Financial Consolidation for Holding Companies: How Finance Leaders Consolidate Across Subsidiaries

A holding company is an entity that owns a controlling interest in one or more subsidiary businesses. Unlike an operating company that generates revenue from goods or services directly, a holding company derives its value from the ownership stakes it holds. Holding groups can range from relatively simple two or three entity structures to sprawling international networks with dozens of subsidiaries operating across multiple jurisdictions, currencies, and accounting standards.

For finance leaders and CFOs working within holding structures, financial consolidation is not a nice to have activity. It is a legal, regulatory, and strategic necessity. In most jurisdictions, a holding company that controls a group of subsidiaries is required to prepare consolidated financial statements that reflect the group as a single economic entity. This means combining the balance sheets and income statements of every subsidiary, eliminating intercompany balances and transactions, translating foreign currency results, and adjusting for non-controlling interests where the holding company does not own 100% of a subsidiary.

Beyond the regulatory requirement, consolidated financials are the foundation upon which board members, investors, lenders, and auditors form their view of the group. A board that cannot see a clean, timely consolidated picture of the group is making decisions without the full picture. Lenders and investors need consolidated accounts to assess credit risk and returns. Auditors need them to sign off on the group. The finance function that can produce these statements reliably and on time earns strategic influence rather than spending all its energy on month end firefighting.

Automate NCI calculations across all your entities.

BrizoConsol handles non-controlling interest automatically — no manual adjustments required.

The problem for most holding companies is that financial consolidation has traditionally been a laborious, error prone process dominated by spreadsheets, manual journal entries, and enormous amounts of copy and paste work. This guide explains what that process actually involves, where it breaks down, and how purpose built software like BrizoConsol changes the outcome for holding company finance teams.

The Real Challenges Holding Companies Face at Consolidation Time

Most holding companies consolidate using a combination of accounting software at the subsidiary level and spreadsheets at the group level. Each subsidiary runs on whatever accounting platform suits its operations, whether Xero, QuickBooks, Sage, or another system. At period end, a finance manager or group accountant downloads trial balances from each entity, pastes them into a master workbook, maps accounts across different charts of accounts, eliminates intercompany items, translates foreign currency, accounts for non-controlling interest, and attempts to produce a coherent group pack. This process works in a loose sense. It produces numbers. But it introduces several categories of risk and inefficiency that compound as the group grows.

The first challenge is account mapping. Each subsidiary runs its own chart of accounts, which reflects the needs of that particular business. A manufacturing entity operating in Germany uses different account names and structures than a professional services business in the United Kingdom. Someone has to map these to a common group chart of accounts every single time a consolidation is run, unless that mapping has been carefully documented and maintained in a consistent, accessible format. In practice, the mapping lives in the head of one person, encoded in formulas buried deep in a spreadsheet that nobody else fully understands. When that person leaves, the knowledge leaves with them.

The second challenge is intercompany elimination. Holding groups are full of intercompany activity. Parent loans to subsidiaries, management charges, shared service recharges, and intercompany sales of goods or services are all common. Every one of these transactions exists in two entities simultaneously and must be eliminated before the group accounts can be considered accurate. In a simple two entity group, this is manageable. In a group with ten or twenty entities, it becomes an enormous reconciliation exercise, and it is very easy for balances to remain unreconciled when each entity has recorded the same transaction slightly differently.

The third challenge is multi currency consolidation. Holding groups frequently own subsidiaries that operate in different currencies. The rules for translating foreign currency financial statements, including which rate to use for the balance sheet, which rate to use for the income statement, and how to account for the resulting translation difference, are both complex and mandatory. Getting this wrong does not just produce incorrect numbers. It produces accounts that will not pass an audit and may need to be restated, which is a damaging and expensive outcome for any holding group.

The fourth challenge is timeliness. A finance team that spends two weeks on manual consolidation work is a finance team that cannot provide meaningful insight to the board. By the time the pack is finished, the information is stale. Leadership is making decisions on data from three weeks ago. In a fast-moving business environment, that delay has a real cost in the quality of decisions being made at the top of the group.

