Every finance team managing a multi-entity group knows the feeling. Month-end arrives, the trial balances are in, and then comes the part nobody looks forward to: hunting down every intercompany transaction, matching it against the counterparty’s records, resolving the inevitable discrepancies, and posting the elimination journals — all before the consolidated accounts can be produced. In a group with three entities, this process is manageable. In a group with eight, twelve, or twenty, it becomes one of the most time-consuming and error-prone tasks in the entire reporting cycle. This post explains what intercompany elimination software actually does, why manual approaches break down at scale, and what to look for when evaluating purpose-built tools.

What Intercompany Elimination Actually Involves

Before examining the software options, it is worth being precise about what intercompany elimination means and why it is technically demanding. When one entity within a group sells goods or services to another, both sides of that transaction are recorded in the respective entity’s accounts — revenue in the selling entity, cost of goods or expenses in the buying entity. From a group perspective, those are internal flows. They did not generate any economic activity outside the group, and if they are left in the consolidated financials, the group’s revenue and costs will be overstated by exactly the amount of those internal transactions.

The same logic applies to intercompany loans, where both a receivable and a payable appear on the group balance sheet; to management fees, where an income line and an expense line cancel each other out; and to dividend payments between entities. Each of these must be eliminated — meaning both sides must be identified and removed from the consolidated financials — before the group accounts reflect economic reality. This is not optional under any recognised accounting standard. IFRS 10, UK GAAP, and US GAAP all require that intercompany balances and transactions be fully eliminated on consolidation.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

The Matching Problem

The reason elimination is difficult in practice is not conceptual — it is practical. The two sides of an intercompany transaction are recorded in different entities, often in different accounting systems, sometimes in different currencies, and frequently at slightly different times. A management fee invoiced by the parent in one period may be recorded as an expense by the subsidiary in the following period. A loan repayment processed on 30 June in one system may appear in the counterparty’s records on 1 July. These timing differences mean that even a well-run group will have intercompany balances that do not agree perfectly at any given reporting date, and the process of reconciling and resolving those differences is where the hours accumulate.

Why Manual Elimination Fails at Scale

Many finance teams approach intercompany elimination through a combination of spreadsheets and manual journal entry. For small groups, this works well enough. The volume of intercompany transactions is low, the finance team knows each entity intimately, and a diligent accountant can complete the eliminations in a few hours. But the workload does not scale linearly with the number of entities. It scales more steeply than that, because the number of possible intercompany relationships grows with every entity added to the group.

A group of four entities has up to twelve directional intercompany relationships. A group of ten has up to ninety. Each of those relationships may have multiple transaction types — trading, loans, fees, dividends — and each transaction type must be tracked, matched, and eliminated separately. The spreadsheet model that served a three-entity group reliably will begin to crack under the weight of a ten-entity group, and the cracks tend to appear in the worst possible places: undetected mismatches that flow through to the consolidated balance sheet, elimination journals that double-count one side, or adjustments that are correctly made in one period but reversed inconsistently in the next.

“The manual elimination process is one of the leading sources of restatements in consolidated accounts for mid-market groups — not because finance teams lack skill, but because the volume of matching and cross-checking required simply exceeds what can be reliably managed without dedicated tooling.”

There is also a personnel risk. When the elimination process lives in spreadsheets maintained by one or two individuals, the institutional knowledge of how it works lives with those individuals. A team change, a period of illness, or a significant growth in the group’s entity count can expose how fragile the underlying process really is. Intercompany elimination software addresses this by encoding the process in a structured, auditable system that does not depend on any single person’s memory or undocumented methodology.

Currency Complexity Compounds the Problem

For groups with entities operating in different currencies, the matching challenge is compounded by translation differences. An intercompany loan denominated in US dollars will appear on both sides of the group balance sheet, but the two entities may translate it at slightly different rates depending on when the rate was last updated in their respective systems. This creates a currency-driven mismatch that is not a bookkeeping error — it is a structural feature of multi-currency groups — and it requires specialist handling during the elimination process. In a manual environment, this is typically addressed through a series of manual adjustments that are cumbersome to prepare and even more cumbersome to audit.

