Financial Consolidation for Property Groups: How to Handle SPVs, Intercompany Loans and Group Reporting

The CFO of a property investment group with eleven entities received a request from her bank in March: provide consolidated accounts for the group within three weeks, including a group balance sheet showing all investment properties, bank facilities, and intercompany loan positions. Each of the eleven SPVs ran its own Xero ledger. There was no consolidated view. Her team spent two weeks pulling trial balances, mapping account codes into a master spreadsheet, manually eliminating intercompany loans, and arguing about which exchange rate to apply to the two overseas entities. They delivered — just — but the process left three people exhausted and produced a set of accounts her auditors subsequently identified two errors in.

Property groups face a consolidation problem that is structurally different from most other sectors. Understanding what makes financial consolidation for property groups distinctively complex — and how to approach it properly — is the starting point for getting it right.

Why Property Groups Have More Entities Than Almost Any Other Sector

A retail business with ten locations usually operates as a single legal entity. A property group with ten assets almost never does. Each property is typically held in a separate special purpose vehicle (SPV) — a discrete legal entity established to ring-fence the liability, financing, and tax position of each asset. The bank lending against a commercial building in Manchester wants its security confined to that asset, not commingled with a residential development in Birmingham. Hence: ten properties, ten SPVs, ten sets of accounts.

Automate NCI calculations across all your entities.

BrizoConsol handles non-controlling interest automatically — no manual adjustments required.

This structure is rational from a legal and financing standpoint. It creates significant complexity for the finance function. Each SPV must file its own statutory accounts. Each has its own bank account, its own loan facility, and — in a well-run group — its own audit trail. At group level, the holding company or fund entity needs consolidated financial statements that present the group’s position as a whole: total assets under management, combined debt, net equity, group cash position, and the intercompany positions that must be eliminated before any of those figures are meaningful.

For groups using Xero, QuickBooks or MYOB at the SPV level — which is the norm for groups up to around 30 entities — producing those consolidated accounts manually is the single largest month-end close problem the finance team faces.

The Consolidation Challenges Unique to Property Groups

Intercompany loans between SPVs and Holdco

Property groups routinely fund SPV acquisitions through loans from the holding company. The holdco lends £2 million to SPV3 to fund a deposit; SPV3 records a liability, holdco records a receivable. At consolidation, both sides must be eliminated — otherwise the consolidated balance sheet overstates both assets and liabilities by £2 million. Where there are eleven SPVs and several years of intercompany loan history, the elimination schedule becomes substantial. Interest accruals on those loans must also be eliminated, along with any management fees charged down from holdco to the SPVs.

For a detailed walkthrough of how these eliminations work mechanically, see our practical guide to intercompany eliminations — the principles apply directly to property group loan structures.

