When one company acquires another, the transaction creates a set of technical accounting requirements that will affect every group consolidation for as long as the subsidiary remains part of the group. Get the acquisition accounting right on day one, and subsequent consolidations are straightforward. Get it wrong, and the errors propagate — distorting goodwill, understating liabilities, and creating persistent reconciliation problems that compound with each reporting period.

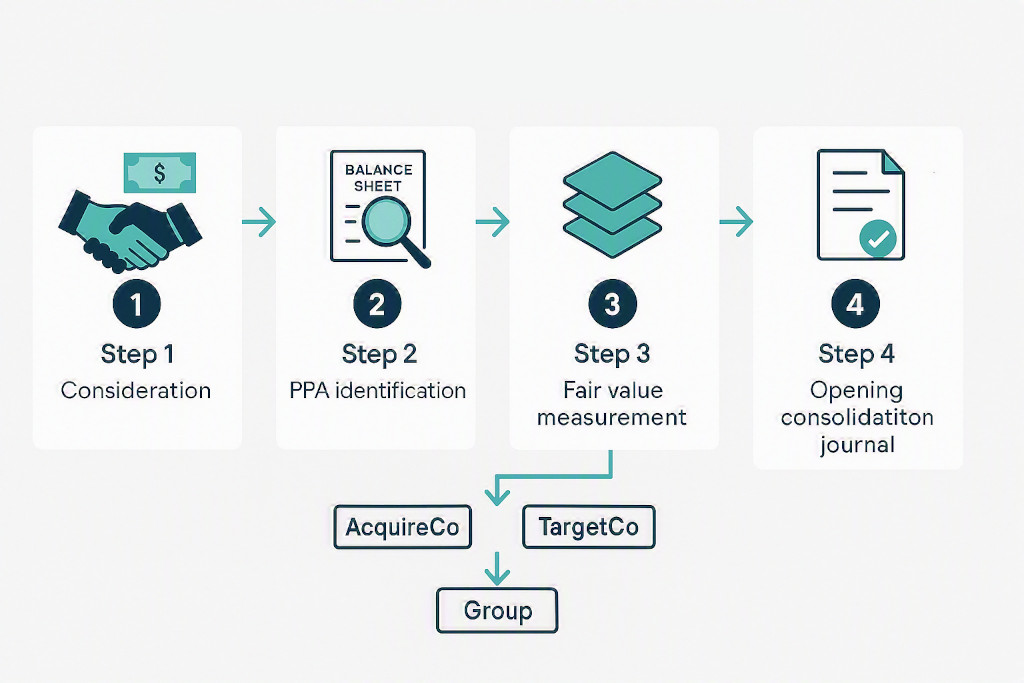

Acquisition accounting under IFRS 3 (and its US equivalent, ASC 805) follows a structured process known as the acquisition method. This post walks through that process step by step: from identifying the consideration transferred to recognising acquired intangible assets, accounting for deferred tax on fair value uplifts, and posting the opening consolidation journal. The goal is a worked example you can follow in practice, not a summary of the standard.

What Is the Acquisition Method?

IFRS 3 requires that all business combinations be accounted for using the acquisition method. This means that on the date control passes from seller to acquirer — the acquisition date — the acquiring entity must:

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

- Measure the consideration it has transferred.

- Identify and measure the fair value of all the acquiree’s identifiable assets and liabilities, including intangible assets that were not previously recognised on the acquiree’s own balance sheet.

- Measure any non-controlling interest (NCI) in the acquiree.

- Recognise goodwill (or a gain on a bargain purchase) as the residual.

The acquisition method applies whether the acquisition is for cash, shares, deferred consideration, a combination of all three, or any other form of consideration. It applies to acquisitions of 100% of an entity and to partial acquisitions where control is obtained.

Step 1 — Measure the Consideration Transferred

The consideration transferred is the fair value, at the acquisition date, of everything the acquirer gives up to obtain control. This is straightforward when the consideration is a single cash payment. It becomes more complex in common deal structures.

Deferred consideration

If part of the purchase price is payable in the future on a fixed schedule, it is discounted to present value at the acquisition date using a rate that reflects the credit risk of the arrangement. The discount unwinds as a finance charge in subsequent P&Ls.

Contingent consideration (earn-outs)

Earn-out arrangements — where additional amounts are payable if the acquired business hits revenue or profit targets — must be measured at fair value on the acquisition date and recognised as a liability (or equity, depending on the settlement mechanism). This estimate is based on a probability-weighted assessment of the range of outcomes. Unlike deferred consideration, the earn-out liability is subsequently remeasured to fair value at each reporting date, with movements recognised in profit or loss. This is a common source of surprise for acquirers who expect the liability to simply reduce as targets are or are not met.