How Intercompany Elimination Software Works in Practice

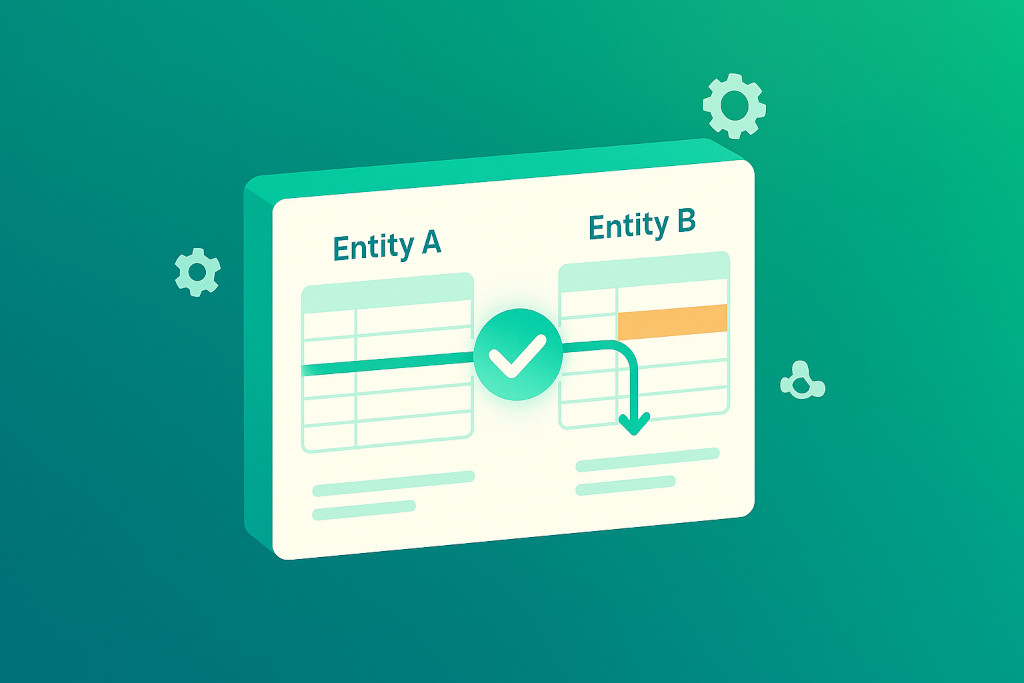

Purpose-built intercompany elimination software approaches the problem from a fundamentally different direction. Rather than asking the accountant to match transactions manually and post journals based on that matching, it creates a structured intercompany register — a single view of all transactions between group entities — and automates the matching and elimination process against that register.

In BrizoConsol, this works through direct API connections to each entity’s accounting platform. BrizoConsol connects natively to Xero, QuickBooks, MYOB, and Zoho Books, pulling trial balances and transaction data automatically without requiring CSV exports or manual data entry. Once the data is in the consolidation environment, the system identifies intercompany account codes, matches transactions between entities, flags discrepancies for review, and applies elimination entries automatically where the match is clean.

Automatic Elimination Rules

For groups with recurring intercompany transactions — a monthly management fee from parent to subsidiaries, for example, or a standing intercompany loan — BrizoConsol supports configurable auto-elimination rules. These rules define the intercompany relationship, the account codes on each side, and the elimination treatment, and then apply the elimination automatically at each reporting period without requiring any manual intervention. The accountant reviews the result rather than performing the elimination from scratch, which transforms a multi-hour monthly task into a brief confirmation exercise.

