Intercompany Elimination Journal Entry Examples: A Practical Guide

Intercompany eliminations are the technical core of group consolidation. When one entity in a group sells goods to another, charges management fees, lends money, or pays a dividend to the parent, both entities record the transaction — and both sides must be removed before you can produce consolidated financial statements that reflect only the group’s relationship with the outside world.

Understanding elimination entries in principle is one thing. Knowing exactly what to debit and credit — and why — is another. This guide works through the four most common types of intercompany elimination journal entry with worked examples for each: intercompany sales, intercompany loans, intercompany management fees, and intercompany dividends.

For background on why eliminations are required and how they fit into the overall consolidation process, see our overview of intercompany elimination as the foundation of group consolidation.

Intercompany eliminations without the manual work.

BrizoConsol identifies and eliminates intercompany balances automatically at consolidation.

Why Elimination Entries Are Needed

When you consolidate a group, you are adding together the financial statements of multiple entities and presenting them as if the group were a single economic unit. That means any transaction between entities within the group is, from the group’s perspective, internal — it has not generated revenue, cost, or a balance with the outside world.

Without elimination entries, consolidated figures are overstated in ways that mislead users of the accounts:

- Intercompany sales inflate both group revenue (in the parent) and group cost of sales (in the subsidiary).

- Intercompany loans cause the same amount to appear as both an asset (in the lender) and a liability (in the borrower), inflating the group balance sheet.

- Intercompany management fees inflate both the parent’s fee income and the subsidiary’s expenses.

- Intercompany dividends inflate the parent’s dividend income while reducing the subsidiary’s retained earnings — creating a mismatch that must be removed.

Each elimination entry works by reversing the original accounting treatment on one or both sides, so the net effect on the consolidated statements is nil.

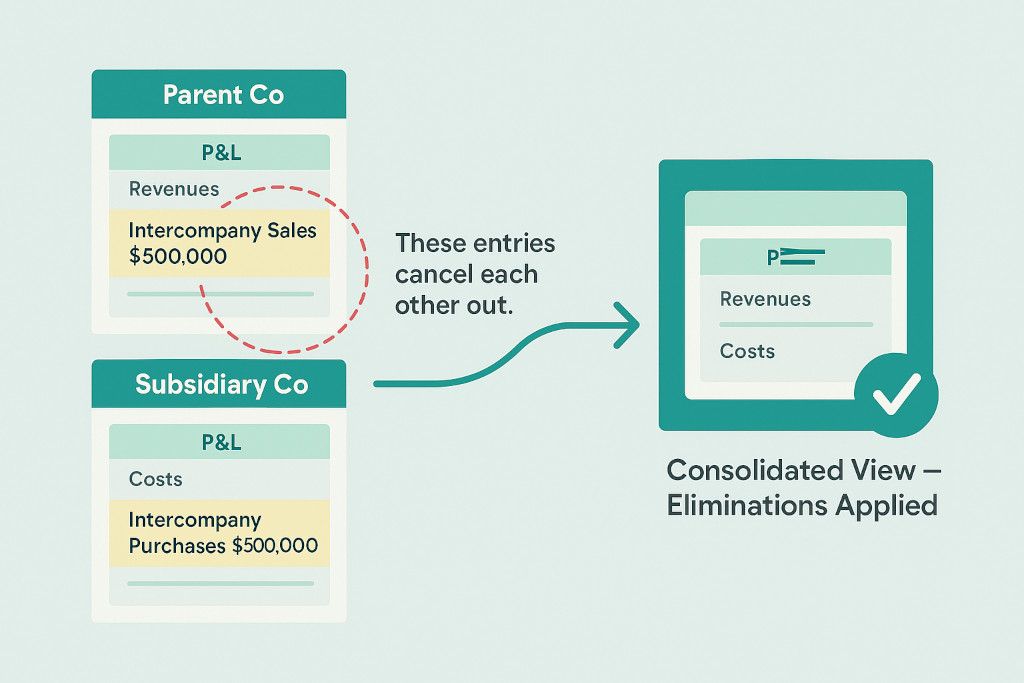

Intercompany Sales Elimination

📋 Scenario: Intercompany Sale of GoodsParent Co sells $500,000 of goods to Subsidiary Co during the year at cost plus 20% margin. Subsidiary Co has sold all the goods on to external customers before year end (so there is no closing stock adjustment required).

