Intercompany Elimination: The Foundation of Group Consolidation

When one entity in your group sells to another, lends money to another, or charges management fees to another, both entities record the transaction in their own books. Left uncorrected, those internal flows inflate your group accounts — revenue, expenses, assets and liabilities all count twice. Intercompany eliminations are the adjustments that remove those duplicates so your consolidated financials show only what the group earns, spends and owes to the outside world.

If you are consolidating a multi-entity group for the first time — or trying to understand why your consolidated revenue does not match what you expected — this is the place to start. Intercompany eliminations are not an optional refinement. They are the mechanism that makes a consolidated set of accounts meaningful.

Why Eliminations Are Necessary

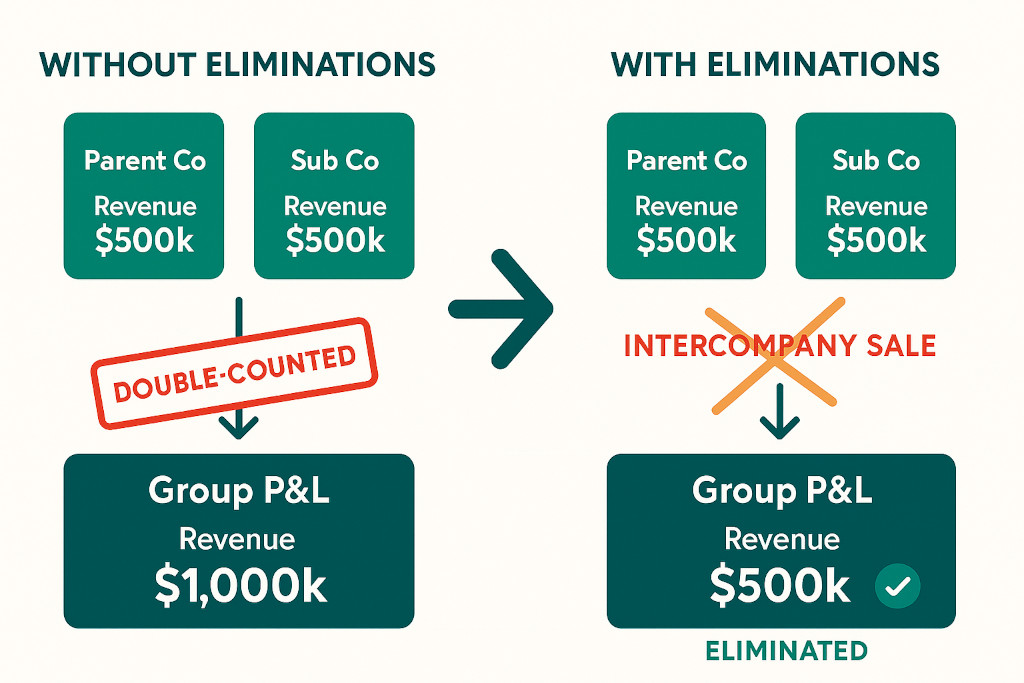

Consider a parent company that owns a trading subsidiary. During the year the subsidiary supplies $400,000 of services to the parent. The subsidiary records $400,000 of revenue. The parent records $400,000 of cost. From a legal-entity perspective, both entries are correct.

Intercompany eliminations without the manual work.

BrizoConsol identifies and eliminates intercompany balances automatically at consolidation.

But from a group perspective, no external revenue was generated. The $400,000 moved from one pocket to another within the same economic unit. If you simply add the two profit-and-loss accounts together, you overstate group revenue by $400,000 and overstate group costs by the same amount. The profit figure stays the same, but the revenue and expense lines are both inflated — and regulators, lenders and investors reading the consolidated accounts will draw the wrong conclusions about the group’s trading scale.

Eliminations correct this by removing both sides of the transaction from the consolidated view: the subsidiary’s intercompany revenue and the parent’s intercompany expense cancel each other out, leaving the group P&L to reflect only transactions with third parties.

The same logic applies to the balance sheet. An intercompany loan appears as a receivable on the lender’s books and a payable on the borrower’s books. In the consolidated balance sheet, both must be removed — otherwise the group appears to have debt it does not actually owe to anyone outside the group, and an asset that is simply money owed to itself.

