The owner of a four-entity services group had been running each business profitably for five years. He had a clear view of each company individually: the revenues, the costs, the profit margins. What he did not have — what his bank was now asking for in connection with a refinancing — was a consolidated set of accounts showing the group as a single economic entity. His accountant produced something workable after three weeks of manual spreadsheet work. The bank asked a few questions that exposed some intercompany balances that had not been properly eliminated. The refinancing was delayed. The group was profitable and fundable. The reporting process let it down.

This situation is more common than it should be. Multi-entity businesses regularly reach the point where stakeholders — banks, investors, auditors, directors — need a group view, and the finance team discovers that producing one accurately is considerably harder than running each entity’s own books. Group reporting is a discipline in its own right. Understanding what it requires, why it goes wrong, and how to do it properly is the starting point for any multi-entity business that needs to produce reliable consolidated accounts.

What Group Reporting Actually Means

Group reporting is the process of producing financial statements that represent two or more legal entities as a single economic unit. Rather than showing the finances of each company individually, group reporting produces a consolidated picture: a combined profit and loss statement, a consolidated balance sheet, and typically a consolidated cash flow statement, all prepared as if the entities were one business.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

The key word is consolidated. A group of four companies does not simply add their revenues together to get group revenue. Intercompany transactions — any sale, charge, loan, or transfer from one group entity to another — must be eliminated before the consolidated figures are calculated. A management fee that the holding company charges to its subsidiaries shows up as income in the holding company and as an expense in the subsidiaries. At the group level, both entries must be removed, because from the outside world’s perspective, no economic transaction has taken place. Money has moved between pockets within the same jacket.

Group reporting also involves combining entities that may use different charts of accounts, operate in different currencies, and be owned in different proportions. All of these factors have to be addressed before the consolidated numbers can be considered accurate. Getting each one right is a specific technical task, not just a matter of running a sum.

Which Businesses Need Group Reporting

Group reporting applies to any organisation that controls or significantly influences more than one legal entity. The structures vary widely, but the reporting challenge is consistent across all of them.

Holding companies are the most obvious case. A parent entity that owns controlling stakes in one or more operating subsidiaries is almost certainly required by law to produce consolidated accounts. In most jurisdictions, this requirement kicks in regardless of whether the group is listed or private — controlling more than 50% of the voting rights in another entity typically triggers the obligation to consolidate. For groups operating across multiple countries, the requirements of IFRS, US GAAP, FRS 102, or local GAAP will all apply depending on where the group is domiciled and where it reports.

Private equity and investment groups that own portfolios of operating businesses face the same requirement, often with additional complexity introduced by acquisition accounting — specifically the need to recognise goodwill, fair value adjustments, and deferred tax liabilities arising from business combinations at the point of acquisition.

Family-owned multi-entity businesses, professional practices structured across multiple trading entities, franchise groups, property investment groups holding assets through separate SPVs, and joint ventures all present group reporting requirements that are structurally similar even if the scale differs. In every case, the core challenge is the same: the finance function needs to look across legal entity boundaries and produce a single, accurate picture of the combined enterprise.

Even groups that are not legally required to consolidate find that they effectively need group reporting to run the business. A CFO managing four operating companies cannot give the board meaningful performance data by showing each P&L in isolation. The board needs a group view. That view requires consolidation work, even if it is being done informally and without an audit obligation attached to it.

What Group Reporting Must Produce

The output of a group reporting process is a set of consolidated financial statements. In their full form, these include three primary statements and a set of supporting notes and schedules.

The consolidated income statement — also called the consolidated profit and loss account — shows the group’s combined revenues and costs after eliminating all intercompany transactions. This is the statement that tells the board whether the group as a whole is profitable and gives investors a view of operating performance.

The consolidated balance sheet shows the combined assets and liabilities of the group, again after eliminating intercompany balances. Intercompany loans, receivables, and payables that exist between group entities must all be removed before this statement can be presented. Any goodwill arising from acquisitions — where the group paid more than the book value of the acquired entity’s net assets — appears as an asset on the consolidated balance sheet and must be subject to impairment testing in each subsequent period.

The consolidated cash flow statement reconstructs the group’s actual cash movements for the period. Building this statement from a set of individual entity P&Ls and balance sheets is one of the more technically demanding parts of group reporting, because it requires the indirect method to be applied to consolidated — not entity-level — movements, with intercompany cash flows also eliminated.

