The finance director of a mid-sized GP group had a problem she described as “reporting in four different languages.” Her group comprised a holding company, two general practice entities trading under separate Xero files, and a pathology laboratory on QuickBooks. Every month she exported four sets of accounts, pasted them into a master spreadsheet, tried to remember which management fees cancelled which, and hoped nothing had changed in the chart of accounts mappings since the previous close. Board reports arrived ten days late. The figures were accurate, she believed — but she could never be entirely certain.

This is not an unusual situation. Financial consolidation for healthcare groups is, in practice, one of the more demanding consolidation challenges a finance team can face. The sector combines the structural complexity of a holding company group with revenue recognition patterns that differ sharply by entity type, significant intercompany activity, and — in many groups — joint venture arrangements with clinician partners that introduce non-controlling interest calculations at close.

This guide sets out the consolidation mechanics specific to healthcare, works through a realistic example, and explains what a proper group close process should look like.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

Why Healthcare Groups Have Unusually Complex Consolidation Challenges

Healthcare groups share many of the consolidation challenges common to any multi-entity business — differing charts of accounts, intercompany balances that must be eliminated, and the need to produce a single view of group performance. But several features of healthcare make the task harder than it is in most other sectors.

First, revenue recognition varies dramatically by entity. A GP practice may bill on a fee-for-service or bulk-billing basis, with income recognised at the point of service. A specialist clinic may carry significant receivables from private health insurers with a lag of four to eight weeks. A pathology or imaging entity may recognise revenue on dispatch of results. When you roll up these entities into a consolidated P&L, timing differences in revenue create distortions unless the group’s accounting policies are explicitly aligned.

Second, intercompany transactions in healthcare groups are frequent and structurally embedded. Holdings entities routinely charge management fees to operating clinics for administration, IT, billing support, and human resources. Clinics refer patients to group-owned diagnostic entities and are charged for those services. Capital is deployed via intercompany loans. None of these should appear in the consolidated accounts — they represent transactions within the group, not with external parties — but eliminating them correctly requires discipline and a clear audit trail each month.

Third, many healthcare groups include clinical joint ventures. A hospital group may hold a 65% interest in a specialist clinic alongside a clinician partner. A GP network may have acquired 80% of a practice, leaving 20% with the founding doctor. These partial ownership arrangements create non-controlling interest at both the income statement and balance sheet level — adding a layer of calculation that must be performed correctly for every affected entity at each close.

The Most Common Healthcare Group Structures

Healthcare groups take several structural forms, and the consolidation approach differs meaningfully between them. The most common arrangements are as follows.

GP and primary care groups typically consolidate a holding entity with multiple practice entities, each trading as a separate legal entity for liability and licensing reasons. Management fees flow from holding to clinic level. Charts of accounts often differ between practices, particularly where practices were acquired rather than established by the group.

Specialist networks — dermatology, ophthalmology, orthopaedics, and similar roll-up groups — frequently involve partial ownership of individual clinics, where the founding specialist retains a minority stake. NCI is therefore a routine feature of the consolidation, and the group’s effective economic interest in each entity must be tracked precisely.

Allied health and dental groups often operate across multiple jurisdictions and currencies, particularly groups that have expanded into Southeast Asia or the Pacific. Multi-currency translation adds a further layer of complexity: entity financials must be translated to the group’s functional currency before elimination entries are posted, and any resulting translation difference sits in equity as a foreign currency translation reserve.

Aged care and disability service groups carry significant government funding, which can sit in deferred income on the balance sheet until performance obligations are met. The interplay between funding cycles and the group’s financial period means that cut-off judgements at each close require attention.

In each structure, the fundamental consolidation requirement is the same: add 100% of each entity’s revenues, expenses, assets, and liabilities, then remove every transaction, balance, and unrealised gain that relates to activity within the group rather than with the external world.

Intercompany Transactions Healthcare Groups Must Eliminate

The intercompany eliminations required in a healthcare group fall into four main categories.

Management fees. Where a holding entity charges operating entities for shared services, the fee is income in the holding entity and an expense in the clinic. At a group level, the transaction is internal. Both the income and the corresponding expense must be eliminated in full. If the management fee is not eliminated, the consolidated P&L will overstate both revenue and costs — often by hundreds of thousands of pounds or dollars annually in a group of modest size.

