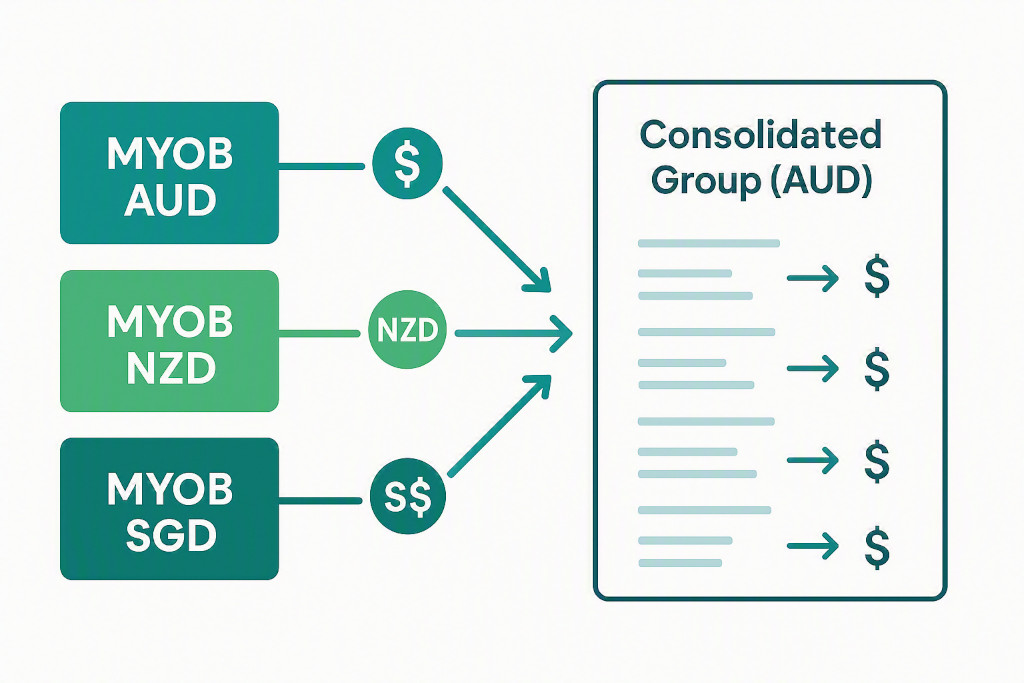

The CFO of a Perth-based services group recently described their month-end process to us: three MYOB files, three currencies, and a spreadsheet that takes two finance staff four days to reconcile. Every month, they manually pull trial balances from each entity, apply exchange rates, rebuild the consolidated P&L and balance sheet from scratch, and then spend another day chasing a balance sheet that won’t balance because the cumulative translation adjustment wasn’t carried forward correctly.

If your group runs entities across Australia, New Zealand, Singapore, the UK, or any other currency jurisdiction using MYOB, you will recognise this problem immediately. MYOB is excellent accounting software for individual entities. But MYOB multi-currency consolidation — the process of translating foreign subsidiary financials into your group’s presentation currency and eliminating intercompany transactions across those entities — is simply not something MYOB is designed to do.

This article explains what the standards require, where MYOB’s limitations sit, and how growing multi-currency groups are solving this without replacing their accounting software.

Consolidate your MYOB entities in minutes.

BrizoConsol connects to MYOB and automates your group financial statements.

Why Multi-Currency Consolidation Is Different from Single-Currency Consolidation

When all your entities operate in the same currency, consolidation is primarily about eliminations — removing intercompany sales, loans, and dividends so that the group accounts reflect only transactions with third parties. Challenging, but tractable with the right tools.