For groups that own subsidiaries partially rather than in full, the consolidated balance sheet must also show non-controlling interest — the portion of the subsidiary’s equity that belongs to minority shareholders rather than the parent. This line appears in equity on the balance sheet and requires a specific calculation based on the subsidiary’s net assets and the non-controlling ownership percentage.

The Five Things Group Reporting Requires to Be Done Correctly

Most errors in group reporting trace back to one or more of five specific technical requirements not being handled properly. Understanding each of them is essential to understanding why the process is harder than it looks and where investment in the right tools pays off.

Account Mapping Across Entities

Every entity in the group has its own chart of accounts. These charts reflect the history of each business — how it was set up, which accounting software it uses, which accountant configured it, and which industry it operates in. A property holding entity’s chart of accounts looks nothing like a professional services firm’s. A company acquired from a third party arrives with a chart of accounts designed for its previous owner’s purposes, not the group’s.

Before consolidation can run, every account in every entity must be mapped to a shared group chart of accounts. Revenue from Entity A and revenue from Entity B need to land in the same group line before they can be combined. A group with five entities and two hundred accounts per entity has up to a thousand mapping decisions to make — and those mappings must be maintained, updated, and applied consistently every single period. Any inconsistency in how accounts are mapped produces errors in the consolidated output, and those errors are difficult to trace once the consolidated figures have been assembled.

Intercompany Elimination

Intercompany transactions are the most technically important and the most frequently mishandled element of group reporting. Every time one group entity transacts with another — charges a management fee, lends money, sells goods, provides a service — both sides of that transaction appear in the individual entity accounts. At the group level, both sides must be eliminated before the consolidated statements are produced.

The elimination covers income statement items — intercompany revenues and expenses — and balance sheet items, including intercompany receivables and payables and intercompany loan balances. Where an intercompany transaction has generated an unrealised profit — for example, where one entity has sold inventory to another entity in the group and that inventory has not yet been sold to a third party — the unrealised element must also be eliminated from consolidated profits.

The complication in practice is that intercompany balances frequently disagree between entities. Entity A records a receivable of $50,000 from Entity B. Entity B records a payable of $48,500 to Entity A. The difference of $1,500 may reflect timing — a payment in transit — or it may reflect an error. Either way, the mismatch must be investigated and resolved before the consolidation can close. In a group with ten or fifteen entities and significant intercompany activity, reconciling these differences each period is a substantial task. For a more detailed walkthrough of how intercompany eliminations work mechanically, see our guide to intercompany journal automation.

Foreign Currency Translation

Groups with entities operating in more than one currency face an additional layer of complexity. The financial statements of each foreign entity must be translated into the group’s presentation currency before they can be included in the consolidated accounts. The translation is not simply a matter of applying a single exchange rate. Under IFRS and most other frameworks, the balance sheet is translated at the closing rate as of the reporting date, while the income statement is translated at the average rate for the period. The difference between what these two rates produce — the currency translation adjustment — is not recognised in profit or loss but is taken directly to other comprehensive income and accumulated in a separate component of equity.

Getting this right requires maintaining both the closing rate and average rate for each currency for each reporting period, applying them correctly to the right categories of items, and calculating the resulting translation adjustment accurately. The cumulative translation adjustment that sits in equity also needs to be reversed when a foreign subsidiary is disposed of, which adds a further complication at the point of any group restructuring. For a detailed treatment of how currency translation works in group consolidation, see our currency translation adjustment guide.

Non-Controlling Interest

When a parent company owns less than 100% of a subsidiary, the portion of that subsidiary’s equity and earnings that belongs to outside shareholders must be separately identified in the consolidated accounts. This is the non-controlling interest. It appears as a separate component of equity in the consolidated balance sheet, and the NCI share of the subsidiary’s profit or loss is separately presented in the consolidated income statement, below the group’s profit for the period.

The NCI calculation flows through from the subsidiary’s net assets at each reporting date and must be updated for the subsidiary’s profits or losses for the period, any dividends paid by the subsidiary, and any changes in the ownership percentage arising from share transactions. For groups that have acquired subsidiaries through business combinations, the NCI figure at acquisition also depends on whether the group uses the proportionate method or the full goodwill method — a choice that affects both the NCI balance and the goodwill recognised on acquisition. Our NCI feature overview covers how BrizoConsol handles these calculations automatically.