Investment property revaluations

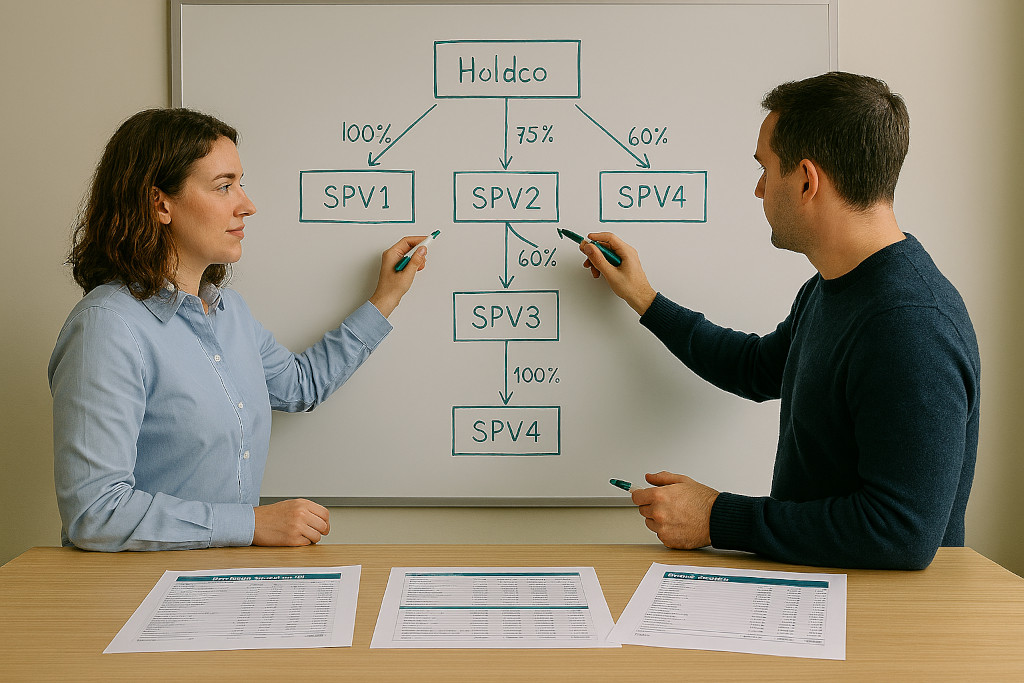

Where SPVs carry investment properties at fair value under IAS 40 or equivalent, revaluation gains and losses affect the individual entity’s balance sheet and — under certain frameworks — its income statement. At group level, these revaluations must be incorporated correctly. Where a property is owned by an SPV in which the holdco has a 75% stake, only 75% of the revaluation gain flows to group equity; the remaining 25% belongs to the non-controlling interest. Many finance teams handle this correctly in the statutory accounts of the SPV but misallocate it at the consolidation stage.

Mixed accounting platforms across the group

Property groups that have grown through acquisition frequently inherit the accounting platforms their acquired SPVs were already running on. A group of twelve SPVs might have eight on Xero, three on MYOB, and one legacy entity still on QuickBooks. Each platform uses its own chart of accounts. Before any consolidation can run, the account codes from each platform must be mapped to a common group structure. In a manual process, this mapping is rebuilt — or more accurately, copied and nervously edited — every single month.

Foreign currency subsidiaries

For groups holding assets in more than one currency jurisdiction — common for groups with New Zealand, Australian, or UK assets alongside European holdings — each foreign subsidiary’s financial statements must be translated into the group presentation currency before consolidation. The balance sheet is translated at the closing rate; the income statement at the average rate for the period. The resulting translation difference must be recognised as a cumulative translation adjustment (CTA) in group equity. This is one of the most error-prone calculations in group accounting and one of the most common audit findings in property group consolidations.

What a Property Group Consolidation Looks Like in Practice

Consider a simplified property group with the following structure:

Holdco Ltd — Group Parent (100% owner of all SPVs)

↓

SPV1 — Commercial office, Manchester

Xero · £4.2m property value · £2.8m bank loan

SPV2 — Residential development, Leeds

Xero · £1.9m WIP · £1.2m holdco loan

SPV3 — Retail unit, Bristol

MYOB · £3.1m property value · £2.1m bank loan

SPV4 — Industrial estate, Auckland (NZD)

Xero NZ · NZD 6.8m property · NZD 4.5m bank loan

Holdco has made intercompany loans to SPV2 (£1.2m) and provided development finance to SPV1 (£400k). Management fees of £5,000 per month are charged to each SPV. Before a consolidated balance sheet can be prepared, the following items must be eliminated and adjusted:

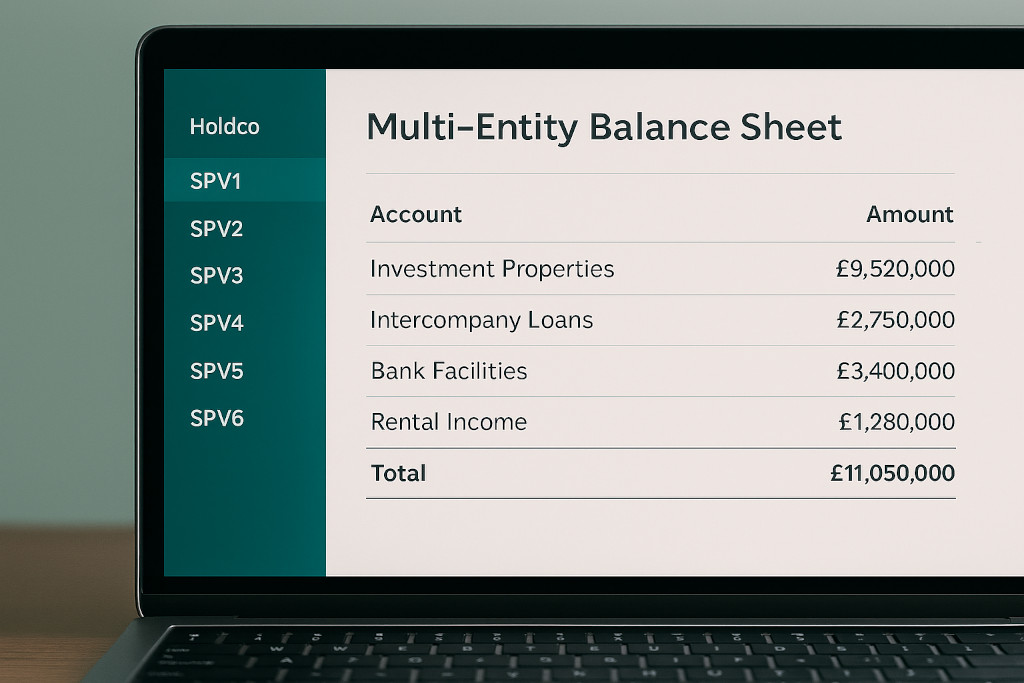

| Item | Holdco | SPV | Consolidation treatment |

|---|---|---|---|

| Intercompany loans | Receivable: £1.6m | Payable: £1.6m | Eliminate both sides — net to zero |

