Zoho Books is one of the most capable cloud accounting platforms in its class — particularly for small and mid-sized businesses operating across the Asia-Pacific, Middle East, and South Asian markets where Zoho has strong penetration. It handles invoicing, bank feeds, payroll integrations, GST and VAT compliance, and entity-level financial reporting with impressive depth. For a single organisation, it covers almost everything a finance team needs.

The challenge begins the moment that single organisation becomes two or three. A holding company acquires a subsidiary. A founder launches a second operating entity in a different country. A regional group structure emerges with separate Zoho Books organisations for each legal entity. At that point, the question that every multi-entity finance team eventually has to answer arrives: how do we get a consolidated view of the group? And the honest answer, when it comes to Zoho Books alone, is that you cannot — at least not without significant manual work.

What Zoho Books Is Designed to Do

Zoho Books is built to manage the accounting of a single organisation. It does this well: chart of accounts, journal entries, bank reconciliation, accounts payable and receivable, tax filings, and entity-level P&L, Balance Sheet, and Cash Flow reports are all handled natively and with good depth. Zoho also allows you to manage multiple organisations under a single Zoho account, making it straightforward to switch between entities without logging out and back in.

Group consolidation for Zoho Books — fast and accurate.

Connect your Zoho Books organisations and consolidate into one clean group view.

But managing multiple organisations and consolidating them are two fundamentally different things. Having access to three Zoho Books files does not mean Zoho can produce a P&L that combines all three, eliminates the transactions between them, translates foreign currency balances into a single presentation currency, and presents the result as a unified set of group financial statements. That capability does not exist in Zoho Books, regardless of which plan you are on.

What Zoho Books Cannot Do for Group Consolidation

For a group with multiple Zoho Books organisations, these are the specific gaps that emerge at the consolidation layer:

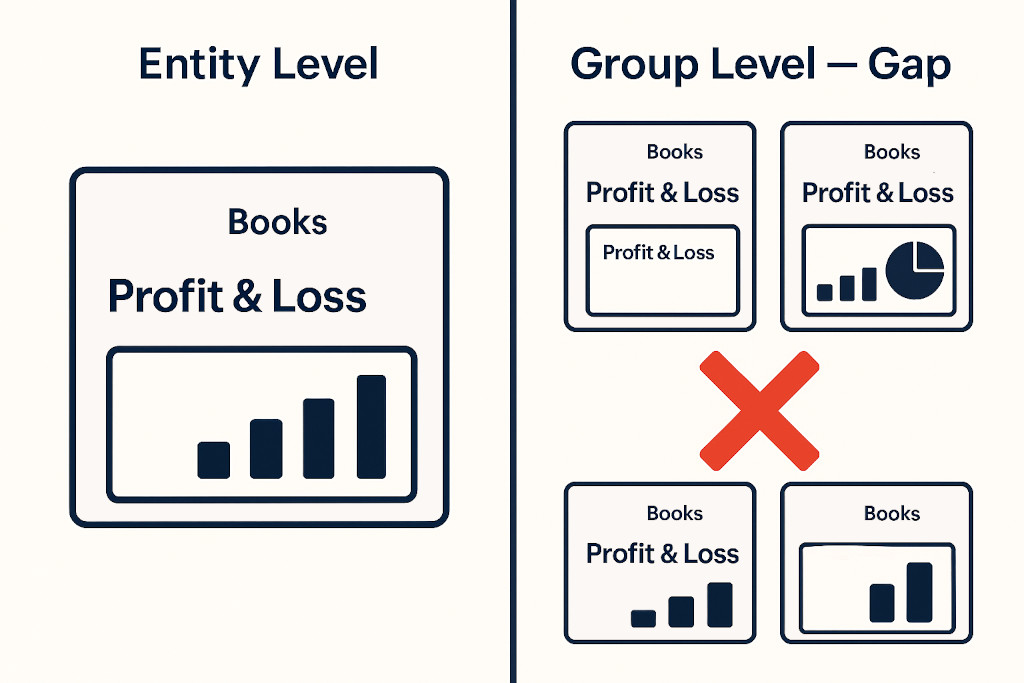

No Native Consolidated Financial Statements

There is no report in Zoho Books that aggregates revenue, expenses, assets, liabilities, or equity across multiple organisations. Group financials must be assembled externally, typically by exporting trial balances from each organisation and combining them in a spreadsheet. Every month. Every quarter. Every year-end.