What Holding Company Consolidation Actually Requires

To consolidate a holding group accurately, a finance team needs to perform several distinct operations, each of which must be done correctly for the overall result to be trustworthy. Understanding what these operations involve is the first step toward building a process that can deliver reliable results at scale.

First, the team needs a common chart of accounts. Every subsidiary trial balance needs to be mapped to a consistent set of account codes and categories before the figures from different entities can be combined. Without this mapping, adding together the revenues of two subsidiaries is meaningless because one might record revenue under one account structure and another might use a completely different approach. A group chart of accounts that is clearly defined and consistently applied is the foundation of reliable consolidation.

Second, the team needs to handle intercompany eliminations thoroughly. This means identifying every transaction that occurred between entities within the group and removing it from the consolidated result. If the parent charged a subsidiary a management fee, that income in the parent and that expense in the subsidiary must both be removed. If the parent lent money to a subsidiary, the loan asset in the parent and the loan liability in the subsidiary must both be removed. Failure to eliminate these transactions correctly results in overstated revenues, overstated expenses, overstated assets, or overstated liabilities in the consolidated accounts, all of which create audit risk and investor concern.

Third, the team needs to handle non-controlling interests where applicable. When a holding company owns 75% of a subsidiary rather than 100%, the remaining 25% belongs to outside shareholders. The consolidated accounts need to present the full results of the subsidiary because it is controlled by the group, but must also identify the portion of those results and net assets that belong to the minority shareholders separately. This attribution must be calculated correctly for the equity section of the balance sheet and the profit attribution on the income statement to be accurate.

Fourth, where subsidiaries operate in foreign currencies, the team needs to apply the correct translation methodology. Income statement items are typically translated at the average rate for the period. Balance sheet items are typically translated at the closing rate. The difference that arises from applying these two different rates is recorded as a currency translation adjustment in equity and must be separately tracked and presented in the consolidated accounts. Purpose built consolidation software eliminates most of the failure points that arise when these calculations are performed manually.

How BrizoConsol Supports Holding Company Consolidation

BrizoConsol is purpose built for the kind of consolidation work that holding companies need to perform on a recurring basis. Rather than treating each subsidiary as a separate file to be downloaded and stitched together manually, BrizoConsol connects directly to the accounting platforms that each subsidiary uses and pulls data automatically each period. Finance teams that run Xero in some entities and QuickBooks in others can consolidate them all within a single platform without manually exporting trial balances, reformatting data, or maintaining a bank of CSV files.

The account mapping function in BrizoConsol means that the group chart of accounts is defined once and maintained within the platform. BrizoConsol maps each subsidiary account to the group structure using the logic the finance team configures, and applies that mapping consistently every single period. This eliminates the most error prone step in the traditional spreadsheet process and ensures the same treatment is applied regardless of who is running the consolidation. The mapping is transparent, auditable, and not dependent on any individual knowing which formula in which cell drives which result.

Intercompany eliminations are handled within BrizoConsol directly. Finance teams can define the intercompany relationships between entities and BrizoConsol will identify and eliminate the relevant balances and transactions as part of the consolidation run. Rather than hunting through ten trial balances looking for matching figures, the platform surfaces the intercompany positions and processes the eliminations automatically. Where intercompany balances do not agree between entities, BrizoConsol highlights the discrepancy so it can be investigated and resolved before the consolidation is finalised.

For holding companies with minority shareholders, BrizoConsol handles NCI calculations as part of the consolidation process. The finance team defines the ownership percentages for each entity and BrizoConsol applies the correct attribution of results and net assets to controlling and non-controlling interests in the consolidated output. For groups that have acquired subsidiaries over time and hold different percentage stakes in different entities, this automated NCI calculation removes a significant source of manual work and potential error.

