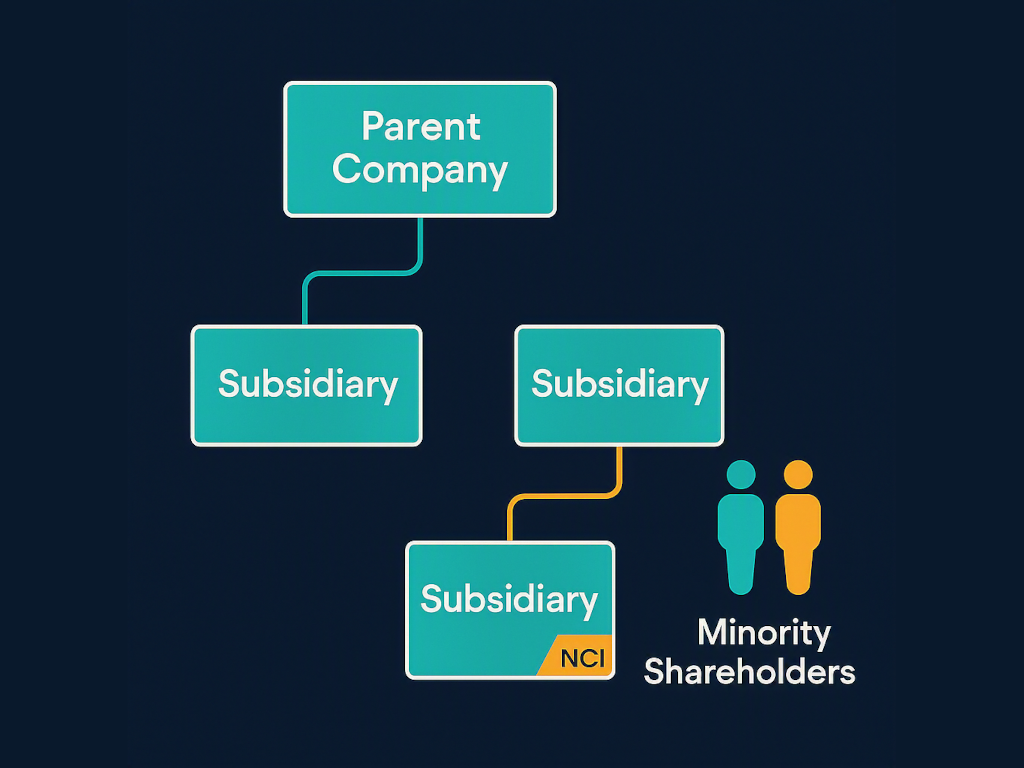

When a parent company acquires a controlling stake in another business but does not own 100% of it, the financial statements of the group become more complex in one very specific and important way: not all of the subsidiary’s net assets, income, and equity belong to the parent. A portion — the share held by outside investors — must be recognised, measured, and disclosed separately. This portion is called the Non-Controlling Interest, commonly abbreviated as NCI and also referred to in older accounting standards as Minority Interest. Understanding how to calculate NCI correctly is one of the most essential technical skills in group financial reporting, and it is also one of the most commonly mishandled. Finance teams that get it wrong end up overstating the equity attributable to the parent, misrepresenting consolidated profit, and producing balance sheets that do not reconcile — all errors that become deeply problematic when external auditors or investors scrutinise the numbers. This guide walks through exactly how NCI is calculated, from the acquisition date through to each subsequent reporting period, with worked examples for each step. At the end, we cover how BrizoConsol eliminates the manual workbook entirely by calculating NCI automatically the moment you set an ownership percentage.

What Is Non-Controlling Interest and Why Does It Matter?