No Intercompany Elimination

When one Zoho Books entity invoices another — for management fees, shared services, intercompany loans, or stock transfers — both sides of that transaction appear in each entity’s books. At the group level, these transactions need to be removed entirely: the revenue in the selling entity and the corresponding expense in the buying entity must cancel out, as must any intercompany receivables and payables on the Balance Sheet. Zoho Books does not detect, flag, or eliminate these transactions. Without manual elimination, any consolidated P&L will overstate both revenue and costs, sometimes substantially.

No Multi-Currency Group Translation

Zoho Books supports multi-currency transactions within a single organisation — you can raise invoices in foreign currencies and record bank accounts in different currencies. But it does not translate an entire organisation’s financial statements from its functional currency into a group presentation currency. A group with a parent company in India (INR), a subsidiary in the UAE (AED), and a branch in Singapore (SGD) cannot produce a currency-translated consolidated Balance Sheet from Zoho Books alone. The cumulative translation adjustment (CTA) that IFRS requires — the equity reserve that accumulates from applying different exchange rates to different balance types — does not exist in Zoho Books.

No Non-Controlling Interest

When the parent company owns less than 100% of a subsidiary, the share belonging to outside investors — the non-controlling interest (NCI) — must be separately identified in the consolidated income statement and Balance Sheet. Zoho Books has no NCI calculation capability.

No Audit Trail Outside the General Ledger

Any consolidation adjustments made in a spreadsheet leave no traceable record inside Zoho Books. When an auditor asks why a consolidated balance differs from the sum of the entity trial balances, the answer lives somewhere outside the accounting system — often in a workbook maintained by whoever handled last month’s close.

💡 The key distinction: Zoho Books gives you visibility into multiple sets of entity-level books. Zoho Books consolidation requires a layer above those books — one that brings the data together, eliminates intercompany flows, converts currencies, and produces group financials that Zoho itself cannot generate.

