If you have ever prepared or reviewed a consolidated balance sheet and found yourself staring at a line in equity labelled Cumulative Translation Adjustment — or Foreign Currency Translation Reserve, or something similar depending on your reporting framework — and wondered exactly where that number comes from, you are not alone. The CTA is one of the most consistently misunderstood items in group financial reporting. Finance professionals who are entirely comfortable with intercompany eliminations, NCI calculations, and deferred tax treatments will often describe the CTA as something that simply appears at the end of the consolidation process and is reconciled after the fact, rather than something they can calculate from first principles with confidence. This guide exists to change that. The Cumulative Translation Adjustment is not mysterious once you understand the mechanics behind it — it is a precise and logical consequence of translating foreign currency financial statements using two different exchange rates for different parts of the balance sheet and income statement. Every component of the CTA can be traced back to a specific translation decision, and every movement in the CTA from one period to the next can be explained and reconciled. This post walks through the calculation step by step, with worked examples, the key formula, an explanation of each component, the most common mistakes that cause CTA balances to be wrong, and how modern consolidation tools handle the calculation automatically.

What Is the Cumulative Translation Adjustment?

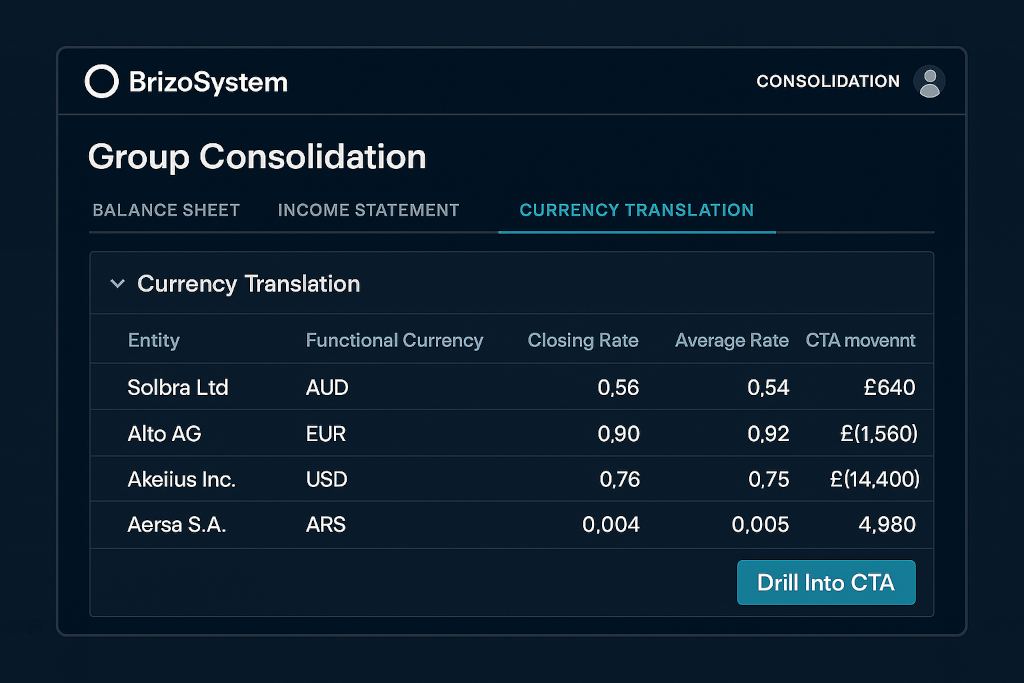

The Cumulative Translation Adjustment is an equity reserve that accumulates the exchange rate differences arising from translating a foreign subsidiary’s financial statements into the parent company’s presentation currency. Under both IFRS (specifically IAS 21) and US GAAP (ASC 830), the translation of a foreign subsidiary’s financial statements into the presentation currency follows a specific set of rules: assets and liabilities on the balance sheet are translated at the closing rate (the spot exchange rate on the last day of the reporting period), income statement items are translated at the average rate for the period (a proxy for the rates in effect when transactions actually occurred), and equity components — such as share capital, retained earnings brought forward, and other equity reserves — are translated at the historical rates in effect when those equity items were originally recognised. Because the closing rate, the average rate, and historical rates are almost never the same, the translated balance sheet does not balance automatically. The difference that is needed to make the translated balance sheet balance is the translation adjustment for the period. Over time, as exchange rates move and more periods are consolidated, these period adjustments accumulate in a reserve on the equity side of the consolidated balance sheet — hence the term Cumulative Translation Adjustment. Critically, the CTA is not a profit or loss item. It sits in Other Comprehensive Income (OCI) and flows into equity rather than through the consolidated income statement. It only gets recycled through the income statement when the foreign subsidiary is partially or fully disposed of — at which point the accumulated CTA related to that entity is released as part of the gain or loss on disposal.

The Translation Rules: Three Rates for Three Things