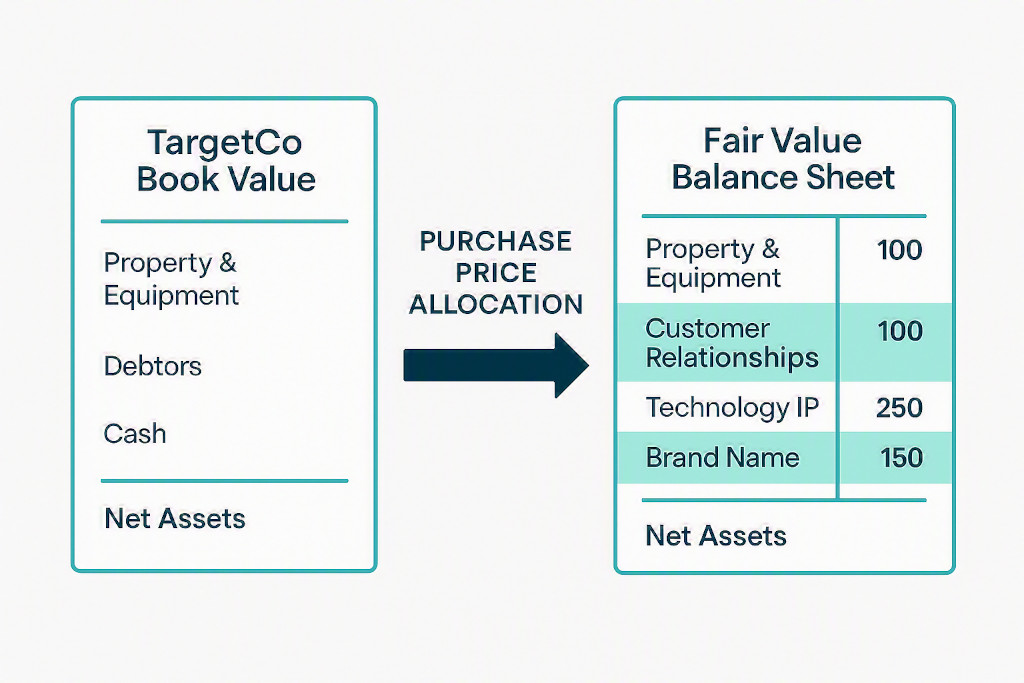

Step 2 — Identify and Fair Value the Acquired Net Assets (Purchase Price Allocation)

The most technically demanding part of acquisition accounting is the purchase price allocation (PPA): the process of identifying all the identifiable assets and liabilities of the acquiree and measuring each at fair value. This step regularly surfaces assets that did not appear on the acquiree’s own balance sheet at all, because under normal accounting rules an entity cannot recognise internally generated intangibles such as customer relationships or brand names.

Intangible assets that commonly arise in a PPA

| Intangible Asset | Typical Businesses | Common Valuation Method |

|---|---|---|

| Customer relationships | Any recurring-revenue business | Multi-period excess earnings method (MEEM) |

| Developed technology / IP | SaaS, manufacturing, pharma | Relief-from-royalty method |

| Brand / trade name | Consumer, retail, FMCG | Relief-from-royalty method |

| Order backlog | Construction, project businesses | Incremental income approach |

| Licences and permits | Regulated industries, media | Market approach or income approach |

| Non-compete agreements | Professional services, advisory | With-and-without method |

The PPA is typically performed by a specialist valuer engaged by the acquirer, and must be completed within twelve months of the acquisition date (the IFRS 3 measurement period). Provisional fair values can be used in the first consolidation if the work is not complete, but they must be finalised — and the opening balance sheet retrospectively adjusted — within that window.

Common mistake: Recognising only the assets on the acquiree’s pre-acquisition balance sheet, and treating the entire excess of consideration over book value as goodwill. This overstates goodwill, understates identifiable intangibles, and produces incorrect amortisation charges in future periods. Under IFRS, auditors routinely challenge PPA completeness.

Step 3 — Calculate Goodwill

Once fair values are established, goodwill is the residual: the amount by which the sum of the consideration transferred and any NCI exceeds the fair value of the net identifiable assets. Under IFRS 3, the acquirer can choose, on a transaction-by-transaction basis, whether to measure NCI at fair value (full goodwill method) or at NCI’s proportionate share of the fair value of the acquiree’s net identifiable assets (partial goodwill method). The choice affects both the goodwill recognised and the NCI balance in equity.

The NCI post on the BrizoConsol blog covers the mechanics of how to calculate non-controlling interest in financial consolidation in detail, including the difference in NCI measurement between the two methods.