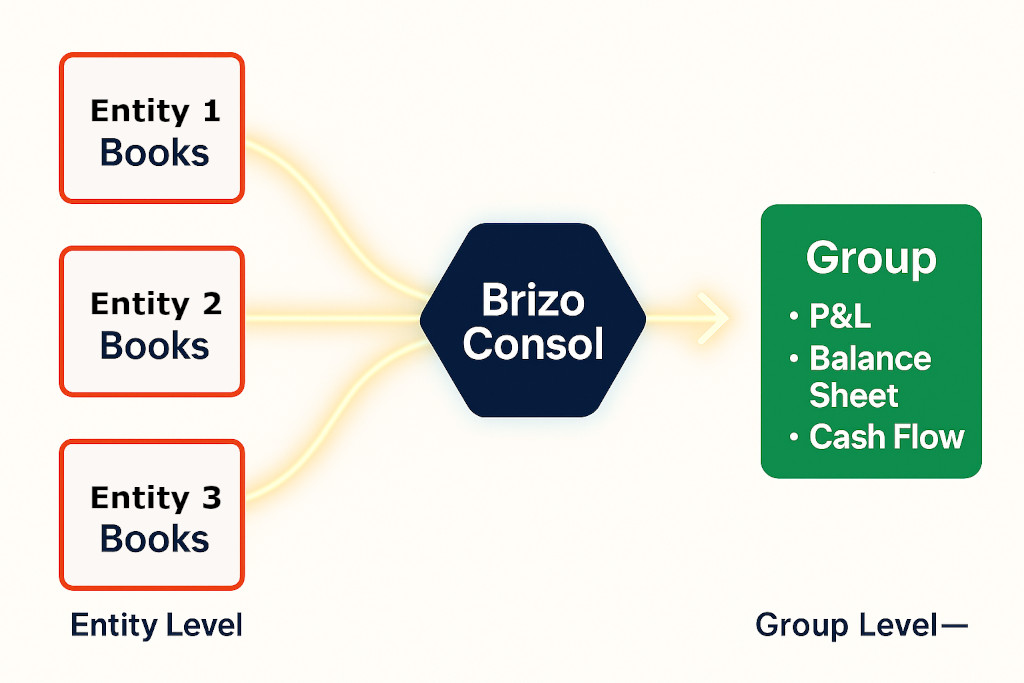

How BrizoConsol Bridges the Gap

Purpose-built consolidation software connects directly to your Zoho Books organisations and handles the consolidation layer automatically — replacing the monthly manual process with a structured, repeatable system. Here is how BrizoConsol approaches each of the gaps described above:

Direct Zoho Books API Integration

BrizoConsol connects to each of your Zoho Books organisations via the Zoho Books API. There are no CSV exports, no manual data transfers between systems. Financial data pulls automatically on a defined schedule, so the consolidated view is always current. When a transaction is updated or a period is closed in Zoho Books, the change flows through to the consolidated output without any manual re-export.

Automatic Intercompany Eliminations

BrizoConsol identifies intercompany transactions across connected Zoho Books entities and eliminates them from the consolidated view. For groups where charts of accounts are consistently structured, matching happens automatically. For recurring intercompany flows — management fees, shared cost allocations, intercompany financing — elimination rules are configured once and applied each period without manual intervention. Every elimination entry carries a full audit trail: what was eliminated, why, and when.

Multi-Currency Translation and CTA

Each Zoho Books entity’s financials are translated into the group presentation currency using the methodology required by IFRS or US GAAP: closing rate for balance sheet items, average rate for income statement items, and historical rate for equity. The cumulative translation adjustment is calculated and allocated to the correct equity line automatically. Exchange rates can be maintained within BrizoConsol for each reporting period, and all rate applications are logged and traceable. There are no manual currency worksheets to maintain and no risk of applying the wrong rate to the wrong balance type.

Consolidated Reports Available Immediately

Once the Zoho Books connections are established and the consolidation configuration is in place, BrizoConsol produces consolidated P&L, Balance Sheet, and Cash Flow statements on demand. Reports update automatically as underlying Zoho Books data changes. BrizoConsol’s Insight Package feature allows you to schedule the delivery of consolidated reports to specific recipients — board members, investors, lenders — automatically at each reporting cycle, without any manual formatting or distribution work.

