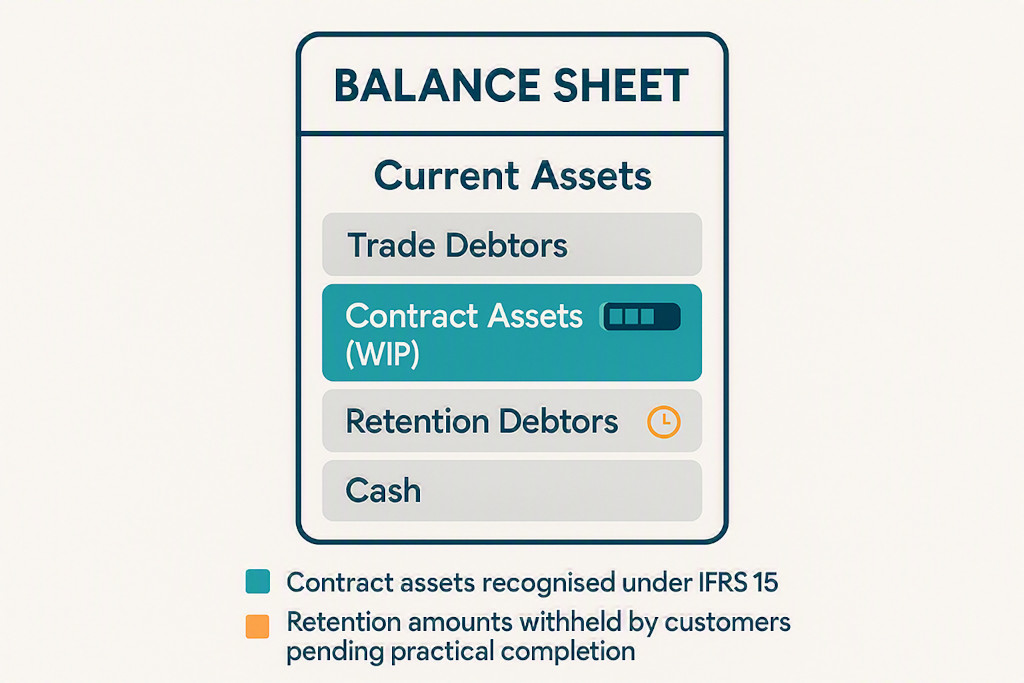

For a construction group consolidation, this means that the group P&L reflects revenue earned across multiple contracts at different stages simultaneously, and that the balance sheet carries contract assets (the excess of revenue recognised over amounts billed) and contract liabilities (the excess of amounts billed over revenue recognised) for each contract in progress.

BuildCo Residential’s active contract portfolio at the month-end looks like this:

| Contract | Total Value £ | Completion % | Revenue to Date £ | Billed to Date £ | Contract Asset / (Liability) £ |

|---|---|---|---|---|---|

| Maple Quarter (residential) | 4,200,000 | 65% | 2,730,000 | 2,500,000 | 230,000 |

| Birchwood Estate (residential) | 2,800,000 | 20% | 560,000 | 630,000 | (70,000) |

| Oakfield Close (residential) | 6,100,000 | 95% | 5,795,000 | 5,700,000 | 95,000 |

| Total — BuildCo Residential | 13,100,000 | 9,085,000 | 8,830,000 | 255,000 |

The net £255,000 contract asset sits on BuildCo Residential’s balance sheet as “amounts recoverable on contracts” or “contract assets” under IFRS 15 terminology. When the group balance sheet is consolidated, these contract assets from BuildCo Residential and the equivalent figures from BuildCo Commercial and BuildCo DE GmbH are all brought in at their entity-level amounts — there are no intercompany adjustments required on the contract assets themselves, unless contracts cross entity boundaries within the group.

Contract Assets, Retention, and WIP on the Consolidated Balance Sheet

Construction group balance sheets carry several items that do not appear in most other industries, and that require careful presentation in the consolidated accounts.

Retention debtors

Most UK construction contracts retain a percentage of each application for payment — typically 3% to 5% — until practical completion and the expiry of a defects liability period. These retentions can sit in debtors for twelve to eighteen months after the work is complete. On the consolidated balance sheet, retentions are usually split between current (due within twelve months) and non-current (due after twelve months) debtors. In a group with several large contracts in their defects period simultaneously, the total retention balance can represent a significant portion of net assets — and getting it wrong in the consolidation (for example, by double-counting it as both a debtor and an income accrual) is a common error.

Intercompany retention balances

Where one group entity subcontracts work to another — for example, BuildCo Residential engaging BuildPlant Ltd for scaffolding erection as a subcontract rather than a hire — the main contractor retains a percentage of each payment to the subcontractor. This creates an intercompany retention creditor (in the main contractor) and an intercompany retention debtor (in the subcontractor) that must both be eliminated on consolidation, in the same way as any other intercompany balance.

Eliminating Intercompany Plant Hire in a Construction Group

The central plant company model is efficient operationally, but it creates a category of intercompany transaction that must be eliminated on consolidation every single month. BuildPlant Ltd charges plant hire to the two UK trading entities:

- BuildCo Residential: £35,000/month plant hire

- BuildCo Commercial: £25,000/month plant hire

Over twelve months, this produces £720,000 of plant hire income in BuildPlant Ltd and £720,000 of plant hire expense in the trading entities. Both sides of this transaction must be eliminated in the group P&L — they are internal charges and do not represent revenue or cost at the group level. Additionally, if any plant hire invoices are unpaid at the month-end, the intercompany debtor (in BuildPlant) and intercompany creditor (in the trading entities) must be eliminated from the group balance sheet.

