The group finance manager of a quick-service restaurant franchise received an urgent request from the board on the last Thursday of March: consolidated accounts for the group’s eleven entities, formatted for a bank covenant review, due by end of the following week.

She knew the numbers. Each entity ran its own accounting file — four in Xero, four in QuickBooks, three in MYOB — and she had been pulling those books together manually in Excel for three years. It had always taken around a fortnight. She had eight working days.

The request was not unusual. What was unusual was that she finished in six days — and with no errors in the royalty eliminations for the first time in two years.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

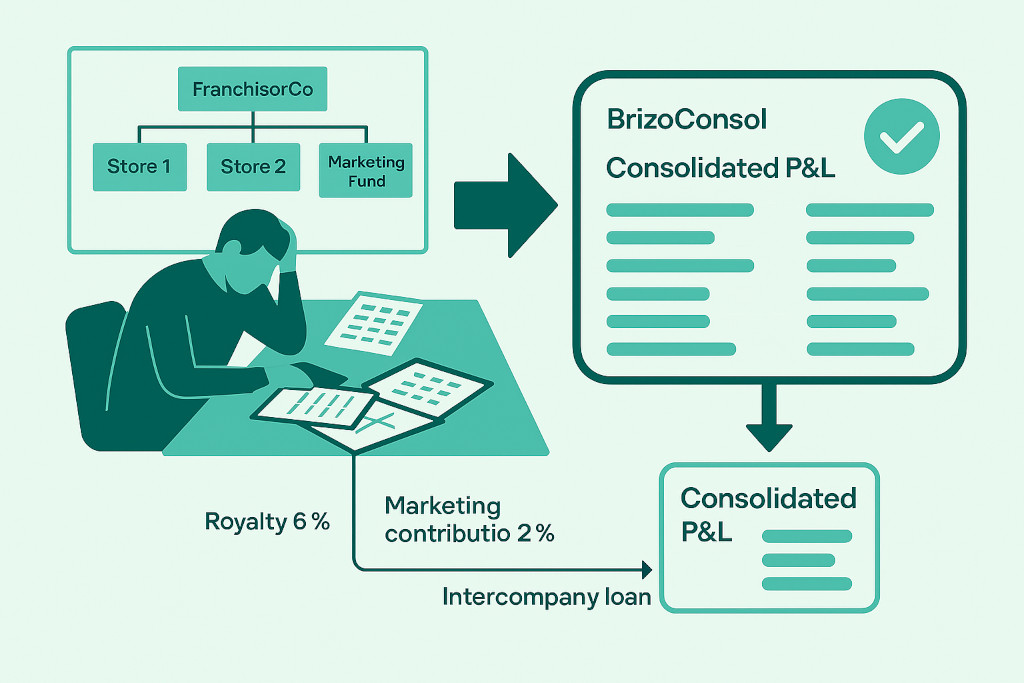

Franchise groups are a distinct and often underserved category when it comes to financial consolidation. The structure looks simple on paper: a central franchisor entity, a set of store-level entities, maybe a marketing fund and an IP holding company. In practice, the intercompany flows — royalties, brand fees, management charges, and intra-group loans — create an elimination workload that most consolidation guides barely address.

This article walks through what makes franchise group consolidation different, where the manual process breaks down, and how multi-entity finance teams get it right.

Why Franchise Groups Are Harder to Consolidate Than Standard Groups

Most multi-entity groups consolidate a parent that holds subsidiaries engaged in different activities. The intercompany flows tend to be relatively predictable: management fees, intercompany loans, and dividends. There is usually one elimination journal type that accounts for the bulk of the work.

Franchise groups are different in three ways.

First, the royalty flow is structural, recurring, and runs in the same direction every month. Each operating entity pays a royalty to the franchisor or IP holding entity based on a percentage of revenue. That royalty is revenue in the franchisor’s books and an expense in each store’s books. It must be eliminated in full on consolidation. In a group with fifteen stores, that is fifteen elimination entries before you have touched anything else.

Second, the marketing fund introduces a separate legal entity. Most franchise systems pool a percentage of each store’s revenue into a centralised marketing fund, often held in a distinct company or trust. That fund makes contributions that flow between entities, creating its own set of intercompany balances that must reconcile and be eliminated.