Consolidation Adjustments

Beyond the four standard steps above, group reporting frequently requires additional adjustments. Acquisition accounting adjustments — the fair value adjustments made to the acquired entity’s assets and liabilities at the date of acquisition, and the amortisation of those adjustments in subsequent periods — must be maintained and applied each time the consolidation runs. Goodwill impairment testing is an annual requirement. Deferred tax adjustments arising from the difference between the accounting and tax base of assets create further complexity. Groups that have made acquisitions at different points in time carry a layered set of adjustments that must all be tracked and maintained correctly.

Why Group Reporting Goes Wrong

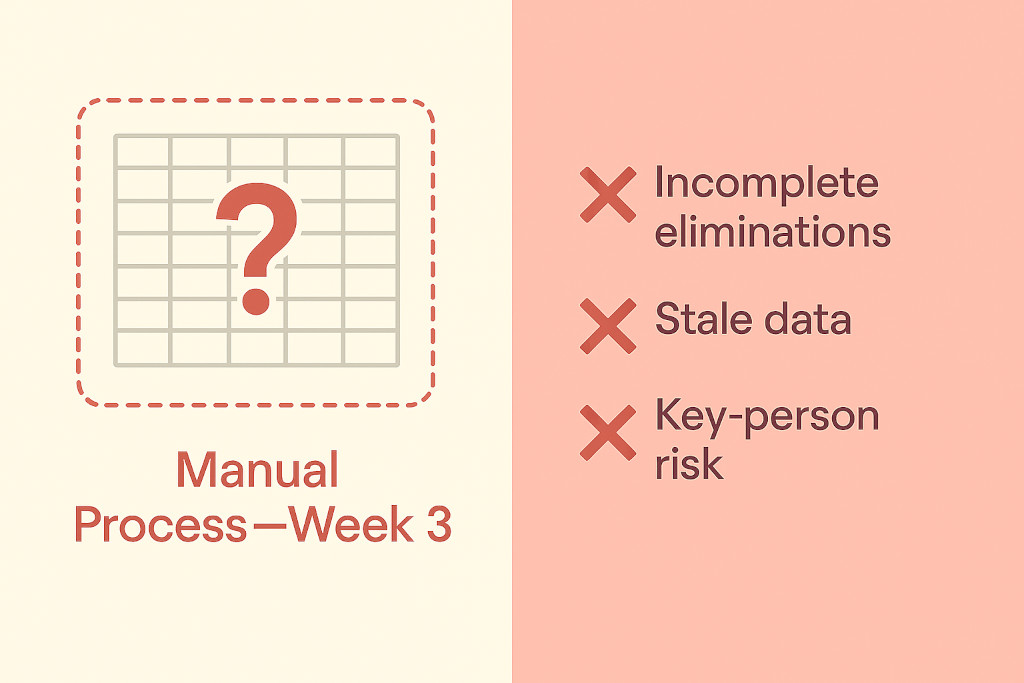

The most common group reporting failure mode is not fraud or incompetence. It is the wrong tool for the job being used by capable people under significant time pressure. That tool, in the overwhelming majority of cases, is Microsoft Excel.

Excel is a powerful and flexible tool for financial modelling and analysis. It is not designed to be a consolidation engine. A consolidation workbook built in Excel grows in complexity with every entity added to the group, every acquisition completed, and every period that passes without the workbook being properly documented and tested. Over time, the workbook becomes a critical piece of infrastructure that one person understands deeply and nobody else can maintain. It is rebuilt from scratch — or partially rebuilt — whenever that person leaves. The manual data entry required to load each period’s trial balances introduces errors that take hours to identify and correct. The version control is informal: the definitive version is the one on a shared drive that may or may not be the latest one, depending on whether someone remembered to save it in the right place.

The result is a consolidation process that takes far longer than it should, produces results that are difficult to audit or independently verify, and consumes the finance team’s capacity right at the point in the month when that capacity is most scarce. A finance team still closing the month-end consolidation in week three of the following month is a finance team that cannot provide the board with timely information. The strategic cost of that delay — in the quality of decisions being made without current data — is real and significant, even if it rarely gets measured.

The second failure mode is incomplete elimination. Intercompany balances that do not reconcile are either written off as rounding, carried forward in the hope that they will self-correct, or simply overlooked in the pressure to close. Any of these outcomes produces consolidated accounts that overstate or understate assets, liabilities, revenues, or costs — often by amounts that are small enough to be ignored individually but material in aggregate.

The third failure mode is timing. When the manual consolidation process takes three weeks, the figures being reported to the board reflect the position as of the end of last month, two and a half weeks ago. In businesses where conditions change quickly, that information is of limited value for decision-making. The board is navigating by a map that was drawn three weeks ago.