Before working through the CTA calculation, it is essential to understand which exchange rate applies to which component of the foreign entity’s financial statements. Getting this right is the foundation of the entire calculation. Assets and liabilities — everything on the balance sheet — are translated at the closing rate. This is the spot rate on the reporting date, which means the translated value of every balance sheet item changes every single period as exchange rates move, even if the underlying local currency balances are completely unchanged. Revenue, expenses, and all income statement items are translated at the average rate for the period. Under IAS 21 and ASC 830, the average rate is used as a practical approximation of the rates that were actually in effect when each transaction was recorded, on the grounds that using transaction-date rates for every individual entry is impractical for most businesses. In practice, a monthly average rate is often used for each period’s income statement, with the cumulative weighted average used for the year-to-date totals. Opening equity — share capital, retained earnings brought forward, and any other equity reserves that existed at the beginning of the period — is translated at the historical rate. The historical rate is the closing rate that was in use at the end of the period when those equity balances were first recognised. This means that opening equity balances carry forward their translated values from the prior period and do not get retranslated to the current closing rate. The profit or loss for the current period, which flows from the income statement into retained earnings, uses the average rate, because that is the rate used to translate the income statement. The CTA then serves as the balancing figure that makes the translated equity section reconcile with the translated net assets.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

Step-by-Step: How to Calculate the CTA

The CTA calculation is best understood by working through a complete example. Imagine a UK parent company consolidating an Australian subsidiary. The functional currency of the Australian entity is AUD, and the presentation currency of the group is GBP. At the end of the financial year, the relevant exchange rates are as follows: the closing rate (AUD/GBP at year-end) is 0.52, meaning one Australian dollar translates to 0.52 British pounds. The average rate for the year is 0.50, meaning that on average over the year, one Australian dollar translated to 0.50 British pounds. The opening rate (the closing rate at the end of the prior year) was 0.48. With these rates established, the first step is to translate the income statement at the average rate to arrive at net profit in GBP. If the Australian subsidiary earned AUD 1,000,000 in net profit during the year, that translates to GBP 500,000 at the average rate of 0.50. The second step is to translate the closing balance sheet at the closing rate. If total net assets at year-end are AUD 4,000,000, those translate to GBP 2,080,000 at the closing rate of 0.52. The third step is to translate the opening balance sheet at the opening rate. If opening net assets were AUD 3,500,000, those translate to GBP 1,680,000 at the opening rate of 0.48. Now the CTA for the period can be calculated: it is the closing translated net assets (GBP 2,080,000), minus the opening translated net assets (GBP 1,680,000), minus the translated net profit for the year (GBP 500,000), minus any dividends paid by the subsidiary during the year translated at the rate on the date of payment, plus any capital contributions made during the year translated at the rate on the date of contribution. In this simplified example with no dividends or capital movements, the CTA for the period is GBP 2,080,000 minus GBP 1,680,000 minus GBP 500,000, which gives a CTA movement of negative GBP 100,000. This negative CTA represents the exchange rate loss arising from the fact that the opening net assets and the current year profit were translated at rates lower than the closing rate used for the balance sheet.