Third, the ownership structure is often layered. Some stores may be company-owned at 100%, others partially owned through a joint venture with an operating partner. Where non-controlling interests exist, the consolidation becomes more complex — NCI share calculations must be applied to each partially owned entity’s equity and earnings before the group statements are correct.

These three features mean that franchise group consolidation has a systematically higher volume of recurring intercompany eliminations than most groups of equivalent size.

The Four Core Challenges

1. Royalty Eliminations

Royalty income in the franchisor entity and the corresponding royalty expense in each operating entity cancel each other out from the group’s perspective. The group never paid itself a royalty — it is simply revenue that moved from one pocket to another.

The elimination must be matched precisely. If the royalty is calculated on a monthly basis as 6% of net sales, and a store records $82,000 in royalty expense, the franchisor entity should record exactly $82,000 in royalty income from that store. Timing differences and rounding, common in franchise systems, cause these figures to drift — and the elimination journal must reconcile rather than simply reverse.

Understanding the mechanics of intercompany eliminations is essential before attempting franchise consolidation. Royalty flows behave identically in principle to management fee eliminations, but they occur more frequently and across more entity pairs.

2. Marketing Fund Accounting

The marketing fund entity receives contributions from all stores and spends on brand advertising. On consolidation, all contributions from operating entities to the fund eliminate against the fund’s income. Any amounts owing between the fund and the stores at period end — because contributions are received monthly but advertising spend is lumpy — create intercompany receivables and payables that must reconcile before the balance sheet will balance.

A marketing fund that is slightly underfunded at month-end will show an intercompany receivable on its balance sheet and a corresponding payable in the operating entities. If those figures do not agree to the cent, the consolidated balance sheet will be out.

3. Common Chart of Accounts

Franchise groups often have a structural advantage here: because the franchisor controls the accounting requirements for its entities, it can mandate a standardised chart of accounts across all operating stores. In practice, however, this advantage erodes over time. Stores accumulate local account codes, bookkeepers add convenience accounts, and by the time a consolidation is required the chart of accounts has diverged enough to make automated roll-ups unreliable.

Designing a common chart of accounts properly — with a master chart mapped at the group level and entity-level flexibility for local compliance — is one of the highest-leverage investments a franchise group finance team can make. It is the foundation on which every consolidation step rests.

4. Intercompany Loan Reconciliation

Most franchise groups fund store fit-outs or expansion through intercompany loans from the franchisor or a central treasury entity. These loans accumulate interest, are sometimes capitalised, and are not always documented with the same level of rigour as external debt. The intercompany loan balances and the associated interest must agree between the lending entity and the borrowing entity before they can be eliminated. A balance that differs by a single dollar will produce a consolidation error that is difficult to trace.