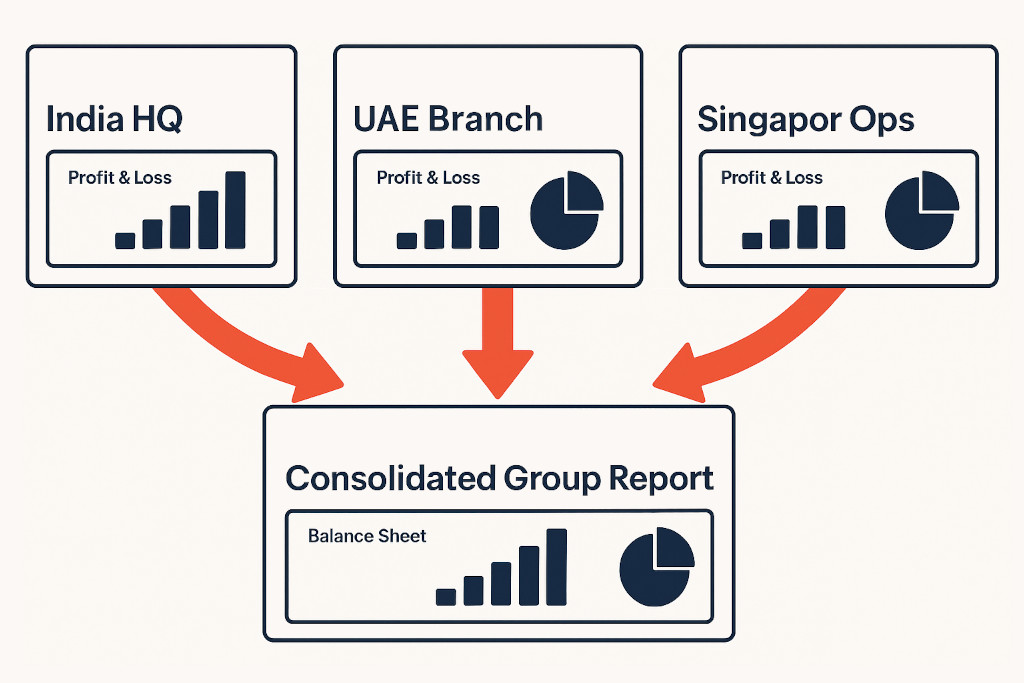

A Common Scenario: Regional Zoho Books Groups

One of the most common use cases for Zoho Books consolidation is a regional group with entities across multiple countries — often in the Asia-Pacific or Middle East, where Zoho Books has particularly strong adoption. A typical structure might include a Singapore holding company, operating subsidiaries in India and the UAE, and a smaller entity in Australia. Each runs Zoho Books in its own functional currency, and each has its own local chart of accounts shaped by local tax and reporting requirements.

In a spreadsheet consolidation, this structure requires exporting four trial balances each month, mapping each entity’s accounts to a common group structure, applying three different currency translations with three sets of exchange rates, reconciling intercompany balances across four entities, and assembling the group P&L and Balance Sheet from formulas that must be updated every period. For a group of this complexity, the monthly close consolidation typically takes two to three days of focused finance team time — and that is when everything goes smoothly.

BrizoConsol’s AI Auto-Map feature handles the account mapping step: it analyses each entity’s Zoho Books chart of accounts and suggests mappings to the common group structure automatically. The first month’s setup — connecting the entities, reviewing the account mappings, configuring intercompany relationships — typically takes a few hours. From the second month onwards, the consolidation runs with a fraction of the manual effort.

Mixed Accounting System Groups

Not every group runs entirely on Zoho Books. It is common for one entity in a group to use Zoho Books while another uses Xero, QuickBooks, or MYOB — often because different entities were set up by different accountants at different times, or because local platform preferences vary by country.

BrizoConsol connects natively to Zoho Books, Xero, QuickBooks, and MYOB within the same consolidation group. A group where the Singapore holding company uses Xero, the Indian subsidiary uses Zoho Books, and the Australian entity uses MYOB can be consolidated in a single BrizoConsol workspace. The platform normalises data from each source into a consistent structure, so the consolidation process is the same regardless of which accounting system each entity uses. Groups do not need to migrate entities onto a single platform before they can get consolidated financials.

When to Consider Consolidation Software

For groups using Zoho Books, the right time to evaluate consolidation software tends to be one of these moments: when the spreadsheet consolidation is taking more than a day per month, when intercompany transaction volumes are growing to the point where manual elimination is unreliable, when a new currency is added to the group and currency translation becomes a material part of the close process, or when an audit or board requirement raises the standard of evidence needed to support the consolidated numbers.

The benefit of addressing this sooner rather than later is that the consolidation process becomes part of the group’s operating infrastructure — repeatable, auditable, and delegable — rather than a manual exercise that depends on specific individuals and carries inherent risk each time it is performed. For growing groups, that shift typically pays for itself within a few months in reduced time cost alone.