The CTA Formula

The formula for the CTA movement in a given period can be expressed clearly once the components described above are understood. The period CTA movement equals the closing net assets translated at the closing rate, minus the opening net assets translated at the opening (prior period closing) rate, minus the net profit for the period translated at the average rate, minus any dividends paid during the period translated at the spot rate on the date of payment, plus any capital injections during the period translated at the spot rate on the date of injection. Written more compactly: CTA Movement = (Closing Net Assets × Closing Rate) minus (Opening Net Assets × Opening Rate) minus (Net Profit × Average Rate) minus (Dividends × Spot Rate at Payment Date) plus (Capital Contributions × Spot Rate at Contribution Date). The Cumulative Translation Adjustment on the balance sheet at any point in time is simply the sum of all period CTA movements since the subsidiary was first consolidated. If the subsidiary was acquired part-way through a financial year, the acquisition date exchange rate is used as the opening rate for that first partial period, and only the post-acquisition net assets and results are included in the calculation. It is important to note that the CTA formula produces a balancing figure — it is the number that makes the equity section of the translated balance sheet equal to the net assets translated at the closing rate. Any error in the underlying translation work will show up as a CTA that does not reconcile to the expected movement, which is why the period-on-period CTA movement is a useful internal check on the accuracy of the consolidation process.

Opening Equity, Retained Earnings, and the Compounding Effect

One of the reasons the CTA confuses finance teams is that it compounds in ways that are not immediately intuitive. Each period’s translation adjustment adds to or subtracts from the cumulative balance, and the opening equity that gets carried forward each period is translated at the rate that was current when those equity items were originally recognised — not at the current closing rate. This means that a subsidiary with a long operating history will carry opening equity translated at a mix of historical rates going back many years, and the CTA serves as the bridge between that historically-translated equity base and the current closing rate used for the balance sheet. The retained earnings component of opening equity is particularly important to understand. The retained earnings balance at the start of any period represents the accumulation of all prior year profits, each of which was originally translated at the average rate applicable to its respective year. Those translated retained earnings carry forward at their translated values without being retranslated to the current closing rate. Only the current year’s profit, newly generated during the period, gets translated at the current average rate and added to retained earnings. The result is that the retained earnings balance in the translated financial statements is not simply the total profit since incorporation translated at a single rate — it is the sum of each year’s profit translated at that year’s average rate, accumulated over the entity’s entire history. When exchange rates have been volatile over that history, the gap between the historically-translated retained earnings and what those retained earnings would be worth at today’s closing rate can be very large, and a significant portion of that gap sits in the CTA.

Common Mistakes When Calculating the CTA

Several errors appear repeatedly in CTA calculations, and understanding them is valuable both for avoiding them and for diagnosing a CTA balance that does not reconcile correctly. The most common mistake is using the wrong rate for dividends. When a subsidiary pays a dividend to the parent during the year, that dividend reduces the subsidiary’s equity and should be translated at the spot rate on the date the dividend was paid — not at the average rate and not at the closing rate. Using the average rate for dividends is technically incorrect and produces a CTA that is slightly wrong, which compounds over time as dividends are paid each year. The second common mistake is failing to use the correct opening rate for the first year of consolidation after an acquisition. When a subsidiary is acquired mid-year, the opening rate for translation purposes is the exchange rate on the acquisition date, not the start of the financial year. Using the wrong opening rate for the acquisition year introduces an error that flows through to every subsequent period’s CTA movement. The third mistake is inconsistency in the average rate used for the income statement. If the income statement is translated at one average rate and the profit figure used in the CTA movement formula is taken from a translation at a slightly different rate — for example, because monthly rates were used for the income statement but a full-year average was used in the CTA formula — a reconciling difference will appear. The fourth mistake is forgetting to separately track the CTA for each individual foreign entity rather than treating all foreign entities as a single pool. Each entity has its own functional currency, its own set of exchange rates, and its own CTA movement, and they must be calculated and tracked separately before being aggregated in the consolidated balance sheet.

