When a group’s holding company acquires a controlling interest in another business, a new figure tends to appear on the consolidated balance sheet that can unsettle finance directors who encounter it for the first time: goodwill. It does not sit in any individual entity’s accounts. It cannot be touched or sold independently. Yet under most accounting standards, it is required to be recognised, tested annually for impairment, and in some frameworks, amortised over its useful life.

Goodwill in group consolidation arises from a straightforward principle: the price paid to acquire a business almost always exceeds the fair value of the identifiable net assets being acquired. The difference is the acquirer’s assessment of value that cannot be separately identified — brand reputation, customer relationships, workforce capability, synergies. That excess is goodwill.

This guide explains how goodwill arises, how to calculate it correctly at acquisition, how it is treated subsequently under IFRS, UK GAAP, and US GAAP, and what finance teams need to track in their consolidation process once it is on the balance sheet.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

What Is Goodwill in the Context of Group Consolidation?

Goodwill is an intangible asset that appears only in the consolidated financial statements — not in the individual entity accounts of either the parent or the acquired subsidiary. It represents the premium paid over the fair value of the net identifiable assets of the acquired business at the date of acquisition.

Under IFRS 3 Business Combinations, FRS 102, and ASC 805 (US GAAP), goodwill is calculated at the acquisition date and recognised on the consolidated balance sheet from that point forward. It is tested for impairment at least annually — and more frequently if there are indicators of impairment — and under UK GAAP it is also amortised over its estimated useful life.

Goodwill in group consolidation is not the same as internally generated goodwill, which cannot be recognised under any major accounting framework. Only goodwill arising on the acquisition of a business is recognised in the consolidated accounts.

How to Calculate Goodwill at Acquisition

The basic goodwill formula under IFRS 3 and FRS 102 is:

Goodwill = Consideration Transferred + Fair Value of NCI + Fair Value of Previously Held Interest − Fair Value of Net Identifiable Assets Acquired

In a straightforward acquisition with no previously held interest:

Goodwill = Consideration Transferred + Fair Value of NCI − Fair Value of Net Identifiable Assets

Each component requires careful treatment:

- Consideration transferred is the total acquisition price — cash paid, shares issued at fair value, deferred or contingent consideration at fair value at the acquisition date, and any other assets transferred.

- Fair value of NCI (non-controlling interest) is the share attributable to minority shareholders. Under the full goodwill method (the default under IFRS 3), this is measured at the fair value of the NCI’s proportionate share of the acquired business. Under the partial goodwill method (permitted as an accounting policy choice under IFRS 3), NCI is measured at its proportionate share of the fair value of net identifiable assets only.

- Fair value of net identifiable assets is the fair value of all the acquired entity’s identifiable assets minus its liabilities at the acquisition date. This is not book value — it requires a fair value exercise, often involving independent valuers for property, intangibles, and certain liabilities.

For a detailed walkthrough of how non-controlling interest is calculated and presented in the consolidated balance sheet, the post on calculating non-controlling interest in financial consolidation covers both the full and partial goodwill methods in depth.