The Four Main Types of Intercompany Elimination

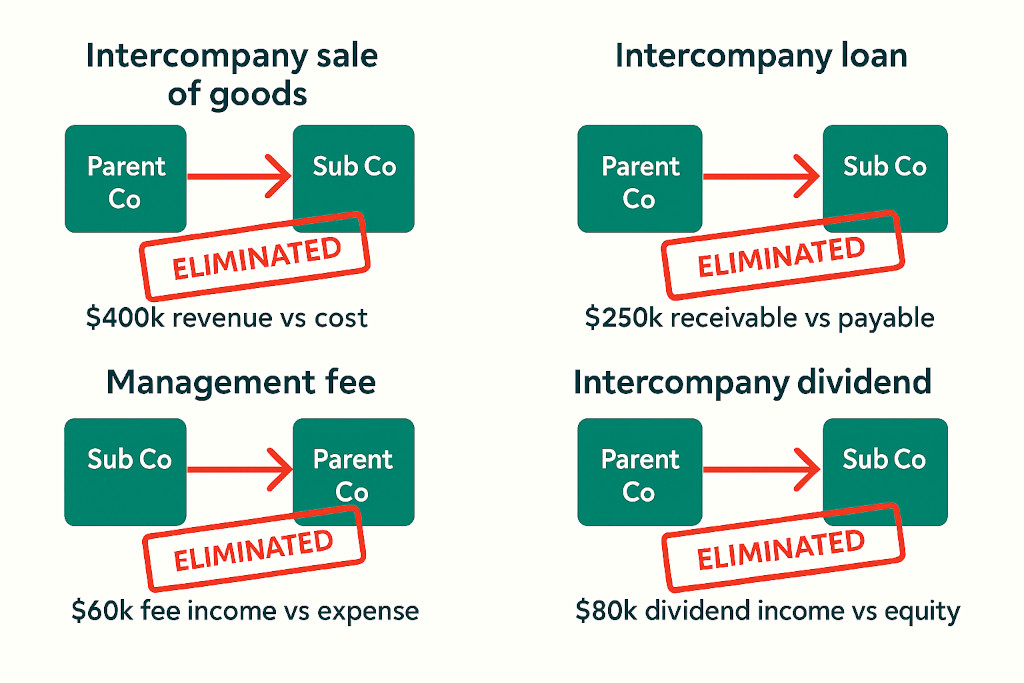

Intercompany sales and purchases

Revenue recorded by the selling entity and the matching cost recorded by the buying entity are both removed. If the goods are still held in inventory, an additional adjustment is needed to eliminate unrealised profit (see below).

Intercompany loans

The loan receivable on the lender’s balance sheet and the matching payable on the borrower’s balance sheet are offset. Any interest income and interest expense flowing between the two entities is also eliminated from the group P&L.

Management fees

When a parent charges subsidiaries for shared services — finance, HR, IT, legal — the fee income recognised by the parent and the management fee expense recorded by each subsidiary must both be removed from the consolidated P&L.

Intercompany dividends

Dividends paid by a subsidiary to its parent are eliminated from consolidated retained earnings. Left in, they would inflate the parent’s investment income and distort equity — the group cannot pay dividends to itself.

Unrealised Profit in Inventory

This is the elimination that most often catches groups off-guard. When entity A sells goods to entity B at a mark-up, and entity B still holds those goods in inventory at the reporting date, the group balance sheet contains an asset that includes a profit no external party has yet confirmed. Under IFRS and US GAAP, that unrealised profit must be eliminated from inventory and from retained earnings until the goods are sold on to a third party. The adjustment is reversed only when the downstream sale occurs.

For groups with significant intercompany trading and slow-moving stock, the unrealised profit balance can be material. It is one of the reasons consolidation software adds more value than a spreadsheet: tracking the in-transit inventory position and reversing prior-period eliminations correctly is error-prone to do manually at speed.

A Worked Example: Two-Entity Group

Imagine a simple group: HoldCo owns 100% of TradeCo. During the year:

- TradeCo sells $400,000 of goods to HoldCo at cost plus 25%. HoldCo has sold all of it on to external customers by year-end.

- HoldCo charges TradeCo a $60,000 management fee for shared finance and HR services.

- HoldCo lent TradeCo $200,000 at 6% p.a. TradeCo paid $12,000 interest during the year.

Before eliminations, the consolidated trial balance contains the following intercompany balances that must be removed:

| Transaction | Remove from P&L / Balance Sheet | Dr | Cr |

|---|---|---|---|

| Intercompany sales | TradeCo revenue ↔ HoldCo cost of sales | $400,000 | $400,000 |

| Management fee | HoldCo fee income ↔ TradeCo management expense | $60,000 | $60,000 |

| Intercompany interest | HoldCo interest income ↔ TradeCo interest expense | $12,000 | $12,000 |

| Intercompany loan | HoldCo receivable ↔ TradeCo payable | $200,000 | $200,000 |

| Total eliminated | $672,000 | $672,000 |

After all four eliminations, the group P&L shows only the revenue earned from external customers and the costs incurred to serve them. The group balance sheet shows only the loan obligation to external lenders — not the internal one. The result is a consolidated view that accurately represents the group as a single economic entity.

Note on goods sold externally by year-end: Because HoldCo has sold all of the goods it bought from TradeCo to external customers by year-end, there is no unrealised profit remaining in inventory at the reporting date — so no additional inventory adjustment is required in this example. Had HoldCo still held $80,000 of TradeCo goods in stock, we would also need to eliminate the 25% mark-up embedded in that inventory value.

Where Eliminations Get Complicated

The two-entity example above is clean: 100% ownership, all goods sold, year-end balances agreed. Real groups add layers of complexity:

Partial ownership and non-controlling interests. When a subsidiary is only partly owned, the intercompany elimination still removes 100% of the intercompany transaction — but the profit or loss adjustment is then split between the group’s share and the NCI share. Getting the NCI allocation right requires tracking the ownership percentage at each consolidation level.