Non-Controlling Interest is the portion of a subsidiary’s equity, net assets, and profit or loss that is attributable to shareholders other than the parent company. It arises whenever a parent acquires a controlling interest in a subsidiary — typically defined as more than 50% of voting rights — but does not acquire the full 100%. The shareholders who hold the remaining percentage are the non-controlling (or minority) shareholders, and their economic interest in the subsidiary must be recognised in the consolidated financial statements separately from the interests of the parent’s own shareholders. This requirement exists because consolidated financial statements are designed to present the group as a single economic entity. When you consolidate a subsidiary, you bring 100% of its assets, liabilities, income, and expenses into the group statements — not just your proportionate share. But including 100% of a subsidiary’s net assets while only 75% of them belong to you would overstate the group’s equity attributable to the parent. NCI is the mechanism that corrects this: it represents the 25% (or whatever percentage applies) that belongs to external shareholders, and it sits within equity on the consolidated balance sheet but is disclosed separately from the parent’s equity. The same logic applies to the income statement — consolidated profit must be split between the amount attributable to the parent’s shareholders and the amount attributable to NCI. Under both IFRS (specifically IFRS 10 and IFRS 3) and US GAAP (ASC 810), this split presentation is mandatory, not optional. Getting it right matters not just for compliance but for the integrity of every key metric that investors and boards rely on — earnings per share, return on equity, net asset value per share, and more.