| Loan interest accrued | Income: £32k | Expense: £32k | Eliminate from P&L and accruals |

| Management fees (annual) | Income: £240k | Expense: £240k | Eliminate from P&L |

| SPV4 (NZD) translation | — | NZD statements | Translate at closing/average rate; post CTA to equity |

| After these eliminations, the consolidated balance sheet reflects only third-party assets, liabilities and equity — no intercompany positions remain. | |||

Illustrative consolidation adjustments for a four-SPV property group. Figures simplified for clarity.

Once the eliminations are posted and SPV4’s NZD statements are translated, the consolidated accounts show: total investment properties at group carrying value, total external bank debt, group equity after eliminating holdco’s investment in its subsidiaries, and the NZD translation adjustment sitting in other comprehensive income.

“A property group’s consolidated balance sheet is only as useful as its eliminations are complete. An uneliminated intercompany loan doesn’t just overstate assets — it overstates the group’s apparent leverage, which is exactly the figure your bank is watching.”

How BrizoConsol Works for Property Management Groups

BrizoConsol connects directly to Xero, QuickBooks and MYOB via live API — which means a group with SPVs spread across multiple platforms can pull all entity trial balances into a single consolidation engine without manual exports or file transfers. For a property group where SPVs have been set up at different times on different platforms, this is the foundation that makes everything else possible.

For the specific challenges property groups face, the platform handles:

- Automatic intercompany elimination — holdco loan receivables are matched against SPV payables and eliminated without manual journal entries. Management fee income and expense pairs are eliminated in the same pass. Every elimination is logged with a full audit trail.

- Multi-currency translation with CTA — SPV4’s NZD accounts are translated at the correct closing and average rates, with the resulting CTA posted to group equity automatically. No spreadsheet, no manual rate lookup.

- AI Auto-Map for chart of accounts — where SPVs on different platforms use different account codes, the mapping engine aligns them to the group chart of accounts. Set up once; it applies to every subsequent month.

- Virtual Groups for reporting by asset class or geography — a property group can create a “Commercial” virtual group (SPV1, SPV3) and a “Residential” virtual group (SPV2) and generate consolidated P&L and balance sheet for each subset without duplicating the underlying data.

- IFRS and UK GAAP tagging — for groups reporting investment properties under IAS 40 or FRS 102, the platform supports framework-level tagging so revaluation entries are handled correctly at group level.

You can see how this fits the broader consolidation picture in our overview of what financial consolidation software does and why property groups need it.

Getting Started: What Property Groups Should Do First

For property groups moving from a manual consolidation process to software, the typical sequence is:

- Map your entity structure. Document which entities exist, which platform each runs on, and the ownership percentages. Note any entities where ownership is not 100% — these will require NCI calculations.

- List all intercompany positions. Before any automation can eliminate them, you need a complete schedule of intercompany loans, management fee arrangements, and any other intragroup trading. The first automated consolidation will flag mismatches — this is normal and useful.

- Agree the group chart of accounts. Decide on the account structure the consolidated accounts will use. This is a one-time exercise and the AI Auto-Map will handle the ongoing translation from entity-level codes to group codes.

- Connect each entity’s ledger. With BrizoConsol, this is a direct API connection — no CSV exports. Each entity is connected once and data flows automatically from that point.

- Run your first consolidation. Expect the first run to surface some intercompany mismatches and account mapping questions. Resolve them once; they will not recur in subsequent months.

Bank covenant tip: If your lender requires consolidated accounts on a quarterly or semi-annual basis, set up BrizoConsol to run a full consolidation at the end of each relevant period. With direct API connections and automated eliminations, the consolidated pack can be produced in hours rather than weeks — leaving time for review rather than data assembly.

For groups that have grown quickly through acquisition and are dealing with multiple accounting platforms, mismatched charts of accounts, and years of accumulated intercompany loan history, the first consolidated run using automation is often the first time the group’s actual financial position has been seen clearly. That clarity — and the reduction in close time that consolidation software delivers — is what makes the switch worthwhile.