Multi-currency intercompany balances. If the intercompany loan is denominated in a currency different from the group’s presentation currency, exchange differences arise at each reporting date. These need to be tracked separately under IAS 21 — the translation difference on a long-term intercompany loan may qualify to be taken to other comprehensive income rather than the P&L.

Intercompany balance disagreements. In practice, HoldCo’s intercompany receivable and TradeCo’s intercompany payable rarely agree exactly at the reporting date — timing differences from goods in transit or payments in clearing mean the two sides often differ. The consolidation process needs to identify, investigate and resolve those differences before the elimination can be posted cleanly.

Volume at scale. A group with ten or twenty entities can have hundreds of intercompany flows — trading transactions, shared service allocations, recharges, dividends and loans crisscrossing the structure throughout the year. Tracking them all manually, ensuring both sides are recorded consistently, and posting the correct elimination journals is the single biggest source of error and delay in multi-entity month-end close.

⚠️ The most common elimination mistake: Forgetting to reverse the prior-period unrealised profit elimination when the goods are finally sold. Many groups eliminate inventory profit correctly at year-end but fail to reverse it in the following period — understating cost of sales and overstating profit until someone spots the cumulative error.

How BrizoConsol Handles Intercompany Eliminations

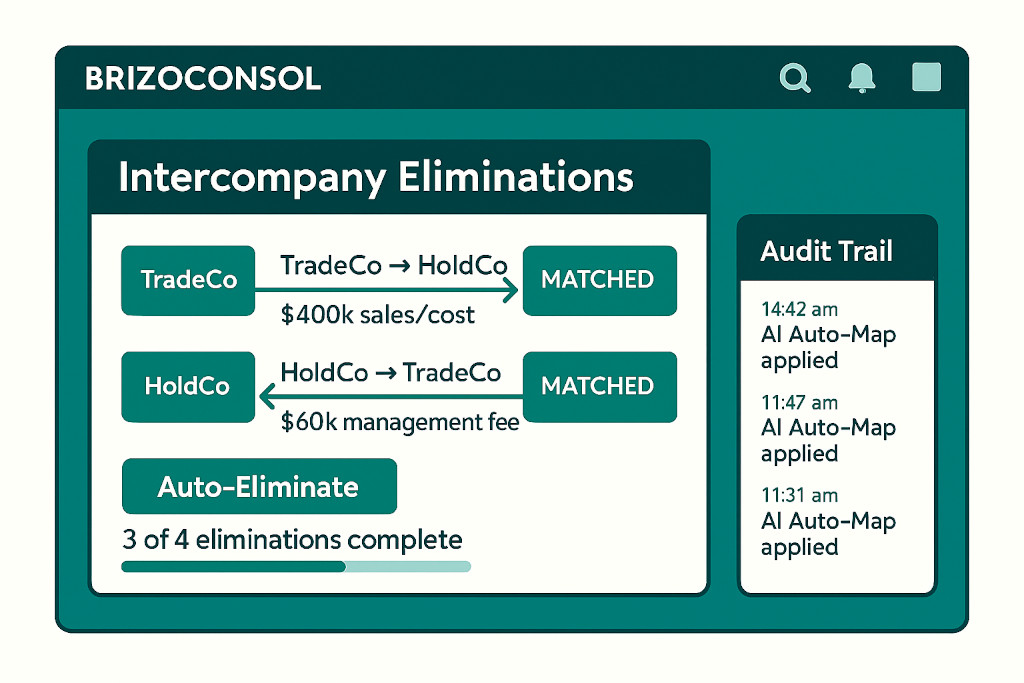

BrizoConsol pulls live data directly from each entity’s accounting system — Xero, QuickBooks, MYOB or Zoho Books — via direct API connection, with no CSV exports required. As each entity’s trial balance is pulled in, BrizoConsol identifies intercompany accounts and matches transactions across the group automatically.

The AI Auto-Map feature handles chart-of-accounts differences between entities: if TradeCo calls the account “Intercompany Revenue” and HoldCo calls it “Group Recharge Income”, Auto-Map recognises the relationship and maps them for elimination purposes. Once mapped, the pairing persists — you set it once and it applies to every subsequent consolidation.

Elimination journals are posted within BrizoConsol’s consolidation layer, leaving the underlying entity accounts untouched. Every journal carries a full audit trail — who posted it, when, and against which source transaction — so the consolidated workpapers are reviewable and sign-off ready without manual reconstruction. For groups producing automated intercompany journals, this replaces the cycle of emailing spreadsheets between entities, reconciling differences, and re-keying adjustments that typically consumes the bulk of close time.

The result is a consolidated P&L and balance sheet where intercompany flows have been removed, NCI is correctly allocated, and currency translation has been applied — ready for board reporting, statutory accounts or group audit without another round of manual adjustments.