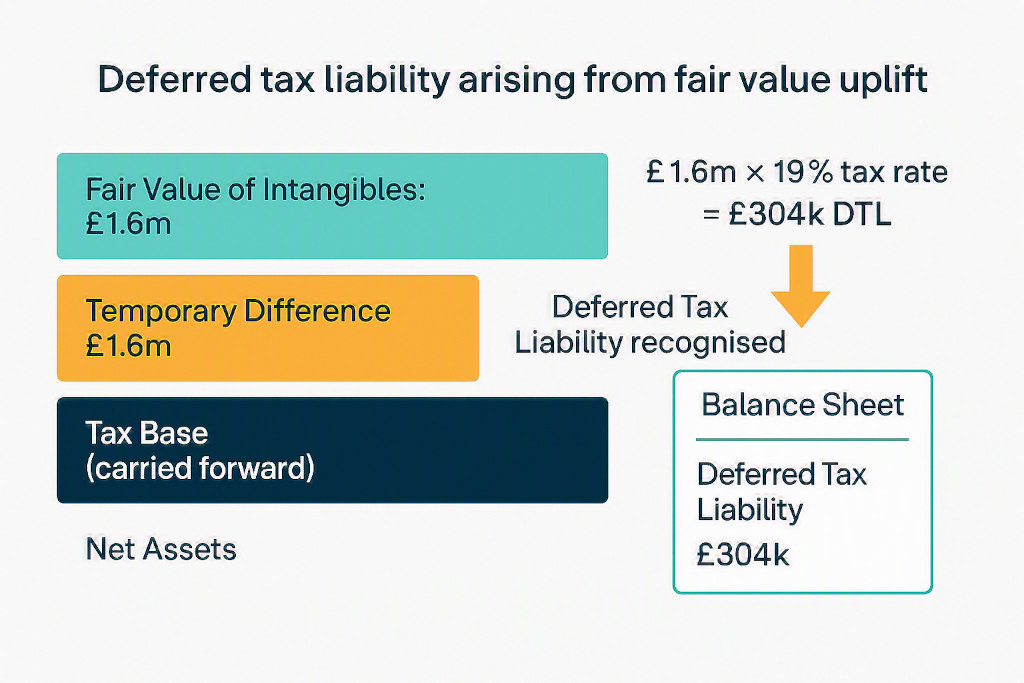

Step 4 — Recognise Deferred Tax on Fair Value Uplifts

This step is frequently omitted in practice, yet it is required by IAS 12 and has a material effect on both the net identifiable assets recognised and the goodwill figure.

When intangible assets are recognised at fair value in the PPA, their carrying amount in the consolidated accounts exceeds their tax base. The tax base of an internally generated intangible that was expensed through the acquiree’s P&L is typically nil — the acquiree received a tax deduction for those costs years ago, and the intangible carries no remaining tax value. The difference between the fair value carrying amount and the nil tax base is a temporary difference, which gives rise to a deferred tax liability (DTL) at the acquisition date.

The DTL is recognised as a liability in the PPA, which reduces the net identifiable assets acquired. Since net identifiable assets are lower after the DTL is recognised, goodwill is correspondingly higher. This is sometimes called the “grossing up” effect: recognising the intangible forces recognition of a DTL, which forces more goodwill.

A Practical Example: AcquireCo Acquires TechTarget Ltd

AcquireCo Ltd acquires 80% of TechTarget Ltd, a UK-based software business, on 1 January. The terms of the deal are:

- Cash consideration at completion: £4,800,000

- Contingent consideration (earn-out): up to £1,000,000 payable in year two if revenue targets are met. The fair value at acquisition date, probability-weighted, is assessed at £600,000.

Total consideration transferred: £5,400,000.

TechTarget’s balance sheet at acquisition date (book value)

| Asset / Liability | Book Value £ |

|---|---|

| Property, plant & equipment | 620,000 |

| Trade debtors | 480,000 |

| Cash | 310,000 |

| Trade creditors | (210,000) |

| Deferred revenue | (200,000) |

| Net assets (book value) | 1,000,000 |

Purchase price allocation — intangibles identified

The PPA exercise identifies three intangible assets not previously on TechTarget’s balance sheet:

| Intangible Asset | Fair Value £ | Useful Life | Valuation Method |

|---|---|---|---|

| Customer relationships | 900,000 | 8 years | Multi-period excess earnings |

| Developed technology (IP) | 500,000 | 5 years | Relief-from-royalty |

| Brand name | 200,000 | 5 years | Relief-from-royalty |

| Total intangibles identified | 1,600,000 | ||

Deferred tax liability on intangible uplift

The tax base of all three intangibles is nil (TechTarget expensed the relevant costs through its P&L in prior years and received tax relief at the time). The temporary difference is therefore the full £1,600,000 fair value. At the UK corporation tax rate of 25%:

DTL = £1,600,000 × 25% = £400,000

Fair value of net identifiable assets

| Component | £ |

|---|---|

| Net assets at book value | 1,000,000 |

| Add: intangibles identified in PPA | 1,600,000 |

| Less: deferred tax liability on uplift | (400,000) |

| Fair value of net identifiable assets | 2,200,000 |

Goodwill calculation (full goodwill method — NCI at fair value)