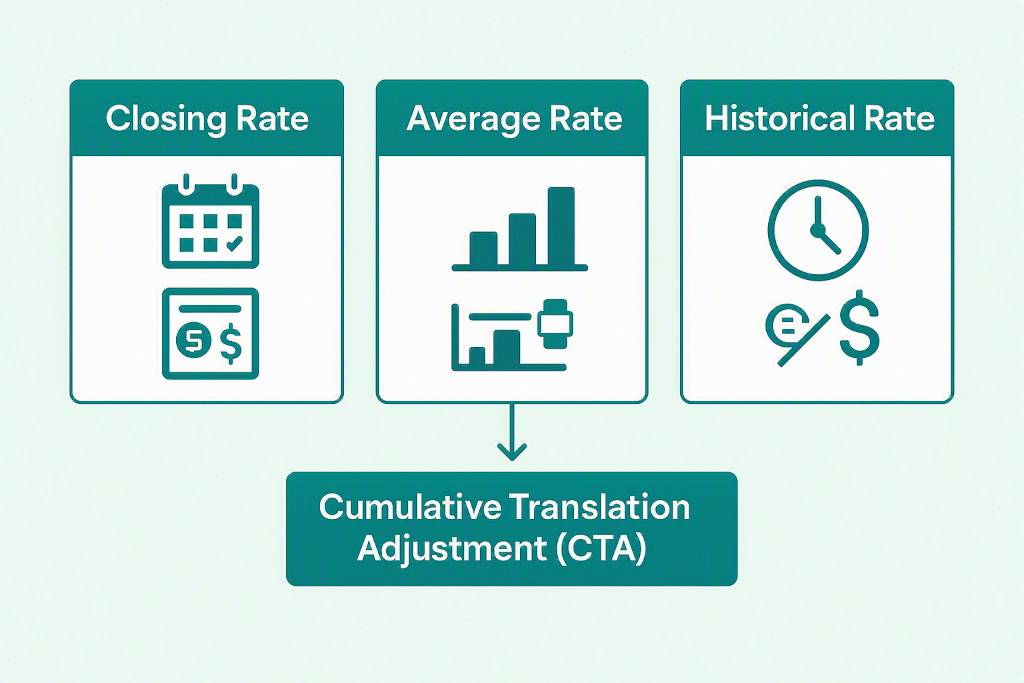

Add a foreign subsidiary and the complexity multiplies. Before you can even begin eliminations, you must translate every line of every subsidiary’s trial balance into your group’s presentation currency. And not at a single rate — IAS 21 (The Effects of Changes in Foreign Exchange Rates) requires three different rates depending on what you’re translating:

- Balance sheet items (assets and liabilities): closing rate at the reporting date

- Income statement items (revenue, expenses): average rate for the period

- Equity items (share capital, retained earnings brought forward): historical rate at the date the equity arose

The difference between translating equity at historical rates and assets at closing rates creates what is known as the Cumulative Translation Adjustment (CTA) — a balancing figure that sits in other comprehensive income within group equity. Getting the CTA right at consolidation is one of the most frequently mishandled areas in group reporting, particularly for groups doing this manually.

The Three Translation Rates Every Group Must Apply

To make this concrete, consider how these rates apply in practice. Assume your NZ subsidiary reports in NZD and your group presents in AUD. At 30 June:

| Item | Rate Applied | Rate Used |

|---|---|---|

| Trade receivables (NZD 850,000) | Closing rate | 0.9100 |

| Property, plant & equipment (NZD 1,200,000) | Closing rate | 0.9100 |

| Revenue (NZD 3,400,000) | Average rate (FY) | 0.9050 |

| Operating expenses (NZD 2,650,000) | Average rate (FY) | 0.9050 |

| Share capital (NZD 500,000) | Historical rate (date of incorporation) | 0.8700 |

| Retained earnings b/f (NZD 620,000) | Historical rate (prior year closing) | 0.8950 |

The translated balance sheet will not automatically balance because assets translated at the closing rate will differ from equity translated at historical rates. The CTA absorbs this difference and is recognised in equity — not in the P&L. This is a deliberate accounting treatment; exchange rate movements on the net investment in a foreign operation are unrealised and should not flow through profit or loss until the subsidiary is disposed of.

The CTA is not an error. If your consolidated balance sheet balances without a CTA line in equity, and you have foreign subsidiaries, something has been translated incorrectly — most commonly, prior year retained earnings applied at the wrong rate.

Where MYOB Falls Short for Multi-Currency Groups

MYOB handles foreign currency at the transaction level well. You can record invoices in NZD or SGD, apply exchange rates, and see the revaluation gains and losses within each entity. That’s entity-level foreign currency — and MYOB does it adequately.