Multi currency groups are fully supported. BrizoConsol applies the correct translation rates to income statement and balance sheet items and calculates the currency translation adjustment automatically. Finance teams no longer need to maintain a separate rate schedule or apply rates manually to each entity. The result is a consolidation process that takes hours rather than days, with a significantly reduced risk of error and a full audit trail of every calculation underpinning the consolidated output.

Multi Currency and Multi Entity Complexity in Holding Groups

The larger a holding group grows, the more complex its consolidation requirements become. A group that starts with two or three entities in a single country and currency will eventually expand, through acquisition or organic growth, into a structure that spans multiple jurisdictions, currencies, and regulatory environments. Each new entity adds not just more accounts to consolidate but more intercompany relationships to track, more currencies to translate, and more potential complications around ownership structure. The consolidation process that worked adequately for a small group frequently becomes unmanageable as the group scales.

Currency translation is one of the most technically demanding aspects of holding company consolidation. Under IFRS and most other major accounting standards, a subsidiary that operates in a foreign functional currency must have its financial statements translated into the group presentation currency at the appropriate exchange rates before being consolidated. This means that the value of a foreign subsidiary in the group accounts will fluctuate with exchange rates even if the subsidiary’s underlying performance is completely stable. The cumulative translation adjustment that results from this process accumulates in equity and must be properly tracked and presented as a separate component of group equity, not commingled with retained earnings.

For groups that include partially owned subsidiaries, the interaction between NCI and foreign currency translation adds another layer of complexity. The NCI share of the currency translation adjustment needs to be separately identified and allocated to the NCI balance in equity rather than to the portion attributable to the parent. In a spreadsheet, getting this right requires very careful formula construction and is easy to get wrong in ways that are not immediately visible but will be identified during audit. BrizoConsol handles these complexities as standard features of the platform, applying the correct treatment automatically based on the ownership and currency configurations the finance team has defined.

This matters enormously for holding groups that are growing through international acquisition. The ability to add a new foreign entity to the consolidation perimeter and have it correctly consolidated in the next reporting period, without weeks of manual setup work, is a capability that fundamentally changes what the finance function can deliver during periods of rapid group expansion. Rather than the finance team being stretched to breaking point every time a new entity is acquired, the onboarding of a new entity into the consolidation process becomes a routine, manageable task.