AcquireCo elects to use the full goodwill method. The NCI (20%) is assessed at a fair value of £900,000 based on an earnings multiple consistent with the deal pricing.

| Component | £ |

|---|---|

| Consideration transferred (£4.8m cash + £0.6m earn-out FV) | 5,400,000 |

| NCI at fair value (full goodwill method) | 900,000 |

| Less: fair value of net identifiable assets | (2,200,000) |

| Goodwill recognised | 4,100,000 |

Without the PPA, the goodwill calculation would use the book value of net assets (£1,000,000) instead of the fair value of £2,200,000 — resulting in goodwill of £5,300,000. The PPA exercise reduced goodwill by £1,200,000 and replaced it with identifiable intangibles that are amortised over their useful lives. Both the goodwill balance and future P&L charges are materially affected.

Opening consolidation journal at acquisition date

Dr Net identifiable assets (fair value) £2,200,000

Dr Goodwill £4,100,000

Cr Cash paid £4,800,000

Cr Contingent consideration liability £600,000

Cr Non-controlling interest £900,000

Note: the “Net identifiable assets (fair value)” debit includes the recognised intangibles of £1,600,000 less the DTL of £400,000, on top of the book-value net assets of £1,000,000.

This journal is posted in the group consolidation workings on the acquisition date. It does not appear in TechTarget’s own statutory accounts — it exists only at the group level. From this point forward, the customer relationships, technology IP, and brand name are amortised in the group P&L over their respective useful lives, and goodwill is tested for impairment annually.

Step Acquisitions

A step acquisition occurs when an entity first holds a non-controlling stake in another company (accounted for as an associate or financial asset) and subsequently acquires additional shares that take it past the control threshold. Under IFRS 3, the previously held interest is remeasured to fair value at the date control is obtained, with any resulting gain or loss recognised in profit or loss. This remeasurement can produce a significant one-time income statement impact, and requires careful documentation of the fair value basis used.

Step acquisitions also raise questions about how the previously held investment was accounted for — under the equity method if it was an associate (20%–50%), or as a financial instrument if it was a minority stake below 20%. Each starting position has different derecognition requirements when control is obtained. This is an area where the accounting team and the M&A advisers need to be aligned well before the transaction closes.

Post-Acquisition: What Carries Forward Into Every Consolidation

Once the acquisition date journal has been posted, several entries must be made in every subsequent group consolidation for as long as the subsidiary remains in the group:

- Amortisation of acquired intangibles. Customer relationships, technology IP, and brand name are amortised over their useful lives through the group P&L. These charges are not in the subsidiary’s own accounts — they exist only at the group level.

- Release of deferred tax liability. As acquired intangibles are amortised, the temporary difference reduces and the DTL partially unwinds each year, producing a deferred tax credit in the group P&L.

- Goodwill impairment review. Goodwill is tested for impairment annually (or more frequently if indicators exist), with any write-down recognised in the group P&L and not subsequently reversed.

- Intercompany eliminations. Once the subsidiary is consolidated, any trading between AcquireCo and TechTarget — management fees, shared services, intercompany loans — must be eliminated on consolidation. The intercompany eliminations guide covers the standard elimination entries that apply from the first post-acquisition period onwards.

- NCI share of post-acquisition results. The NCI’s share of the subsidiary’s profit and equity must be updated each period, flowing through the group P&L and balance sheet separately from the parent’s interest.

These are not one-time entries. They are standing consolidation adjustments — and for groups with several acquisitions at different dates, managing them accurately without a consolidation tool requires maintaining a detailed workbook for each deal, indefinitely.

Acquisition Accounting in BrizoConsol

BrizoConsol is built to handle the consolidation requirements that arise from acquisitions as a standard part of its configuration, not as a workaround. Acquisition date journals are entered once — consideration, fair-value net assets, goodwill, NCI, and contingent consideration — and the system applies the resulting standing adjustments (intangible amortisation, DTL release, goodwill balance) automatically in every subsequent consolidation. Entity data continues to flow in via direct API connections to Xero, QuickBooks, MYOB, and Zoho Books; the acquisition adjustments overlay the underlying entity data at consolidation without requiring manual re-entry each period.

For groups that have grown through acquisition — which describes a significant proportion of the mid-market companies that use financial consolidation software — this capability makes the difference between a consolidation process that closes in three days and one that takes two weeks of reconciliation before the acquisition-date adjustments are even confirmed.

Consolidate Acquired Entities With Confidence

Enter your acquisition date journals once. BrizoConsol applies the standing consolidation adjustments — intangible amortisation, goodwill, NCI — automatically in every close thereafter. Start Free Trial