How to Use Journal Entries in Group Consolidation (With Examples)

It’s the last Friday of the month. Your Xero instance has the parent’s trial balance. QuickBooks has the US subsidiary’s numbers. The Singapore entity is in MYOB. Between them, there are three intercompany loans, a management fee arrangement, and a shared services recharge — none of which should appear in your consolidated group accounts. Before you can produce a single meaningful group number, you need to post consolidation journal entries to strip all of that out.

Journal entries in accounting are the fundamental building blocks of any general ledger. In a single-entity business, most accountants use them daily without much thought. In a multi-entity group, however, consolidation journal entries are a distinct discipline — they exist solely at the group level, never flow back to the subsidiary ledgers, and must be posted in exactly the right sequence to avoid a consolidated P&L that quietly double-counts millions in intercompany revenue.

This guide explains what consolidation journal entries are, the four main types you will encounter, a worked example with real figures, and the most common mistakes that cause group accounts to go wrong.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

What Are Consolidation Journal Entries?

A consolidation journal entry is a group-level adjustment made during the consolidation process to eliminate intercompany transactions, translate foreign currency balances, account for non-controlling interests (NCI), or reclassify items so that the combined financial statements present the group as a single economic entity.

The critical distinction from ordinary journal entries is scope. An ordinary journal entry posts to a subsidiary ledger and appears in that entity’s standalone accounts. A consolidation journal entry exists only in the consolidation workbook or software — it adjusts the combined trial balance but does not alter the underlying books of any individual company.

“Consolidation journal entries are the layer of accounting that turns a collection of entity trial balances into a single, truthful picture of the group.”

Because these entries sit outside the subsidiary ledgers, they must be recreated every period. A manual consolidation in Excel typically means re-entering dozens of journal entries every month-end. Consolidation platforms such as financial consolidation software automate this step by applying the same elimination rules and currency translation logic each period without re-keying.

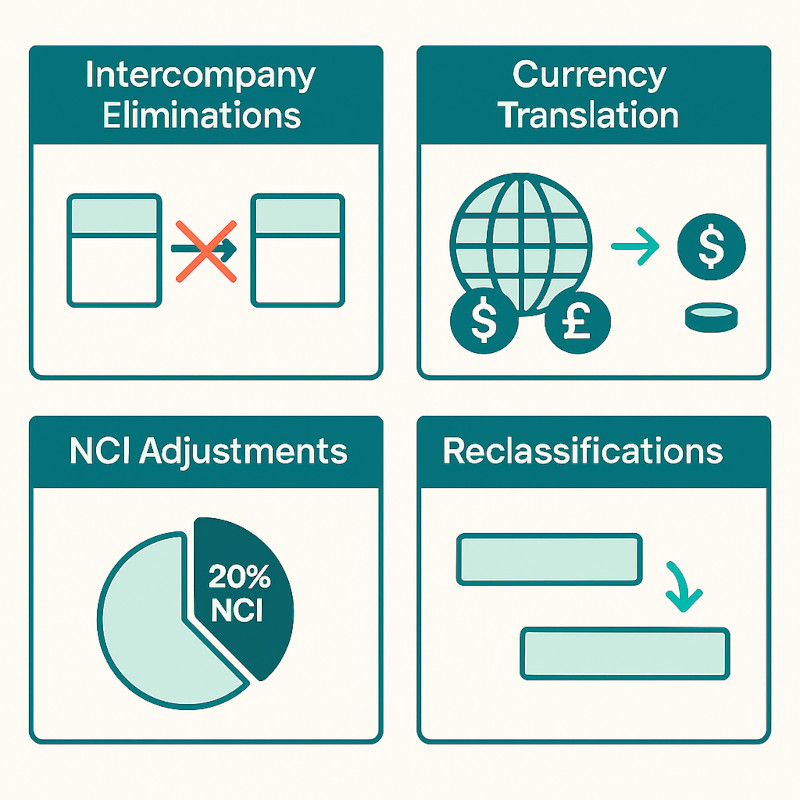

The Four Types of Consolidation Journal Entries

1. Intercompany Elimination Entries

These are the most common consolidation journal entries. When one group entity sells goods or services to another, both the revenue (in the seller) and the cost (in the buyer) exist in the combined trial balance. At group level, this is a transaction with yourself — it must be eliminated entirely. Similarly, any intercompany receivable on one entity’s balance sheet matches an intercompany payable on the other’s: both must be removed so the consolidated balance sheet does not overstate assets and liabilities.

Intercompany loans, interest, management fees, and dividends all require the same treatment. As explained in the practical guide to intercompany eliminations, the rule is simple: if both sides of a transaction sit inside the group boundary, neither side should appear in the consolidated accounts.

2. Currency Translation Adjustment (CTA) Entries

When a group contains subsidiaries that report in foreign currencies, their balance sheets are translated at closing rates and their income statements at average rates. The difference between these two rates — and the movement in those rates since the prior period — produces a currency translation adjustment that is recognised in equity, not in profit or loss under IFRS and US GAAP. A consolidation journal entry is required to record this CTA figure each period.