The Two Methods of Calculating NCI

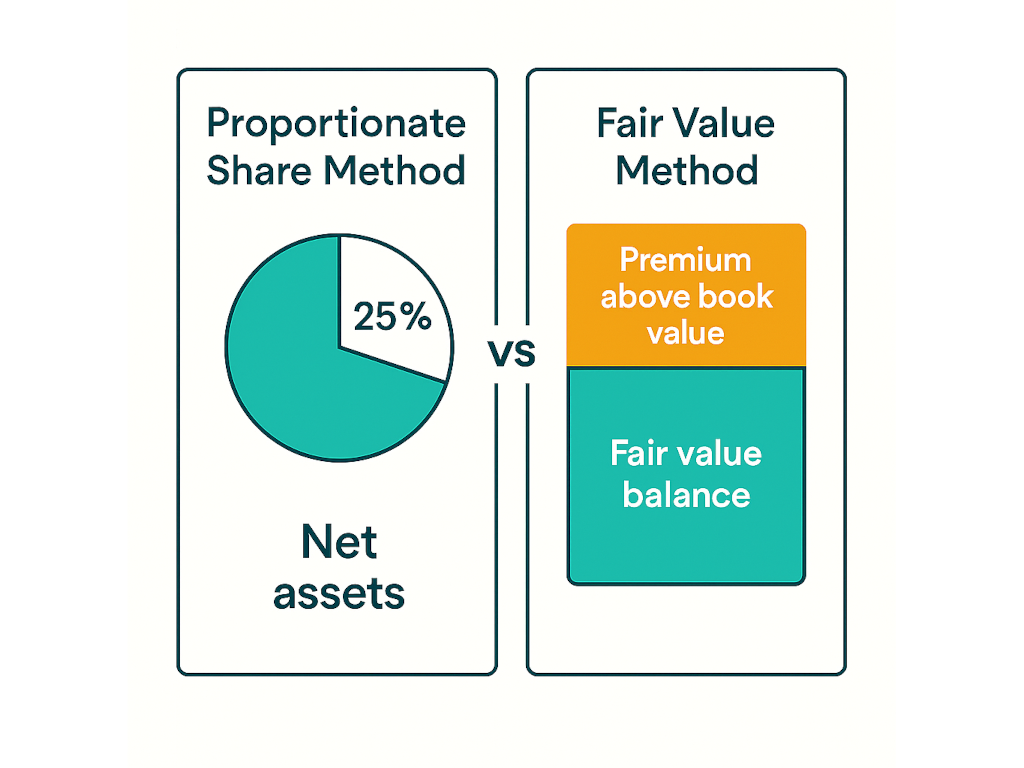

Before working through the calculation steps, it is important to understand that under IFRS 3 (Business Combinations), there are two permitted methods for measuring NCI at the acquisition date, and the choice between them has a meaningful impact on the figures that flow into the consolidated balance sheet. The first method is the Proportionate Share Method (also called the partial goodwill method). Under this approach, NCI is measured as the non-controlling shareholders’ proportionate share of the subsidiary’s identifiable net assets at fair value on the acquisition date. This is the simpler and more commonly used method, particularly for private company groups and those reporting under standards that follow a proportionate approach. The second method is the Fair Value Method (also called the full goodwill method). Under this approach, NCI is measured at its fair value on the acquisition date — which typically means estimating what the minority stake would trade for in an arm’s-length transaction, independent of the parent’s acquisition price. This method results in a higher NCI figure at acquisition because it includes the NCI’s share of goodwill, whereas the proportionate method does not. The choice of method affects the goodwill recognised in the consolidated balance sheet: full goodwill method produces a higher goodwill figure, while the partial goodwill method produces a lower one. Once the method is selected and applied at acquisition, it must be applied consistently for that subsidiary going forward. For the purposes of this guide, the worked examples use the Proportionate Share Method, as it is the more widely applied approach in practice.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

Step 1: Identify the Subsidiary’s Net Assets at Acquisition Date

The starting point for any NCI calculation is establishing the fair value of the subsidiary’s identifiable net assets at the date of acquisition. Net assets is simply total assets minus total liabilities — but the critical word here is “fair value.” Under IFRS 3, all identifiable assets and liabilities of the acquired entity must be measured at their fair value on the acquisition date, not at their carrying value in the subsidiary’s own books. This fair value exercise — often called a purchase price allocation or PPA — is where significant adjustments frequently arise. Property that was carried at depreciated historical cost may have a current market value well above book value. Customer relationships, brand names, and patents that were never recognised as assets in the subsidiary’s standalone accounts must be identified and fair-valued. Contingent liabilities that were not recognised in the subsidiary’s books may need to be recognised at fair value in the consolidated statements. Once all these fair value adjustments are made, the resulting net asset figure is the correct base for calculating both NCI and goodwill. It is worth noting that the fair value exercise is typically performed by the finance team with input from external valuers, particularly for significant acquisitions. The output is documented in a purchase price allocation schedule, which becomes the opening balance for the subsidiary in the consolidated accounts and the foundation for all subsequent NCI calculations.

Worked Example:

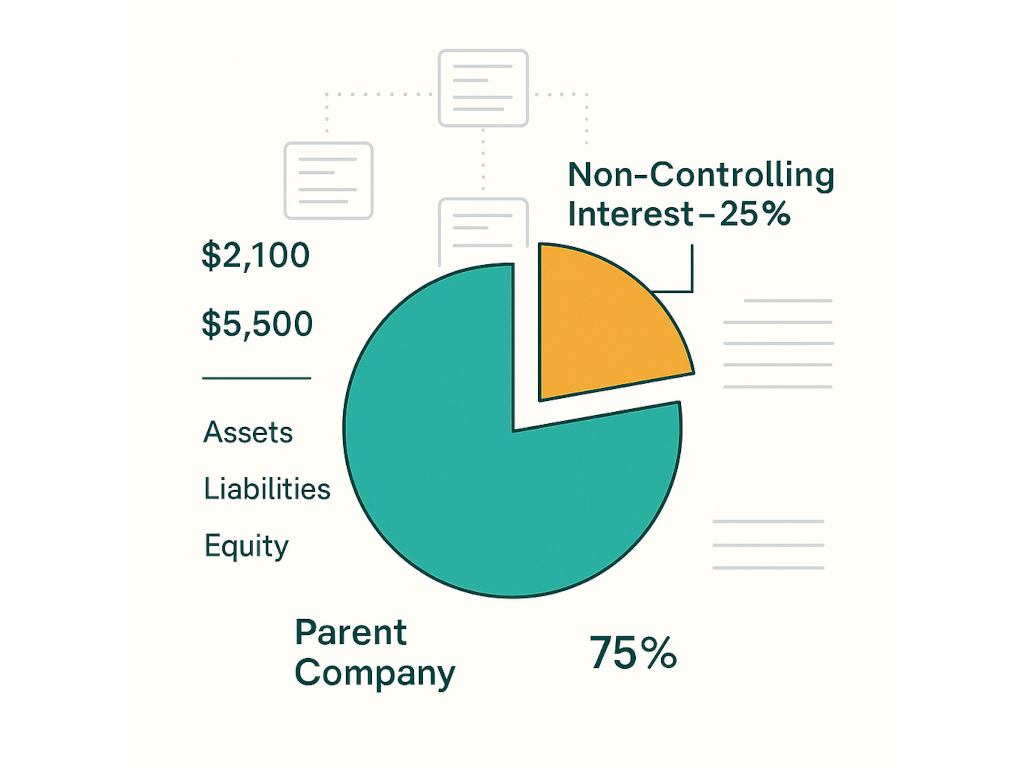

Assume Parent Co acquires 75% of Subsidiary Ltd. At the acquisition date, Subsidiary Ltd’s identifiable net assets at fair value are calculated as:

$000 Property, plant & equipment (at fair value) 4,200 Inventory (at fair value) 800 Trade receivables 600 Cash 400 Total Assets 6,000 Trade payables (500) Borrowings (1,000) Total Liabilities (1,500) Net Assets at Fair Value 4,500

Step 2: Apply the NCI Ownership Percentage

Once the fair value of the subsidiary’s net assets at the acquisition date is established, the NCI at acquisition is simply calculated by multiplying the net assets figure by the non-controlling interest percentage — that is, the percentage of the subsidiary not owned by the parent.

Formula:

NCI at Acquisition = Net Assets at Fair Value × NCI Percentage

This figure represents the non-controlling shareholders’ share of the subsidiary’s net assets on the day the parent took control. It is recognised directly in the equity section of the consolidated balance sheet at the acquisition date and forms the opening NCI balance from which all subsequent movements are tracked. The calculation itself is arithmetically simple, but the inputs — particularly the fair value of net assets — require significant judgment and expertise to get right. An error in the purchase price allocation flows directly into an error in NCI, which then compounds into every subsequent period’s NCI movement calculation. This is why clean, well-documented acquisition accounting is so important: it is not just a compliance exercise but the foundation of accurate group reporting for the entire life of the subsidiary’s membership in the group.

Continuing the Example:

NCI Percentage = 25% (since Parent Co owns 75%)

NCI at Acquisition = $4,500,000 × 25% = $1,125,000

This $1,125,000 is recognised in equity on the consolidated balance sheet as “Non-Controlling Interest” at the acquisition date.

Step 3: Adjust for Post-Acquisition Changes

The acquisition-date NCI figure is just the starting point. In every subsequent reporting period, the NCI balance must be updated to reflect the non-controlling shareholders’ share of movements in the subsidiary’s net assets since the acquisition date. There are three main categories of post-acquisition movement that affect NCI: profit or loss for the period, dividends paid to minority shareholders, and other comprehensive income (OCI) items such as foreign currency translation differences, revaluation surpluses, and actuarial gains or losses on pension schemes. The NCI’s share of the subsidiary’s profit for the period is calculated by multiplying the subsidiary’s post-acquisition profit (after any fair value depreciation adjustments arising from the purchase price allocation) by the NCI percentage. This amount is added to the NCI balance in equity and also presented separately in the consolidated income statement as “Profit attributable to non-controlling interests.” Dividends paid by the subsidiary to its minority shareholders reduce the NCI balance, because they represent a return of equity to those shareholders. OCI attributable to NCI is similarly calculated as the NCI percentage of each OCI item and presented in the consolidated statement of other comprehensive income. The cumulative effect of all these movements, tracked from the acquisition date forward, gives you the NCI balance at any reporting date.