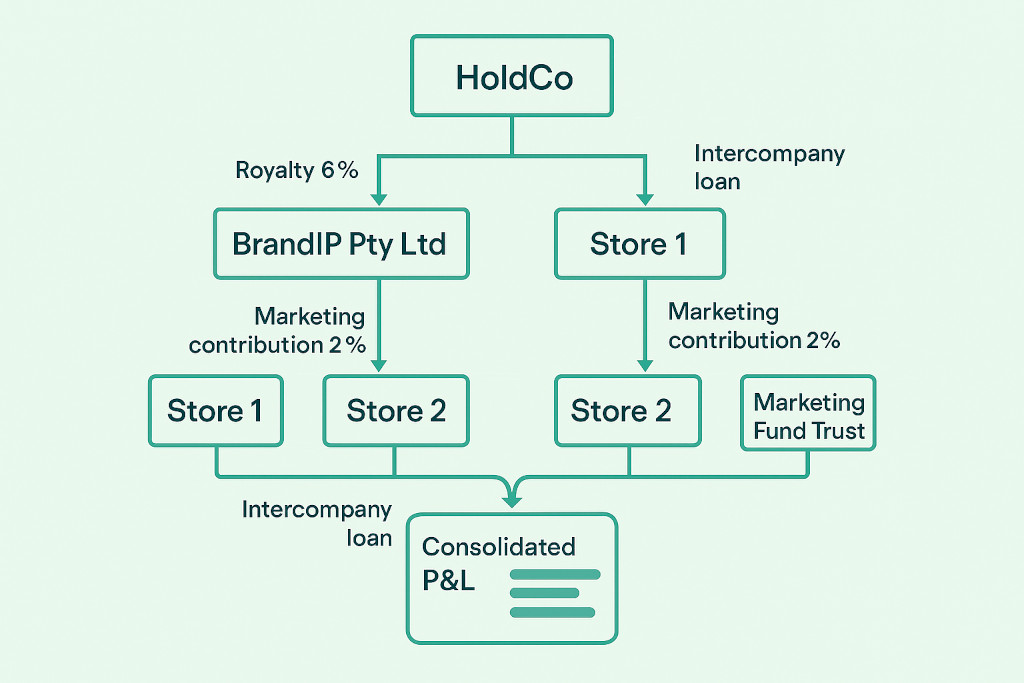

A Worked Example: Five-Entity Franchise Group

Consider the following group structure:

| Entity | Role | Currency | Ownership |

|---|---|---|---|

| HoldCo Pty Ltd | Parent / holding company | AUD | Ultimate parent |

| BrandIP Pty Ltd | IP holder — receives royalties | AUD | 100% owned by HoldCo |

| Store 1 Pty Ltd | Company-owned store | AUD | 100% owned by HoldCo |

| Store 2 Pty Ltd | Company-owned store | AUD | 80% owned by HoldCo |

| Marketing Fund Trust | Marketing fund | AUD | Controlled by HoldCo |

In May, each store pays a 6% royalty on net sales to BrandIP Pty Ltd. Store 1 reports net sales of $320,000; Store 2 reports $275,000. The royalty journal in each store and the corresponding income entry in BrandIP look like this before elimination:

| Entity | Account | Debit (AUD) | Credit (AUD) |

|---|---|---|---|

| Store 1 Pty Ltd | Royalty expense | 19,200 | |

| Store 1 Pty Ltd | Intercompany payable — BrandIP | 19,200 | |

| Store 2 Pty Ltd | Royalty expense | 16,500 | |

| Store 2 Pty Ltd | Intercompany payable — BrandIP | 16,500 | |

| BrandIP Pty Ltd | Intercompany receivable — Store 1 | 19,200 | |

| BrandIP Pty Ltd | Intercompany receivable — Store 2 | 16,500 | |

| BrandIP Pty Ltd | Royalty income | 35,700 |

The group consolidation elimination journal removes the royalty income and expense and cancels the intercompany payables and receivables:

| Consolidation elimination | Debit (AUD) | Credit (AUD) |

|---|---|---|

| Royalty income (BrandIP) | 35,700 | |

| Royalty expense (Store 1 + Store 2) | 35,700 | |

| Intercompany payable — BrandIP (Store 1 & 2) | 35,700 | |

| Intercompany receivable — Stores (BrandIP) | 35,700 |

Additionally, for Store 2 (80% owned), a non-controlling interest of 20% must be calculated on Store 2’s net profit and reflected in consolidated equity. None of this is especially complicated in isolation — the problem is doing it accurately, every month, across five or more entities, when the underlying data lives in separate accounting systems.

Where the Manual Process Breaks Down

Franchise finance teams who consolidate manually in Excel typically spend between two and four days per month on intercompany reconciliation alone — before they have even started the elimination journals. The sequence looks like this:

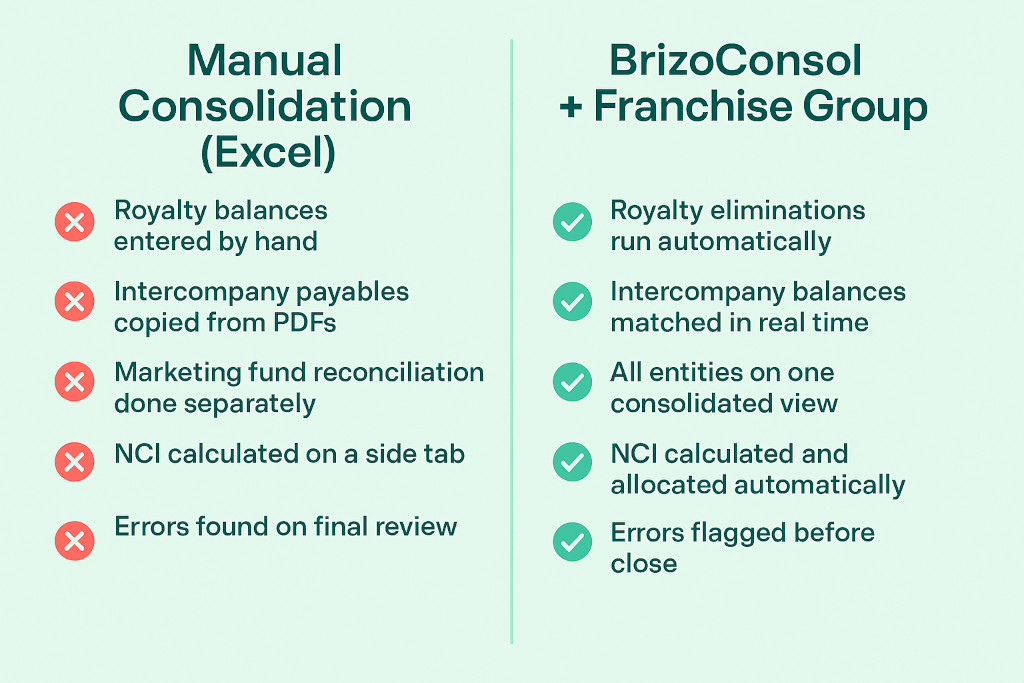

At month-end, each entity’s bookkeeper or accountant exports a trial balance. The group finance manager imports these into a consolidation workbook, maps each entity’s chart of accounts to the group chart, and runs a series of VLOOKUP or SUMIF formulas to produce a combined unadjusted trial balance. She then adds manual journals for each elimination — royalties, marketing fund contributions, management fees, intercompany loans — and rebalances the model.

Three things go wrong reliably. Royalty amounts do not agree between entities because stores and the IP company use different booking dates. Marketing fund balances carry rounding differences from the prior month. And at least one store has a chart of accounts item that did not exist last month, which breaks the mapping.

These are not signs of a poorly run finance function. They are the inevitable result of asking manual processes to handle what is fundamentally a data engineering problem.

Understanding how consolidation software cuts the month-end close for multi-entity groups helps frame the alternative — and the time savings are substantial even for groups with as few as three entities.

What Changes With Consolidation Software

When a franchise group connects its entities to a dedicated consolidation platform, three things change structurally.

First, the trial balance import is automated. Rather than exporting files and pasting data, the software pulls trial balances directly from each accounting system — Xero, QuickBooks, MYOB, Zoho Books — on a schedule or on demand. The group finance manager sees a live, current view of all entity balances without touching a spreadsheet.

Second, intercompany matching is systematic. The platform flags mismatches between intercompany payables and receivables — including royalty balances — so that the finance team can resolve differences at source rather than discovering them in the consolidation model. When the balances agree, the elimination journals run automatically.

Third, the chart of accounts mapping is stored as configuration. Once the group chart is built and each entity’s accounts are mapped to it, that mapping is persistent. A new account added at the store level is flagged for mapping — it does not silently misclassify itself.

Practical Considerations for Franchise CFOs

Before implementing a consolidation process — whether manual or software-assisted — franchise group finance leaders should address three structural questions.

Is the royalty calculation consistent? Royalties calculated on a revenue percentage are straightforward to eliminate. Problems arise when the calculation basis differs between the franchise agreement and the accounting treatment — for example, when some stores treat GST-inclusive revenue as the royalty base and others use GST-exclusive. Standardise the calculation basis first.

Is the marketing fund treated consistently? If the marketing fund is a separate legal entity, confirm whether it is controlled for consolidation purposes and should be fully consolidated, or whether it operates on a trustee basis that changes the treatment. This is an area where the accounting policy needs to be set deliberately rather than inherited from historical practice.

Are all intercompany balances documented? Intercompany loans in particular tend to accumulate without formal documentation. Before automating the consolidation, ensure that each loan has an agreed interest rate, a repayment schedule, and a balance that both parties can confirm. Loans without documentation create audit risk and reconciliation problems that no software can fix.

The Result for Finance Teams Who Get It Right

The franchise finance manager from the opening of this article finished in six days because her royalty reconciliation had been automated. The balances agreed at source. She spent her time reviewing the output rather than building it.

For franchise groups at five entities or more, that shift — from building consolidations to reviewing them — is the measurable outcome of a well-structured consolidation process. The franchise group’s consolidation is never simple. But it can be reliable, repeatable, and fast.

Connect your franchise group entities and produce your first consolidated set of accounts — no spreadsheets required.