Intercompany referral billings. Where a group-owned clinic refers patients to a group-owned diagnostic entity and is invoiced for those services, the diagnostic entity records revenue and the clinic records a cost. Again, this must be eliminated. Any unrealised profit on services not yet completed at period-end — less common in services than in inventory-based businesses, but possible in staged diagnostic workflows — must also be removed.

Intercompany loans and interest. Capital is frequently deployed within a healthcare group via intercompany loans — for example, where the holding entity funds the fit-out of a new clinic. The loan is an asset of the lender and a liability of the borrower; it must be eliminated from the consolidated balance sheet so that no external financing appears to exist. The interest on that loan — income to the lender, expense to the borrower — must be eliminated from the consolidated P&L.

Intercompany equity and investment. The holding entity’s investment in each subsidiary is eliminated against the corresponding share capital and retained earnings of that subsidiary at acquisition date, with any residual goodwill carried on the consolidated balance sheet.

A Worked Example: Consolidating a Three-Entity Healthcare Group

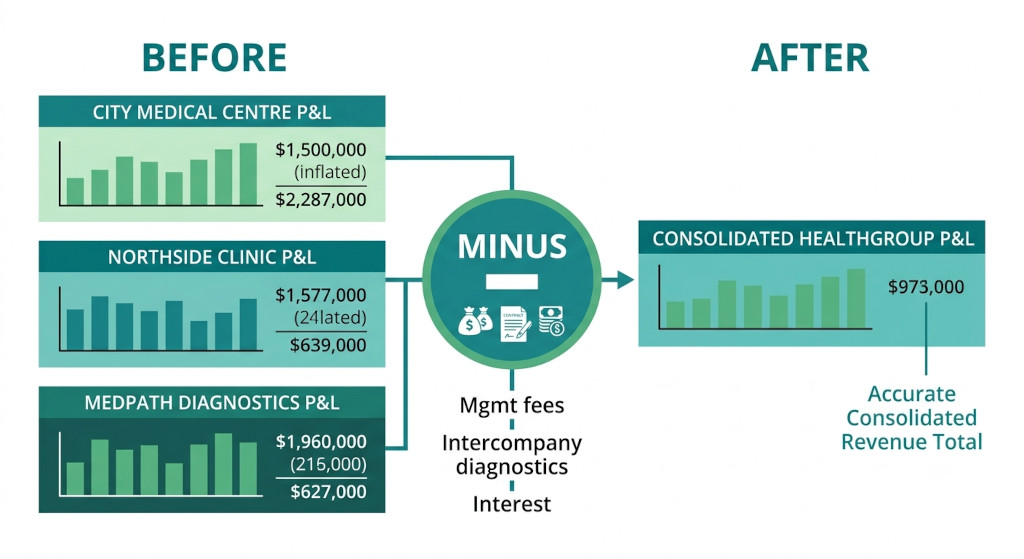

Consider HealthGroup Holdings, a parent entity that owns 100% of City Medical Centre (a GP practice) and MedPath Diagnostics (a pathology lab), and 70% of Northside Specialist Clinic (with a 30% clinician-held NCI). The following table shows the consolidated P&L for the year before and after eliminations.

| Revenue Line | Holdings | City Medical | Northside Spec | MedPath Diag | Combined | Eliminations | Consolidated |

|---|---|---|---|---|---|---|---|

| Patient / clinical fees | — | $2,400K | $1,800K | $720K | $4,920K | — | $4,920K |

| Intercompany — diagnostics (City Medical referrals) | — | — | — | $180K | $180K | ($180K) | — |

| Intercompany — management fees | $204K | — | — | — | $204K | ($204K) | — |

| Intercompany — loan interest | $30K | — | — | — | $30K | ($30K) | — |

| Total revenue | $234K | $2,400K | $1,800K | $900K | $5,334K | ($414K) | $4,920K |

The combined revenue figure of $5,334K would be materially misleading if reported to the board or to lenders without elimination. It is inflated by $414K of intra-group transactions that cancel out when the group is viewed as a single economic entity. After eliminations, consolidated revenue of $4,920K reflects only income generated from external patients and payers — which is the correct basis for assessing the group’s performance.

On the expense side, the corresponding internal charges — the management fee expense in City Medical ($120K) and Northside ($84K), the diagnostic services expense in City Medical ($180K), and the interest expense in MedPath ($30K) — are eliminated in the same entries, so net profit is unaffected by the eliminations. What changes is the presentation: internal flows disappear, and only the group’s true cost base remains visible.