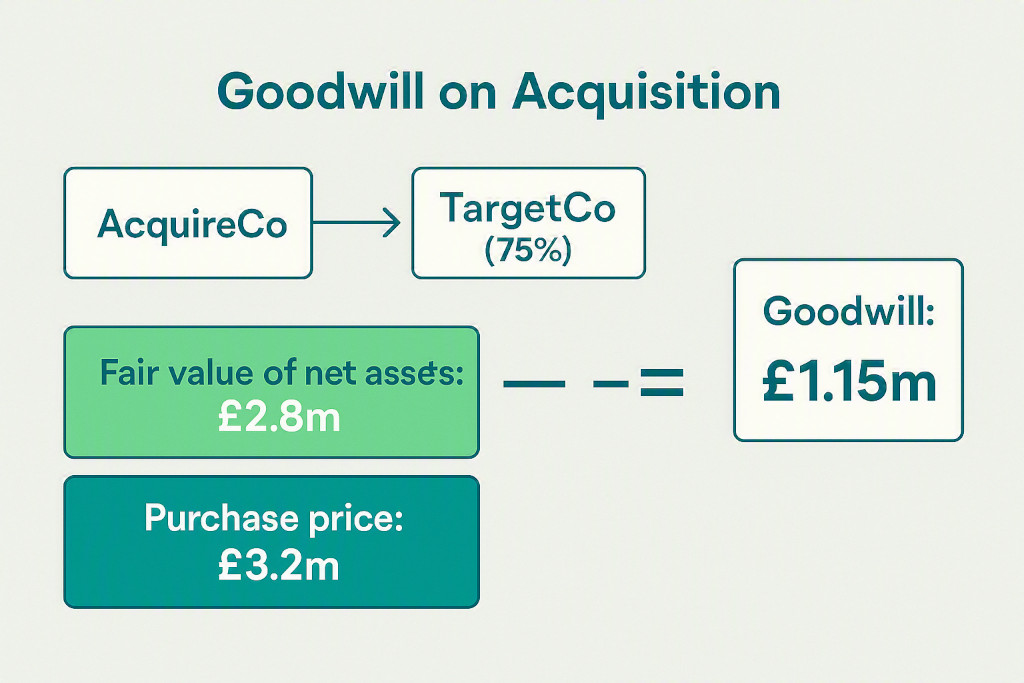

Practical Example: Goodwill on a 75% Acquisition

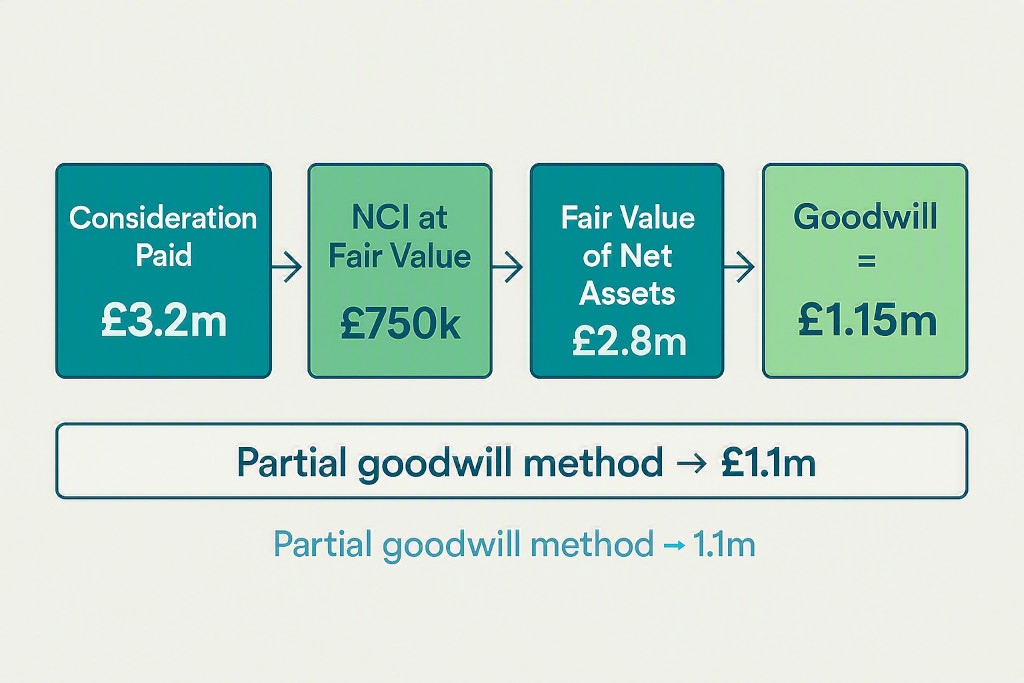

AcquireCo Ltd purchases 75% of TargetCo Ltd on 1 January for £3.2 million in cash. At the acquisition date, the fair value of TargetCo’s net identifiable assets is determined to be £2.8 million. The fair value of the 25% non-controlling interest is assessed at £750,000 (implying a total enterprise value of £3.95m).