Mismatch Investigation and Resolution

Where intercompany balances do not match exactly — which, in practice, is more often than not — BrizoConsol surfaces the discrepancy clearly and provides the context needed to investigate it. The accountant can see both sides of the transaction, the amounts as reported by each entity, the difference, and a timeline of when each entry was posted. This makes it straightforward to determine whether the discrepancy is a timing difference that should be adjusted, a genuine bookkeeping error in one of the entities, or a known currency translation effect that should be handled through the group’s established methodology. The audit trail for every decision is maintained within the platform, creating a clear and reviewable record of how each elimination was handled.

The Audit Trail Advantage

One of the most underappreciated benefits of dedicated group consolidation software is what it does for the audit process. When intercompany eliminations are performed in spreadsheets, auditors must rely on the finance team to reconstruct and explain every elimination journal. This is time-consuming for both parties and introduces the risk that the reconstruction does not perfectly match what was actually done. When eliminations are performed within a structured platform like BrizoConsol, every elimination journal is recorded with a timestamp, a rule reference or manual justification, and the source data on both sides of the transaction. Auditors can review the elimination register directly, and the finance team can respond to queries by pointing to specific records rather than excavating spreadsheet versions.

This matters increasingly as groups grow and come under greater scrutiny from investors, lenders, and regulators. A consolidated balance sheet supported by a clear, automated elimination record is a materially stronger document than one supported by a collection of manually maintained worksheets, and the difference becomes visible the moment any external party starts asking questions about how the numbers were produced.

What Good Intercompany Elimination Software Looks Like

When evaluating financial consolidation software specifically for its intercompany elimination capability, there are several characteristics that distinguish tools built for the job from those that handle elimination as an afterthought.

- Direct data connections, not CSV imports. Manually exporting and importing trial balances introduces lag and version risk. Software that connects via API to the underlying accounting platforms — as BrizoConsol does with Xero, QuickBooks, MYOB, and Zoho Books — ensures the data in the consolidation environment is always current and complete.

- Intercompany register with both-sides visibility. The tool should show both sides of every intercompany relationship in a single view, making it immediately obvious where matches are clean and where discrepancies exist.

- Configurable auto-elimination rules. Recurring transaction types should be eliminable automatically, with the accountant reviewing rather than re-performing the work each period.

- Multi-currency handling within the elimination process. The tool should handle currency translation differences within the elimination workflow, not require manual adjustments outside the system.

- Full audit trail. Every elimination journal — automatic or manually posted — should carry a timestamped record of what was eliminated, on what basis, and by whom.

- Integration with the wider consolidation process. Elimination is one step in a broader consolidation workflow that also includes chart of accounts mapping, currency translation, NCI calculation, and financial statement production. The best intercompany elimination software is part of a complete group consolidation platform, not a standalone module that requires separate tools for the surrounding steps.

From Monthly Ordeal to Routine Process

The measure of good intercompany elimination software is not what it does once — it is what it makes possible every month. When elimination is manual, it is a task that must be approached fresh each reporting period, with the attendant risk that something is missed, misstated, or inconsistently handled relative to the prior period. When it is automated and structured, it becomes a routine confirmation exercise: the system runs the eliminations, the accountant reviews the results and investigates any flagged discrepancies, and the consolidated accounts are produced on a consistent, auditable basis.

For accounting practices managing multiple clients with multi-entity structures, this shift in the character of the work is transformative. The time freed by automating routine elimination work can be redirected toward the analytical and advisory tasks that genuinely require professional judgement — and that clients are willing to pay for. For in-house finance functions, the benefit is reliability: a consistent elimination process that does not depend on any single team member and that scales cleanly as the group adds entities, enters new markets, or takes on additional intercompany arrangements.

Intercompany elimination is one of the most technically demanding steps in group consolidation, and it is one of the steps where manual approaches are most likely to introduce errors that are difficult to detect and expensive to correct. Purpose-built group consolidation software — with robust intercompany elimination at its core — is the practical solution that growing groups and the accountants who support them have been waiting for.