What MYOB cannot do is consolidation-level currency translation. Specifically:

- MYOB has no mechanism to extract a subsidiary’s trial balance and translate it at three different rates simultaneously

- There is no group-level CTA calculation or running balance tracked across periods

- Intercompany eliminations across entities in different currencies require manual FX adjustment before the elimination can be posted

- There is no consolidated P&L or balance sheet that aggregates translated subsidiary figures automatically

- Each month, prior period CTA balances must be manually carried forward — a source of frequent error

As described in detail in our article on group financials MYOB can’t produce, these aren’t edge cases — they are the standard requirements of any group with foreign operations. The result for most MYOB-based groups is a consolidation spreadsheet that grows in complexity every year, becomes increasingly fragile, and takes days rather than hours to produce.

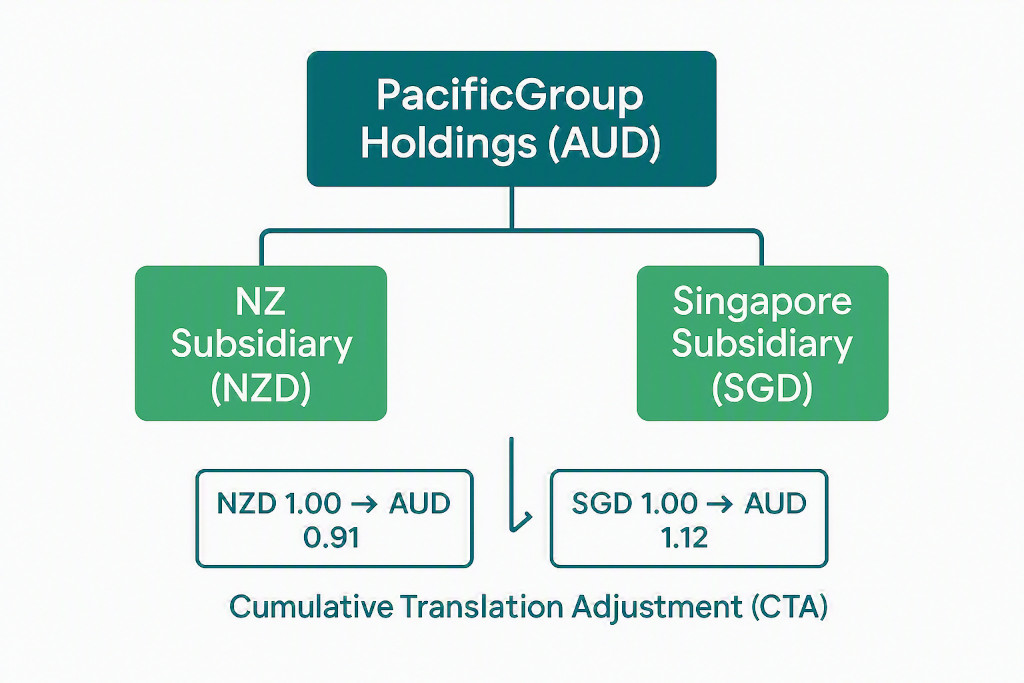

PacificGroup: A Worked Translation Example

Take PacificGroup Holdings, an Australian professional services business with three entities: the Sydney-based parent (AUD), a Wellington consulting practice (NZD), and a Singapore advisory business (SGD). All three run MYOB. The group presents consolidated accounts in AUD.

At 31 December, the NZ subsidiary reports the following trial balance in NZD:

| Line Item | NZD | Rate Type | Rate | AUD |

|---|---|---|---|---|

| Cash & receivables | 480,000 | Closing | 0.9100 | 436,800 |

| Fixed assets (net) | 920,000 | Closing | 0.9100 | 837,200 |

| Trade payables | (210,000) | Closing | 0.9100 | (191,100) |

| Revenue | 1,840,000 | Average | 0.9040 | 1,663,360 |

| Expenses | (1,420,000) | Average | 0.9040 | (1,283,680) |

| Share capital | (300,000) | Historical | 0.8650 | (259,500) |

| Retained earnings b/f | (310,000) | Historical | 0.8910 | (276,210) |

| CTA (balancing figure) | — | — | — | (126,870) |

The AUD 126,870 CTA sits in group equity as other comprehensive income. It is not a profit, not an error, and not discretionary. The same exercise must then be repeated for the Singapore subsidiary in SGD, with its own closing rate, average rate, and historical rate for equity. The two CTAs are accumulated and disclosed separately in the group’s statement of changes in equity.