A useful sanity check at each close: the sum of all intercompany income across the group should equal the sum of all intercompany expense. If they do not balance, a posting error or a timing difference in cut-off exists somewhere — and it will surface as an unexplained variance in the consolidated P&L.

Non-Controlling Interest in Healthcare Joint Ventures

Because HealthGroup holds only 70% of Northside Specialist Clinic, it consolidates 100% of Northside’s revenues and expenses (as it controls the entity) but must then allocate 30% of Northside’s net profit to the non-controlling interest. This allocation appears as a deduction below the consolidated profit figure, giving external readers a clear view of how much of the group’s earnings belong to external minority shareholders.

If Northside generates a net profit of $290K for the year, the NCI allocation is $87K (30%). The consolidated income statement would show total group profit of, say, $820K, with a line reading “Profit attributable to non-controlling interests: $87K” and a residual “Profit attributable to owners of the parent: $733K.”

The NCI also appears on the consolidated balance sheet as a separate component of equity — neither a liability nor part of the parent’s owners’ equity. For healthcare groups that are expanding through joint ventures with clinician partners, tracking NCI accurately across multiple partially-owned entities quickly becomes one of the more technically demanding aspects of monthly consolidation. Automating this calculation — rather than maintaining it in a spreadsheet — is one of the clearest quality-of-life improvements a finance team can make.

Setting Up Consolidation for a Healthcare Group

The practical prerequisites for reliable consolidated accounts in a healthcare group are the same as in any multi-entity business, with a few sector-specific emphases.

A standardised group chart of accounts is the foundation. Clinical entities will often use different account codes and categories — one practice may book locum costs under “clinical staff,” another under “contractor fees.” Before consolidation can produce meaningful line items, those local accounts must be mapped to a consistent group taxonomy. This mapping should be documented, version-controlled, and reviewed whenever an entity changes its bookkeeping structure. For more on this process, the guide to designing a common chart of accounts sets out a step-by-step approach applicable to healthcare groups.

A formal intercompany transaction register is equally important. Every management fee, referral billing, loan, and interest charge between group entities should be documented in a register that is reconciled at each close. The register makes it straightforward to verify that intercompany income and expense balances match — catching mismatches before they become audit findings.

Clear cut-off policies aligned across entities are the third prerequisite. If City Medical accrues its management fee liability in June but Holdings recognises the income in July, the consolidated accounts for June will show an unexplained expense with no offsetting income. Healthcare groups with multiple practices and software platforms are particularly prone to this kind of timing mismatch.

What to Look for in Healthcare Group Consolidation Software

Healthcare groups evaluating financial consolidation software should look for several capabilities that are specifically relevant to the sector.

Multi-source connectivity matters because healthcare groups rarely run all entities on the same accounting platform. Xero is common in primary care; QuickBooks appears frequently in practices acquired from owner-operators; MYOB is entrenched in some aged care and allied health operators. The consolidation tool must be able to pull trial balance data from all of these without requiring manual export and reformatting each month.

Automated intercompany elimination is non-negotiable at any meaningful scale. A group with four entities and three categories of intercompany transaction is already managing twelve or more elimination entries each month. At eight entities, the manual effort becomes unsustainable and the error rate climbs. The tool should identify matching intercompany pairs, post eliminations automatically, and flag any imbalances for review.

Non-controlling interest automation is a requirement for any group with partial-ownership structures. The tool should allow each entity’s ownership percentage to be configured, and calculate NCI allocations — both for the income statement and the balance sheet — without manual intervention each period.

Entity-level and group-level reporting in a single platform is the capability that generates the most day-to-day value for healthcare CFOs. Being able to drill from the consolidated group P&L into a specific entity’s figures — and from there into the underlying transactions — makes variance analysis faster and makes it possible to respond to board and management questions in real time rather than over the course of several days.

Medical group consolidation is, ultimately, not materially different from consolidation in any other service-based group. The underlying accounting is the same. What differs is the density and variety of intercompany flows, the frequency of partial ownership arrangements, and the heterogeneity of the accounting platforms in use across entities. A purpose-built consolidation platform removes most of the manual effort from this process and gives healthcare finance teams the clean, reliable group accounts they need to manage and grow the business effectively.

Ready to consolidate your healthcare group in hours, not days?

BrizoConsol connects to Xero, QuickBooks, MYOB, and Zoho Books — eliminating intercompany transactions automatically and producing consolidated accounts your board can rely on. Start Free Trial