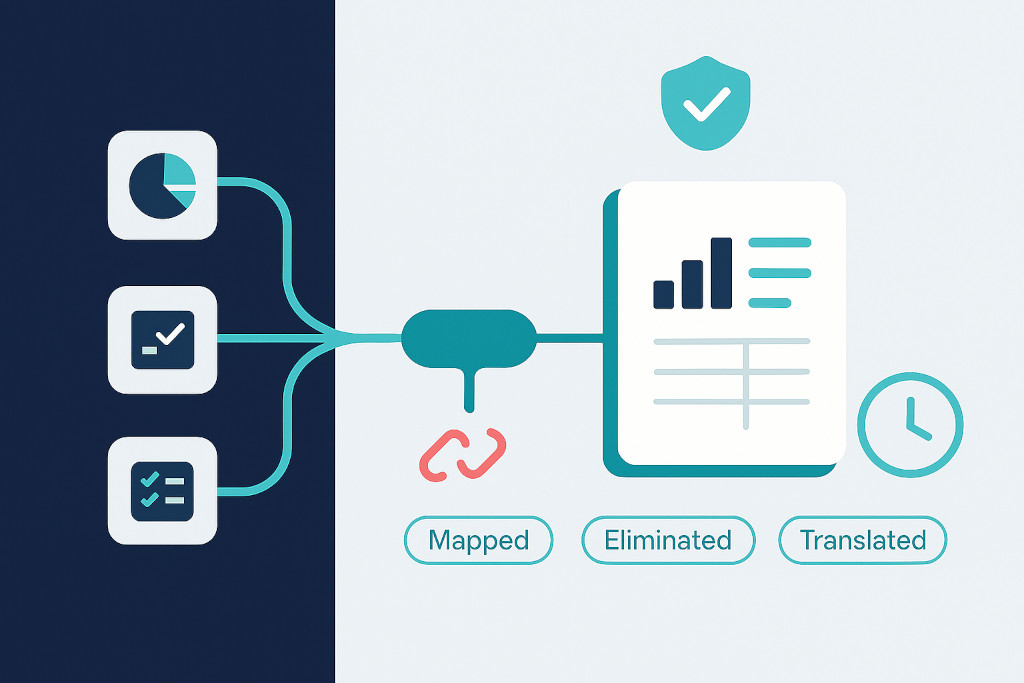

From Fragmented Financials to a Single Group View

For many holding companies, the transition from spreadsheet consolidation to purpose built software is a significant step change in what the finance function can actually deliver to the board and to stakeholders. When consolidation is automated and reliable, the finance team stops being the bottleneck in the reporting process and becomes the team that provides insight rather than just data. The conversation in the boardroom shifts from whether the numbers are right to what the numbers mean and what the group should do in response to them.

The most immediate benefit is speed. When BrizoConsol pulls data directly from subsidiary accounting systems and applies a consistent set of rules to produce the consolidated output, the time from period end to group accounts drops dramatically. What previously took two or three weeks of intensive manual work can be completed in hours. This means the board receives its financial pack while the information is still current and actionable, not three weeks after the period has ended when the underlying trading conditions may already have changed.

The second benefit is confidence in the numbers. When consolidation is done manually in spreadsheets, every person in the finance team knows that the numbers are approximately right rather than definitively right. There is always a nagging uncertainty about whether the intercompany eliminations caught everything, whether the exchange rates were applied correctly, and whether the account mapping is up to date. BrizoConsol removes that uncertainty by applying consistent, documented rules every time the consolidation runs. The output is backed by an audit trail that can be reviewed and challenged, not a set of formulas that only one person understands.

The third benefit is scalability. A holding company that is growing through acquisition needs a consolidation process that can absorb new entities without proportionally increasing the manual work involved. BrizoConsol is designed to onboard new entities efficiently. The finance team connects the new entity’s accounting platform, maps its accounts to the group chart of accounts, defines its intercompany relationships and ownership percentages, and it is ready to be consolidated in the next reporting period. The group can grow without the finance function becoming a barrier to that growth.

Getting Started With BrizoConsol as a Holding Company

The process of moving from spreadsheet consolidation to BrizoConsol is more straightforward than most finance teams expect. The first step is connecting the accounting platforms of each subsidiary entity. BrizoConsol integrates directly with Xero, QuickBooks, and other common accounting systems, pulling trial balance data automatically once the connection is established. There is no need to manually export and import files or maintain a collection of CSV downloads from multiple platforms.

The second step is defining the group chart of accounts and mapping each subsidiary account to it. This is typically the step that requires the most thought because it forces the finance team to make explicit the decisions that were previously implicit in the spreadsheet mapping. But doing this work once inside BrizoConsol means it never needs to be done again from scratch for each reporting period. The mapping is maintained and updated within the platform as the group chart of accounts or individual subsidiary account structures evolve.

The third step is defining the ownership structure of the group, including the equity percentages that determine how non-controlling interest is calculated, and setting up the intercompany relationships between entities so that BrizoConsol can identify and eliminate the relevant balances automatically. This configuration work is done once and maintained as the group structure changes over time. With these foundations in place, the first consolidated run can typically be produced quickly, and from that point on, each reporting period requires only the verification of exchange rates and any changes to intercompany positions before the consolidation runs.

Holding companies that are still consolidating in spreadsheets are carrying a significant operational and reputational risk. A consolidation error that makes it into an audited set of accounts is costly to unwind. A finance team that cannot produce group accounts within a reasonable timeframe cannot serve the needs of the board and the business effectively. BrizoConsol gives holding company finance teams the infrastructure they need to deliver consolidated financials they can stand behind, at the speed the modern board expects, and with the accuracy that auditors and investors require.