Now consider that the group also has an intercompany management fee from the Sydney parent to Wellington of NZD 120,000. That fee must be eliminated — but first it must be restated in AUD at the rate at which it was recorded in each entity, and any FX difference on the intercompany balance must itself be eliminated. This is where manual processes become genuinely error-prone.

How BrizoConsol Handles MYOB Multi-Currency Consolidation

BrizoConsol connects directly to each MYOB entity via API, pulling live trial balances each time a consolidation is run. Once entities are mapped to a common chart of accounts, the platform applies IAS 21 translation rules automatically:

- Balance sheet lines are translated at the closing rate fetched or entered for the period

- P&L lines are translated at the average rate for the period

- Equity brought-forward balances are translated at their historical rates, which are set on first connection and updated as equity movements occur

- The CTA is calculated, tracked, and carried forward automatically each period

Intercompany eliminations — management fees, intercompany loans, dividends — are handled after translation, with BrizoConsol reconciling the FX difference on intercompany balances and posting the elimination net of any currency mismatch. The result is a consolidated P&L, balance sheet, and cash flow in the group’s presentation currency, with a full audit trail from consolidated line to source transaction in each MYOB entity.

For groups running a structured multi-entity month-end close, this compresses what was previously a multi-day spreadsheet exercise into a process that can be completed in under an hour — and repeated consistently every period without risk of prior-period rates being applied incorrectly.

Practical Considerations Before You Start

If you are setting up multi-currency consolidation for the first time, several decisions need to be made upfront:

Presentation currency. Choose the currency in which consolidated accounts will be presented. For most Australian groups with overseas entities, this will be AUD, but it need not be — some groups present in USD or GBP depending on where their investors or lenders are domiciled.

Functional currency per entity. Each subsidiary’s functional currency is the currency of the primary economic environment in which it operates — typically the currency in which it earns revenue and pays expenses. This is usually obvious (the NZ subsidiary earns and pays in NZD) but can require judgement for entities that operate across multiple currencies.

Historical rates for existing equity. When you first connect a foreign subsidiary to your consolidation tool, you need to establish the historical AUD-equivalent of its opening equity. This is a one-time exercise that requires care — particularly for older subsidiaries with accumulated retained earnings across many years at varying rates.

Average rate methodology. Some groups use a simple arithmetic average of month-end closing rates; others use a weighted average based on transaction volume. The method should be applied consistently and disclosed. BrizoConsol supports both approaches.

Note: This article describes the requirements under IAS 21 as adopted in Australia and internationally. Groups reporting under US GAAP should refer to ASC 830, which follows similar principles but with some differences in treatment for highly inflationary economies. Always confirm the applicable standard with your auditor.

Moving Beyond the Spreadsheet

The spreadsheet consolidation model that most MYOB-based groups rely on doesn’t fail catastrophically — it fails gradually. Rates get applied inconsistently, CTA balances drift, and the reconciliation that used to take two days starts taking four. By the time the problem is acute, the finance team has lost months of close time to a process that should be largely automated.

MYOB remains a strong choice for entity-level accounting, particularly for Australian and New Zealand businesses. The gap is not within MYOB but above it — at the consolidation layer, where multi-currency translation, intercompany eliminations, and group reporting need to happen across entities that MYOB was never designed to connect.

That is the gap BrizoConsol fills: a direct API connection to each MYOB entity, IAS 21-compliant currency translation applied automatically, and a consolidated set of accounts produced in the group’s presentation currency — every period, consistently, with a full audit trail.

Consolidate Your MYOB Entities Across Currencies

BrizoConsol connects directly to your MYOB files, handles multi-currency translation automatically, and produces consolidated accounts in your group’s presentation currency — without replacing MYOB. Start Free Trial