Reconciling the CTA Movement: A Practical Checklist

A well-controlled consolidation process includes a period-end CTA reconciliation as a standard step, completed before the consolidated financials are finalised. The reconciliation confirms that the CTA movement calculated from first principles agrees with the CTA balance implied by the translated balance sheet. The starting point is the opening CTA balance, which should agree to the closing CTA balance from the prior period’s consolidation. The next step is to add the current period’s CTA movement, calculated using the formula described above. The result should equal the closing CTA balance on the current period’s translated balance sheet. If it does not, the investigation should follow a structured sequence: first check that the closing rate applied to the balance sheet is correct and consistent with the rate used in the CTA formula; second check that the opening rate used in the formula matches the closing rate from the prior period; third check that dividends have been correctly identified, translated at the spot rate on the payment date, and included in the formula; fourth check that any capital contributions or share issuances during the period have been correctly captured at the spot rate on the date of the transaction; fifth check for any restatements or prior period corrections in the entity’s local accounts that may have changed the opening balance sheet without flowing through the current period income statement. Running this reconciliation every period, rather than only at year-end, dramatically reduces the risk of CTA errors accumulating to a size that is difficult to unwind. It also produces a clear audit trail that external auditors and bank covenant reviewers can follow when they want to understand the source of movements in the equity section of the consolidated balance sheet.

How BrizoConsol Automates the CTA Calculation

Calculating the CTA correctly across a multi-entity group with multiple foreign subsidiaries, potentially each with different functional currencies, is a significant amount of work to do manually in a spreadsheet. The number of exchange rates to track, the number of entity-level movements to calculate, the need to carry forward historically-translated equity balances accurately, and the requirement to reconcile the CTA movement against the translated balance sheet every period all add up to a process that is time-consuming, highly prone to version control errors, and difficult to audit. BrizoConsol eliminates this manual work by handling the multi-currency translation and CTA calculation automatically as part of the consolidation run. When trial balance data is imported from each entity’s accounting software, BrizoConsol applies the appropriate exchange rates — closing rate for balance sheet items, average rate for income statement items, historical rates for equity — and produces the translated financial statements for each entity. The CTA for each foreign entity is calculated automatically and populated in the correct equity reserve in the consolidated balance sheet, with a period-on-period movement that can be drilled into to show the components of the calculation. The system stores each period’s exchange rates and translated balances, which means the opening rate and opening equity values for any future period are always available and accurate, eliminating the risk of rate inconsistencies compounding over time. For finance teams that have historically spent hours each month on manual CTA calculations and reconciliations, BrizoConsol’s automated approach means the CTA is simply correct as part of the standard consolidation output — freeing the finance team to focus on explaining the CTA movement to stakeholders rather than calculating it from scratch.

Conclusion: Understanding CTA Is a Core Consolidation Skill

The Cumulative Translation Adjustment is not a residual or an approximation — it is a precise, calculable number that reflects the economic impact of exchange rate movements on the translated value of foreign subsidiaries over time. Finance professionals who understand how to calculate the CTA from first principles, how to reconcile its movement period on period, and how to identify and correct the most common errors in its calculation are significantly better equipped to manage the complexity of multi-currency group consolidation. The CTA also serves as one of the most useful diagnostic tools in the consolidation process: a CTA movement that does not reconcile to the expected amount is almost always a signal that something else in the translation or consolidation has gone wrong, and catching that signal early saves considerable time and reduces audit risk. For groups managing multiple foreign entities, automating the CTA calculation through a purpose-built consolidation platform is the most reliable way to ensure that the calculation is correct, consistent, and auditable every single period — regardless of how many entities are in the group or how many currencies are in play. Understanding the mechanics remains essential, however, because automation cannot replace the finance team’s ability to review, explain, and take ownership of the numbers that appear in the consolidated financial statements.