The goodwill calculation under the two permitted methods:

| Component | Full Goodwill Method | Partial Goodwill Method |

|---|---|---|

| Consideration transferred (cash) | £3,200,000 | £3,200,000 |

| NCI — full goodwill (at fair value) | £750,000 | — |

| NCI — partial goodwill (25% × £2.8m) | — | £700,000 |

| Total | £3,950,000 | £3,900,000 |

| Less: fair value of net identifiable assets | (£2,800,000) | (£2,800,000) |

| Goodwill recognised | £1,150,000 | £1,100,000 |

The journal entry to recognise the acquisition in the consolidated accounts at the acquisition date:

Acquisition date consolidation entry (full goodwill method)

Dr Net identifiable assets of TargetCo £2,800,000

Dr Goodwill £1,150,000

Cr Cash consideration paid £3,200,000

Cr Non-controlling interest £750,000

Being: recognition of acquisition of 75% of TargetCo Ltd at 1 January

“The most common error at acquisition is using TargetCo’s book value of net assets rather than the acquisition-date fair value. A piece of freehold property carried at £400,000 on TargetCo’s books might have a fair value of £650,000. Using book value understates net assets by £250,000 and overstates goodwill by the same amount.”

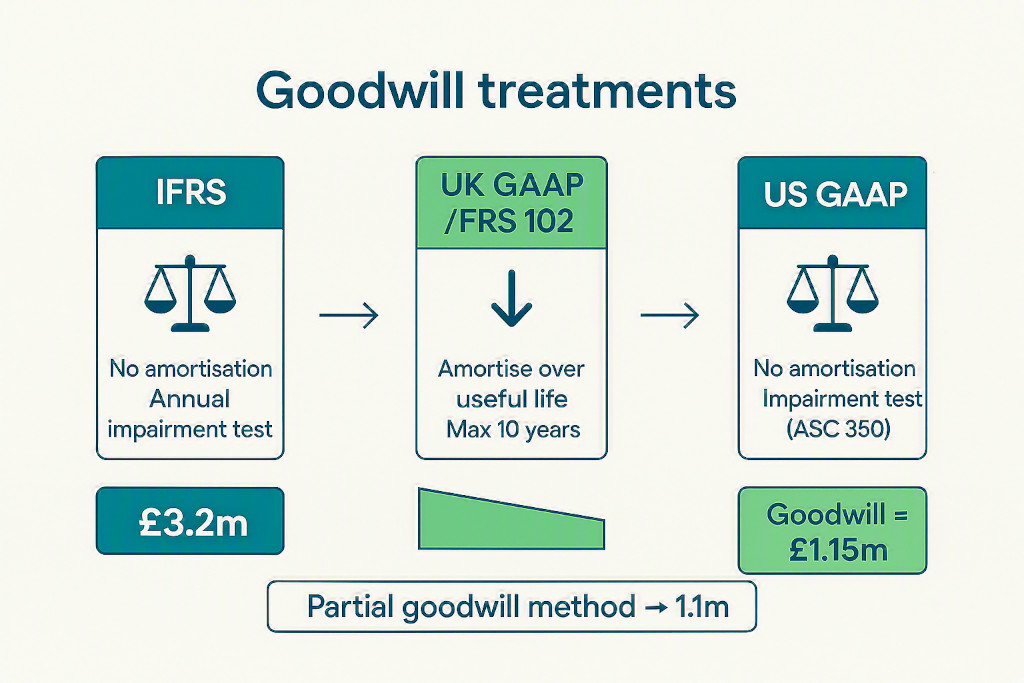

Goodwill After Acquisition: Amortisation and Impairment

Once goodwill is recognised, its subsequent treatment depends on the accounting framework the group applies.

IFRS (IAS 36 / IFRS 3)

Under IFRS, goodwill is not amortised. Instead, it is allocated to cash-generating units (CGUs) — the smallest identifiable groups of assets that generate largely independent cash inflows — and tested for impairment at least once a year, and additionally whenever there is an indication of impairment. If the recoverable amount of a CGU falls below its carrying amount (including allocated goodwill), the difference is recognised as an impairment loss in the consolidated P&L. Goodwill impairment cannot be reversed in subsequent periods.

UK GAAP (FRS 102)

Under FRS 102, goodwill is treated as a finite-life intangible asset and amortised over its useful economic life. Where that life cannot be reliably estimated, a maximum of ten years is applied. Goodwill is also subject to an annual impairment review in the first year after acquisition, and subsequently whenever there are indicators of impairment. Unlike IFRS, UK GAAP allows impairment reversals on goodwill in limited circumstances.