The consolidation journal for the annual plant hire elimination is:

Dr Plant Hire Income (BuildPlant P&L) £720,000

Cr Plant Hire Expense (BuildCo Residential P&L) £420,000

Cr Plant Hire Expense (BuildCo Commercial P&L) £300,000

Group effect: zero net impact on group P&L. BuildPlant’s income disappears; the trading entities’ costs disappear. The plant depreciation in BuildPlant remains, as this is a genuine cost to the group.

This is a standard intercompany elimination — the same principle applies to management fees, intercompany loans, and any other transactions between entities within the group. The intercompany eliminations guide covers the full range of elimination types, including how to handle situations where intercompany invoices are outstanding at the period end and the balances do not match between entities.

Watch out for: The depreciation on plant owned by BuildPlant Ltd is a real cost to the group — it should not be eliminated. Only the intercompany hire charge (income in BuildPlant / expense in the trading entities) is eliminated. A common error is to eliminate both the hire charge and the depreciation, which understates the group’s true asset usage costs.

Foreign Currency Translation: BuildCo DE GmbH

BuildCo DE GmbH operates in Germany and reports in EUR. Its accounts are translated into GBP for consolidation using the IAS 21 closing rate / average rate method: balance sheet items at the closing rate at the period end, and P&L items at the average rate for the period. The resulting foreign currency translation difference — arising because assets are translated at a different rate to the one used when they were initially recognised — is taken to the currency translation reserve in group equity rather than through the P&L.

For the current period, using a closing EUR/GBP rate of 0.848 and an average rate of 0.841:

| BuildCo DE GmbH | EUR | Rate | GBP £ |

|---|---|---|---|

| Revenue (P&L) | 1,240,000 | 0.841 (avg) | 1,042,840 |

| Operating costs (P&L) | (980,000) | 0.841 (avg) | (824,180) |

| Operating profit (P&L) | 260,000 | 218,660 | |

| Net assets (balance sheet) | 1,850,000 | 0.848 (close) | 1,568,800 |

The intercompany management fee charged by BuildGroup Holdings to BuildCo DE GmbH (£15,000 per month, invoiced in GBP) introduces a further complexity: the fee is denominated in GBP but sits as an expense in a EUR entity. Both sides of the management fee must be eliminated on consolidation, but the EUR entity will have recorded the GBP invoice at the exchange rate prevailing on invoice date, which will differ from the closing rate. Any exchange difference on the intercompany balance must be considered when reconciling the elimination.

Group Management Fees in a Construction Group

BuildGroup Holdings charges a £15,000/month management fee to each of its three trading entities (BuildCo Residential, BuildCo Commercial, BuildCo DE GmbH). At the group level, these fees eliminate entirely:

- £540,000 per year of management fee income (in Holdings) — eliminated.

- £540,000 per year of management fee expense (across the three trading entities) — eliminated.

The result is that the group P&L shows neither the income nor the expense. This is a straightforward elimination, but it must be configured correctly and applied consistently. In a spreadsheet-based process, this is one of the first adjustments to be missed if the intercompany schedule is not kept up to date — particularly when a new entity joins the group mid-year and its management fees begin partway through the period. Designing a common chart of accounts across all group entities ensures that management fees, plant hire, and other intercompany charges are coded consistently, making the eliminations straightforward to identify and apply.

What the Consolidated Group P&L Looks Like

After eliminations and currency translation, the BuildGroup consolidated P&L for the month shows:

| £000s | Residential | Commercial | Plant | DE GmbH | Eliminations | Group Total |

|---|---|---|---|---|---|---|

| Revenue | 758 | 520 | — | 87 | — | 1,365 |

| Plant hire income | — | — | 60 | — | (60) | — |

| Direct costs | (571) | (364) | (38) | (69) | — | (1,042) |

| Plant hire expense | (35) | (25) | — | — | 60 | — |

| Overheads | (62) | (44) | (8) | (11) | — | (125) |

| Management fees (interco) | (15) | (15) | — | (15) | 45 | — |

| Operating profit | 75 | 72 | 14 | (8) | 45 | 198 |

The eliminations column resolves to zero net income effect — plant hire in and out cancel, management fees in and out cancel — leaving a group operating profit of £198,000 that reflects only value generated externally. BuildCo DE GmbH is running a small operating loss this month; the group entity-level view makes this immediately visible without requiring a separate management pack.

Financial Consolidation for Construction Groups in BrizoConsol

BrizoConsol connects to the accounting systems used across a construction group — Xero for Holdings, Residential, and Plant; QuickBooks for Commercial and the German entity — and pulls entity data via direct API each time the consolidation is run. Intercompany eliminations for plant hire, management fees, and intercompany loans are configured once and applied automatically at every close. The EUR translation for BuildCo DE GmbH uses the exchange rates entered for the period, calculates the currency translation adjustment, and posts it to the group’s foreign currency translation reserve without requiring a manual journal.

For construction groups that have historically relied on a multi-tab Excel model to produce monthly group accounts, the shift to a connected consolidation tool means that the first meaningful output — a consolidated P&L with eliminations applied and entity columns visible — is available on the day the last entity closes its books, rather than three days later. That timing matters when the board meets in the first two weeks of the month and the finance director needs reliable numbers before the meeting.

The post on what financial consolidation software does and why your group needs it covers the broader case for moving off spreadsheets, including the specific failure modes that affect construction groups most acutely: intercompany balances that do not reconcile, elimination errors that only surface at year-end, and consolidation packs that take a week to produce when the board wants answers in 48 hours.

Built for Construction Groups: Connect, Consolidate, Report

BrizoConsol connects to Xero and QuickBooks across all your entities — holding company, trading entities, plant company, international subsidiaries — and produces a consolidated group P&L with eliminations applied, every month. Start Free Trial