Continuing the Example:

In Year 1 after acquisition, Subsidiary Ltd earns a post-acquisition profit of $600,000 and pays dividends of $100,000 to all shareholders.

$000 NCI at acquisition 1,125 Add: NCI share of profit (25% × $600k) 150 Less: NCI share of dividends (25% × $100k) (25) NCI at End of Year 1 1,250

NCI in the Consolidated Balance Sheet

On the consolidated balance sheet, NCI appears within the equity section — but it is presented separately from the equity attributable to the owners of the parent company. This presentation is mandatory under both IFRS and US GAAP and reflects the fact that while NCI is genuine equity (it represents a real ownership claim on the subsidiary’s net assets), it belongs to shareholders outside the parent group, not to the parent’s own shareholders. A common mistake made by finance teams new to consolidation is to lump NCI together with retained earnings or to present it as a liability. NCI is neither a liability nor part of the parent’s equity — it is a third category, distinctly disclosed, that sits alongside share capital and retained earnings in the equity section of the consolidated balance sheet. The presentation typically looks like this at the equity section level: Share capital (attributable to parent), Retained earnings (attributable to parent), Other reserves (attributable to parent), followed by a clearly labelled row for Non-Controlling Interests. The NCI balance grows each period by the NCI’s share of the subsidiary’s profit and OCI, and shrinks when dividends are paid to minority shareholders or when the parent increases its ownership stake. If a parent acquires additional shares from minority shareholders, the NCI balance decreases and the difference between the consideration paid and the NCI derecognised is recorded as a movement in the parent’s equity — not as goodwill or a gain or loss in the income statement, under IFRS 10.