3. Non-Controlling Interest (NCI) Entries

When a parent owns less than 100% of a subsidiary, the minority shareholders’ share of equity and profit must be carved out and presented separately in the consolidated accounts. Consolidation journal entries allocate the NCI percentage of net assets and net profit to a separate NCI line — ensuring the consolidated P&L and balance sheet are not overstated in favour of the parent’s shareholders.

4. Reclassification and Presentation Adjustments

Not all consolidation journal entries relate to intercompany activity. Some simply standardise presentation across entities with different chart of accounts structures. A subsidiary may classify bank overdrafts as cash and cash equivalents in its standalone accounts; the group policy may require reclassification to current liabilities. These reclassification entries adjust the combined trial balance without changing the group’s net position.

Step-by-Step Example: Posting Consolidation Journal Entries

Consider Meridian Holdings Group — an Australian parent (AUD reporting currency) with two wholly-owned subsidiaries: Meridian UK (GBP) and Meridian NZ (NZD). At 31 May, the following intercompany balances exist:

| Transaction | Amount | In Seller’s Books | In Buyer’s Books |

|---|---|---|---|

| Meridian AU sells goods to Meridian UK | AUD 600,000 | Revenue AUD 600k | COGS AUD 600k (translated) |

| Meridian AU → Meridian NZ management fee | AUD 48,000 | Revenue AUD 48k | Admin Expense AUD 48k (translated) |

| Intercompany loan AU to NZ | AUD 250,000 | IC Receivable AUD 250k | IC Loan Payable AUD 250k (translated) |

| Interest on IC loan (May) | AUD 1,875 | Interest Income AUD 1,875 | Interest Expense AUD 1,875 |

Here are the consolidation journal entries required to eliminate these balances at group level.

JE 1 — Eliminate Intercompany Sales

| Account | Debit | Credit |

|---|---|---|

| Revenue (Meridian AU) | AUD 600,000 | |

| Cost of Goods Sold (Meridian UK — translated) | AUD 600,000 |

Effect: Consolidated revenue and COGS each reduce by AUD 600,000. Group gross profit is unchanged because the margin remains in inventory or in the downstream entity’s cost base.

JE 2 — Eliminate Intercompany Management Fee

| Account | Debit | Credit |

|---|---|---|

| Management Fee Revenue (Meridian AU) | AUD 48,000 | |

| Administration Expense (Meridian NZ — translated) | AUD 48,000 |

Effect: Consolidated revenue and expenses each reduce by AUD 48,000. Group EBIT is unchanged.

JE 3 — Eliminate Intercompany Loan (Balance Sheet)

| Account | Debit | Credit |

|---|---|---|

| Intercompany Loan Payable (Meridian NZ — translated) | AUD 250,000 | |

| Intercompany Receivable (Meridian AU) | AUD 250,000 |

Effect: Consolidated assets and liabilities each reduce by AUD 250,000. Net assets are unchanged.

JE 4 — Eliminate Intercompany Interest

| Account | Debit | Credit |

|---|---|---|

| Interest Income (Meridian AU) | AUD 1,875 | |

| Interest Expense (Meridian NZ — translated) | AUD 1,875 |

Effect: Consolidated net finance income and expense are both reduced by AUD 1,875. No impact on group profit.

Key point: Each of these four journal entries nets to zero — they remove equal and opposite amounts from the combined trial balance. If any consolidation journal entry creates a P&L impact on its own, it is either wrong or relates to an unrealised profit in inventory (a more advanced adjustment covered separately).

Common Mistakes When Posting Consolidation Journal Entries

Mismatched intercompany balances

The most frequent problem at month-end is that the intercompany receivable in Entity A does not match the intercompany payable in Entity B after currency translation. Perhaps Entity A recorded the transaction in USD and Entity B recorded it in AUD at a slightly different rate. When you attempt to eliminate them, you are left with a residual balance that has no obvious home. The fix is to agree intercompany balances before the close — a process often referred to as IC reconciliation — so that both sides agree before any elimination entry is posted.

Forgetting to carry forward equity eliminations

The investment in subsidiaries on the parent’s balance sheet must be eliminated against the subsidiary’s equity at acquisition date in every period, not just once. Many Excel-based consolidations lose this entry when the workbook is rebuilt for a new period, causing the consolidated balance sheet to show both the investment and the subsidiary’s equity — a clear double-count.

Posting in the wrong currency

Consolidation journal entries at group level are posted in the group’s presentation currency. If you are eliminating an intercompany balance that originated in GBP, you must translate it to AUD at the correct rate before posting the elimination entry. Translating at the wrong rate — or omitting translation entirely — will leave a phantom balance that flows into accumulated other comprehensive income or creates an unexplained variance in equity.