What Good Group Reporting Looks Like in Practice

A well-functioning group reporting process has three defining characteristics. It is fast, producing consolidated accounts within a few days of period end rather than weeks. It is accurate, with intercompany balances fully reconciled, eliminations correctly applied, and currency translation handled consistently. And it is auditable, meaning that every consolidated figure can be traced back to a source — the entity-level trial balance that produced it, the elimination journal that removed an intercompany balance, the exchange rate applied to translate a foreign entity’s results.

Speed matters because timely information is more valuable than retrospective information. A CFO reviewing consolidated results for May on the fifth of June can intervene in June if something looks wrong. A CFO reviewing May’s results on the twenty-eighth of June is reviewing history at that point. The business has already moved on.

Accuracy matters because errors in consolidated accounts have consequences. Banks and investors make funding decisions based on these figures. Auditors test them against source records. Errors that are discovered after the accounts have been shared externally damage credibility and may require restatement, which is both costly and reputationally damaging.

Auditability matters because the ability to explain and defend the consolidated figures is what separates a professional finance function from one that produces numbers it cannot fully account for. When a lender asks why group revenue this quarter is different from the same period last year, the finance team needs to be able to answer that question at the group level, not just at the entity level.

Achieving all three — speed, accuracy, and auditability — in a manual Excel-based process becomes increasingly difficult as the group grows. The complexity compounds faster than the finance team’s capacity to manage it manually.

How BrizoConsol Handles Group Reporting for Multi-Entity Businesses

BrizoConsol is purpose-built for multi-entity group reporting. It connects directly to the accounting software each entity uses — Xero, QuickBooks, MYOB, Zoho Books, or any platform via Excel import — and pulls trial balance data automatically at each reporting period. There is no manual data extraction, no copy-pasting of figures, and no risk of importing the wrong version of an entity’s numbers.

Account mapping is configured once for each entity and maintained in the platform. Once a group accountant has mapped each entity’s accounts to the group chart of accounts, that mapping is preserved and applied automatically every time the consolidation runs. Changes to an entity’s chart of accounts — a new account code, a renamed category — are flagged so the mapping can be updated rather than silently carrying forward an incorrect assignment.

Intercompany eliminations run automatically based on the intercompany relationships configured in the platform. BrizoConsol identifies matched intercompany balances across entities, flags discrepancies where the two sides of a transaction do not agree, and posts the elimination journals without manual intervention. The finance team’s role shifts from calculating and posting eliminations to reviewing and approving them — a much faster and more reliable process than building elimination schedules manually.

Currency translation is handled at the entity level, with closing and average rates applied correctly to balance sheet and income statement items respectively. The resulting currency translation adjustment is calculated automatically and presented in other comprehensive income, consistent with IFRS requirements. For groups with multiple foreign entities, this alone represents a significant reduction in manual calculation work each period.

Non-controlling interest calculations are maintained by the platform based on the ownership structure configured for each subsidiary. The NCI share of equity, profit, and comprehensive income is calculated automatically and presented in the consolidated statements in the correct format.

The output is a set of consolidated financial statements — consolidated P&L, consolidated balance sheet, consolidated cash flow statement — that can be produced on demand rather than at the end of a weeks-long manual process. For accounting firms managing consolidations on behalf of clients, or for CFOs and group finance teams managing multi-entity structures in-house, this change in the time required to close each period has a direct impact on the quality and timeliness of reporting available to the business.

For a more detailed look at how the platform handles specific structural scenarios, the holding company consolidation guide and the property group consolidation guide cover the specific requirements those structures present.

Getting Group Reporting Right From the Start

The finance teams that handle group reporting well share a common characteristic: they treat it as a process to be designed and maintained, not a task to be repeated from scratch each period. That means defining a group chart of accounts and maintaining account mappings consistently. It means setting clear rules about how intercompany transactions are recorded, so that both sides of each transaction are entered in a way that makes reconciliation straightforward. It means establishing a close timetable that each entity follows, so that trial balances are available at the same point in time across the group. And it means choosing tools that are built for the job rather than adapting general-purpose tools to a problem they were not designed to solve.

Multi-entity businesses that have been managing group reporting through spreadsheets typically reach a point — a new entity acquired, a lender requesting audited consolidated accounts, a CFO who wants monthly board packs without a three-week close cycle — where the manual process stops being viable. That inflection point is the right moment to build the process on a foundation that will scale with the group rather than against it.

If you are at that point, or if you want to see what group reporting looks like when the process is properly automated, see BrizoConsol in action.