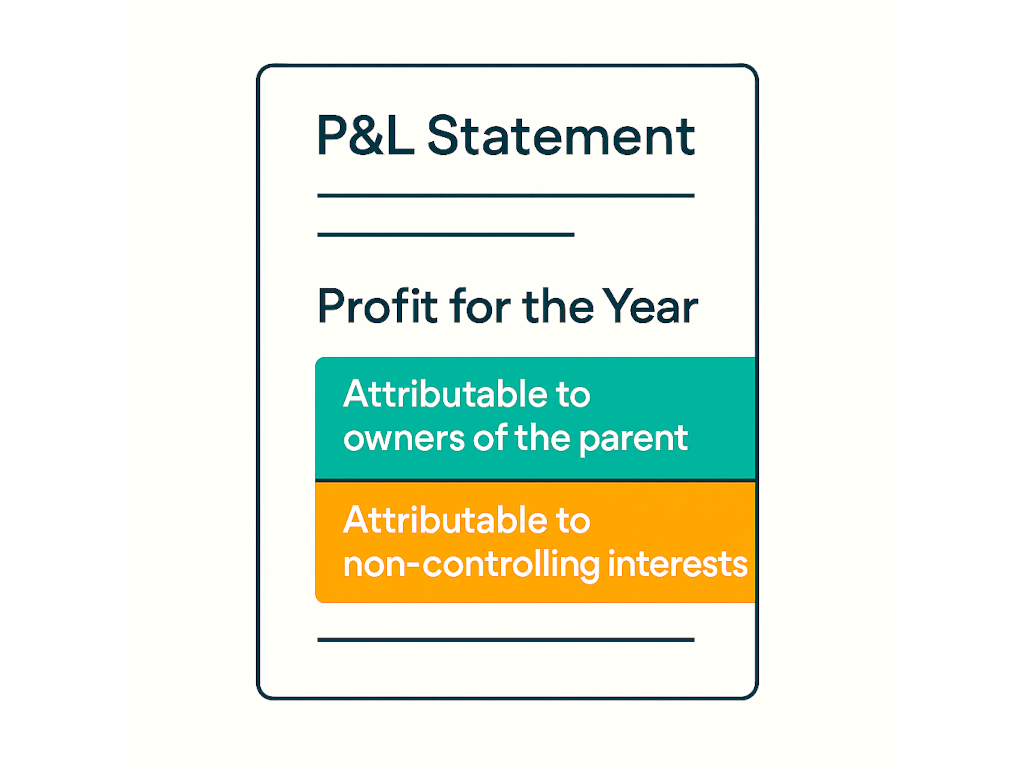

NCI in the Consolidated Income Statement

Just as NCI must be disclosed separately in equity on the balance sheet, the consolidated income statement must also split the total profit for the period between the amount attributable to the parent’s shareholders and the amount attributable to non-controlling interests. This split appears at the bottom of the income statement, after the total “Profit for the period” line, and it is a mandatory disclosure rather than an optional one. The NCI’s share of profit is calculated as its percentage of the subsidiary’s profit after tax for the period — but with one important adjustment: any additional depreciation or amortisation arising from the fair value uplift of assets recognised in the purchase price allocation must be charged against the subsidiary’s profit before the NCI split is applied. This is because the fair value adjustments were made at the group level, not in the subsidiary’s own books, and they affect the economic profit of the subsidiary that is being shared between the parent and the minority shareholders. Forgetting to make these PPA-related adjustments is one of the most common technical errors in NCI calculations — it results in NCI being slightly overstated each period, and the cumulative error can become material over the life of a long-lived acquisition. In addition to the profit split, the statement of other comprehensive income must similarly split each OCI component between the amounts attributable to the parent and to NCI.

How BrizoConsol Calculates NCI Automatically

If the step-by-step process above looks like a lot of work to maintain across every reporting period — it is, when done manually. The traditional approach involves an NCI workbook in Excel, usually maintained separately from the main consolidation model, with its own set of formulas linking to the subsidiary’s trial balance data, tracking fair value depreciation adjustments period by period, and rolling forward the NCI equity balance. It needs to be updated every month-end, checked for broken links every time the trial balance structure changes, and reconciled to the balance sheet and income statement totals manually. A single formula error can cascade into a misstatement across the entire consolidated set. BrizoConsol eliminates all of this. When you set up a subsidiary in BrizoConsol , you simply enter the parent’s ownership percentage — say, 75% — and the platform handles every NCI calculation automatically from that point forward. The NCI balance is calculated and updated in real time as the subsidiary’s trial balance data flows in from the connected accounting software. The NCI share of profit is split and presented automatically in the consolidated income statement. The NCI equity balance rolls forward correctly each period, incorporating profit, dividends, and OCI movements without any manual intervention. There is no separate NCI workbook to maintain, no risk of formula errors, and no reconciliation step at month-end. If the ownership percentage changes — for example, if the parent acquires an additional stake — updating the percentage in BrizoConsol instantly recalculates everything downstream. For groups with multiple subsidiaries at different ownership percentages, BrizoConsol tracks each entity’s NCI independently and aggregates them correctly in the consolidated statements. What would take an experienced finance manager several hours per month to maintain manually is handled by the platform in the background, so the team can focus on reviewing and interpreting the numbers rather than producing them.

Conclusion

Non-Controlling Interest is not a rounding line on the balance sheet — it is a substantive disclosure that reflects the rights of real shareholders with a real economic stake in your subsidiary. Calculating it correctly requires clean acquisition-date fair values, disciplined tracking of post-acquisition profit, dividends, and OCI, and precise presentation in both the balance sheet and the income statement across every reporting period. The mechanics, as this guide has shown, are logical and systematic — but they require consistent attention and are prone to compounding errors when managed in spreadsheets. BrizoConsol was built to remove that risk entirely. By automating NCI calculation from ownership percentage through to consolidated disclosure, it gives finance teams accurate, audit-ready NCI figures every period without the manual workbook. If your group includes partially owned subsidiaries and you are still calculating NCI by hand, it is worth seeing how much time and risk BrizoConsol can take off your plate. Start a free trial at brizoconsol.com.