Missing NCI entries

If a subsidiary is less than 100% owned, every elimination that involves that subsidiary’s equity must split the impact between the parent’s share and the NCI share. Omitting the NCI entry overstates the parent’s equity in the consolidated balance sheet. For a detailed walkthrough of how to calculate and post NCI, see how to calculate non-controlling interest in financial consolidation.

How BrizoConsol Handles Consolidation Journal Entries Automatically

Every journal entry described above can be handled manually in Excel. For a group with two entities and four intercompany transactions, the workload is manageable — perhaps two or three hours per month. For a group with eight entities, three currencies, management fees flowing in multiple directions, and a minority shareholder in two of the subsidiaries, the manual journal entry count can exceed sixty per close cycle. Errors compound, and a single missed or misstated entry can distort the consolidated P&L by material amounts.

BrizoConsol connects directly to Xero, QuickBooks, MYOB, and Zoho Books via live API — no CSV exports, no manual trial balance imports. When the entities are mapped and the intercompany relationships configured, BrizoConsol identifies all intercompany balances automatically each period and posts the corresponding elimination journal entries in the consolidation engine. Currency translation is applied at the correct closing and average rates, CTA is calculated and recognised in equity, and NCI allocations are computed based on ownership percentages.

Every consolidation journal entry carries a full audit trail — the system records what was eliminated, at what rate, in which period, and what the source balances were. For finance teams facing internal audit reviews or external audit sign-off, this eliminates the need to reconstruct the journal entry logic from a series of Excel tabs.

Virtual Groups in BrizoConsol add a further capability: finance teams can configure segment views — by region, brand, or cost centre — without altering the underlying legal entity structure. This means the same set of consolidation journal entries that produce the statutory group accounts can also be recut automatically to show, for example, the APAC region as a standalone consolidated view.

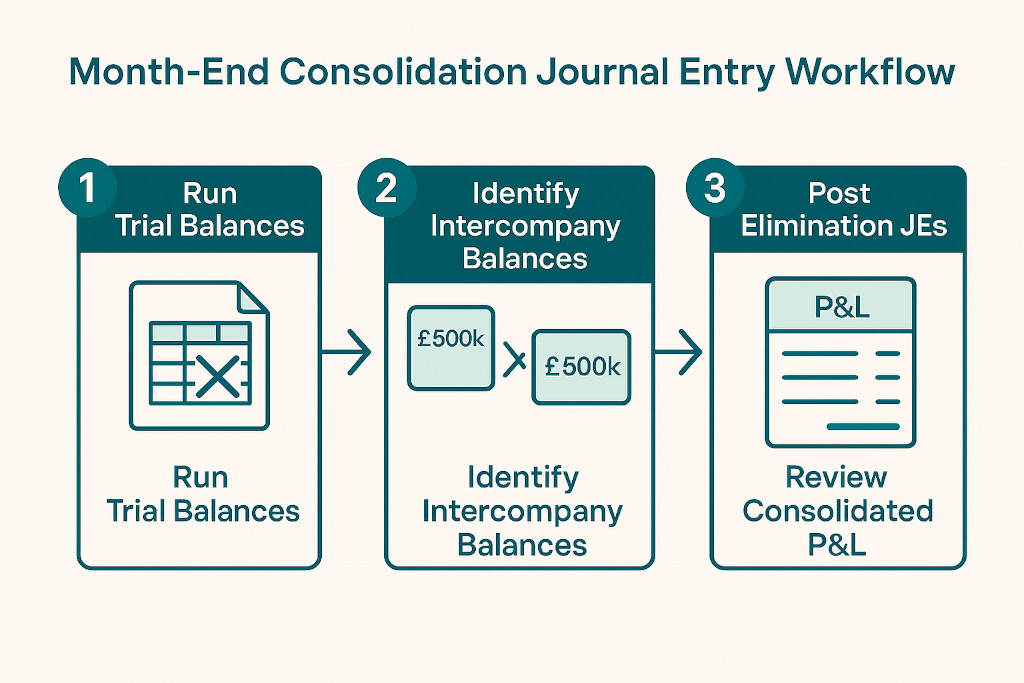

Journal Entry Sequencing Matters

One final point that Excel-based consolidations frequently get wrong is sequencing. Consolidation journal entries must be applied in the correct order to avoid double-eliminating items or missing the interaction between entries. The standard sequence is:

First, eliminate the investment in subsidiaries against opening equity. Second, eliminate intercompany revenue and cost transactions. Third, eliminate intercompany balance sheet positions (receivables, payables, loans). Fourth, eliminate interest, dividends, and management fees. Fifth, calculate and post currency translation adjustments. Sixth, allocate NCI. Finally, review the consolidated trial balance for any residual intercompany balances before closing.

Running this sequence reliably every month — across multiple entities, multiple currencies, and multiple ownership structures — is precisely the kind of repetitive but high-precision work that consolidation software is designed to handle.

Stop re-entering consolidation journal entries every month

BrizoConsol connects directly to your accounting systems and automates eliminations, currency translation, and NCI — with a full audit trail on every entry. Start Free Trial