US GAAP (ASC 350)

The US GAAP treatment of goodwill aligns more closely with IFRS than with UK GAAP: goodwill is not amortised but is subject to annual impairment testing. Public entities test at the reporting unit level; private entities may elect a simplified amortisation approach under ASU 2014-02, amortising goodwill on a straight-line basis over ten years.

Negative Goodwill — What Happens When Goodwill Is Negative?

Occasionally, the calculation produces a negative figure — the consideration paid is less than the fair value of the net identifiable assets acquired. This is known as negative goodwill, or a bargain purchase.

Before recognising negative goodwill, the acquirer is required to reassess the fair values of all assets and liabilities and confirm the consideration transferred. If the negative figure persists after reassessment, it is recognised immediately as a gain in the consolidated P&L under both IFRS 3 and ASC 805. Under FRS 102, negative goodwill is presented separately on the consolidated balance sheet and released to profit over the periods the acquired assets are expected to be recovered — a different treatment that reflects FRS 102’s more cautious approach.

Bargain purchases are uncommon in arm’s length transactions and often reflect distressed sale conditions, forced disposals, or errors in the initial fair value exercise.

How Consolidation Software Handles Goodwill

Goodwill in group consolidation sits entirely outside the individual entity accounting records. It is calculated at the group level, maintained in the consolidated working papers, and must be re-tested each year. For groups managing their consolidation in a spreadsheet, this creates a persistent risk: the goodwill schedule lives in a file that may not be properly version-controlled, the CGU allocation is rarely revisited, and the impairment trigger review is easy to overlook at a busy year-end.

BrizoConsol supports goodwill management through the group consolidation journals layer. Finance teams can post the initial goodwill recognition as a consolidation journal at the acquisition date, record any subsequent amortisation charges (for FRS 102 groups) as recurring journals, and capture impairment write-downs with a full audit trail. Because BrizoConsol connects directly to each entity’s accounting system via API, the net asset position of the acquired subsidiary is always current — making the recoverable amount assessment against carrying value a comparison of live figures rather than a period-end exercise in spreadsheet reconstruction.

For groups that are building out their consolidation process from scratch — or replacing a manual approach — the guide on what financial consolidation software does and why groups need it explains the full scope of what a consolidation tool manages beyond the individual entity books.

Common Mistakes in Goodwill Accounting

A few errors appear with enough regularity to be worth flagging explicitly:

- Using book value instead of fair value. The goodwill calculation requires the fair value of net identifiable assets at the acquisition date, not the carrying amount in the acquired entity’s accounts. Failing to restate assets to fair value — particularly property, plant and equipment, customer relationships, and brand intangibles — inflates goodwill and understates identifiable intangible assets.

- Ignoring deferred tax on fair value adjustments. When an asset is restated to fair value at acquisition, the difference between the new carrying amount and the tax base of the asset gives rise to a deferred tax liability. This deferred tax affects both the net identifiable assets figure and, consequently, the goodwill calculation.

- Failing to allocate goodwill to CGUs promptly. Under IFRS, goodwill must be allocated to CGUs no later than the end of the first annual reporting period after the acquisition. Delay makes the impairment test meaningless and creates a compliance exposure.

- Treating goodwill impairment as a timing difference. Once goodwill is impaired, the write-down is permanent under IFRS and US GAAP. Restoring it in a subsequent year is not permitted, regardless of business recovery.

- Omitting NCI’s share of goodwill under the full goodwill method. Under the full goodwill method, the NCI is measured at fair value, which attributes a portion of goodwill to the minority. Groups that default to the partial goodwill method without a deliberate accounting policy choice may understate the NCI balance on the consolidated balance sheet.

Goodwill in group consolidation is one of the areas where the gap between theory and practice is widest. The principles are well established, but the execution — fair value exercises, CGU allocation, annual impairment assessments — requires consistent discipline across reporting periods. For groups using consolidation adjustments of this kind alongside intercompany eliminations and multi-currency translation, maintaining a structured, auditable approach to each adjustment is what separates a clean group close from one that unravels under scrutiny.

Manage Goodwill and All Your Consolidation Adjustments in One Place

BrizoConsol handles acquisition journals, recurring amortisation, impairment write-downs and intercompany eliminations — all with a full audit trail, connected directly to your accounting platforms. Start Free Trial