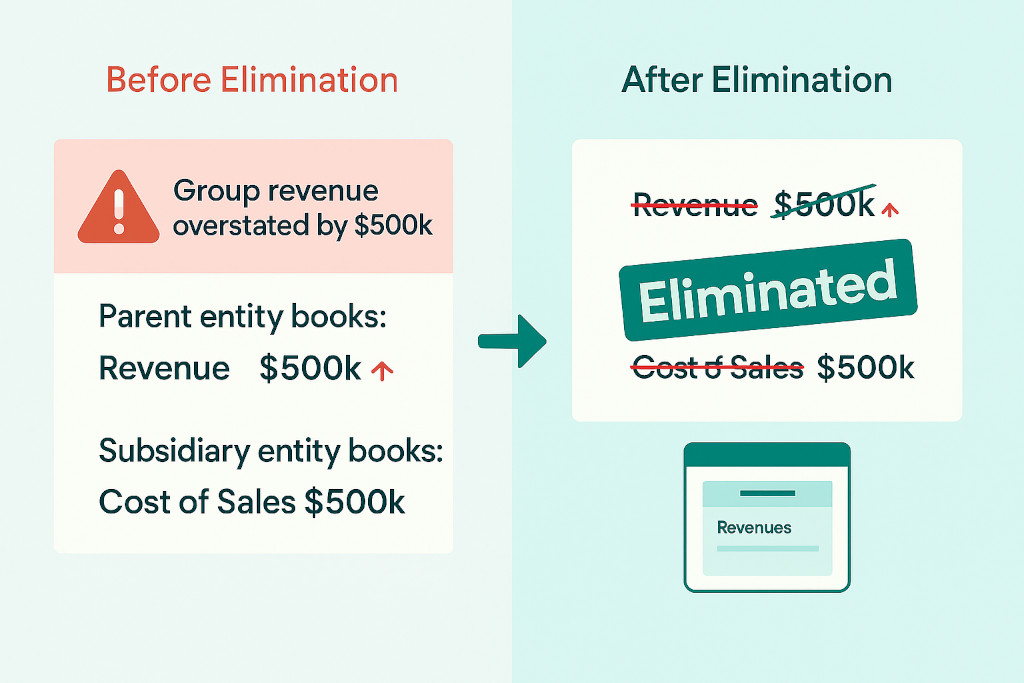

Parent Co books:Dr Intercompany Receivable $500,000 | Cr Revenue (Intercompany) $500,000

Subsidiary Co books:Dr Cost of Sales (Intercompany) $500,000 | Cr Intercompany Payable $500,000

Elimination Entry — Intercompany Revenue and Cost

The intercompany revenue in the parent and the intercompany cost of sales in the subsidiary must be eliminated. Both amounts are equal, so the consolidated income statement reduces by $500,000 on both the revenue line and the cost line, with no effect on group profit.

Journal Entry 1 — Intercompany Sales Elimination (P&L)

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Revenue — Intercompany Sales | $500,000 | Parent Co | |

| Cost of Sales — Intercompany | $500,000 | Subsidiary Co | |

| Total | $500,000 | $500,000 |

Elimination Entry — Intercompany Balances

The intercompany receivable in the parent and the intercompany payable in the subsidiary must also be eliminated from the consolidated balance sheet. If they are not eliminated, the group balance sheet will include a debtor and a creditor that are the same amount — inflating both total assets and total liabilities equally.

Journal Entry 2 — Intercompany Balance Sheet Elimination

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Intercompany Payable (Subsidiary Co) | $500,000 | Subsidiary Co | |

| Intercompany Receivable (Parent Co) | $500,000 | Parent Co | |

| Total | $500,000 | $500,000 |

Note on unrealised profit: If Subsidiary Co had NOT sold all the goods to external customers by year end, the closing stock in Subsidiary Co would include a profit element that has not yet been realised from the group’s perspective. An additional unrealised profit elimination entry would be required — reducing both the closing stock value and group retained earnings by the unrealised margin. The examples above assume full onward sale.

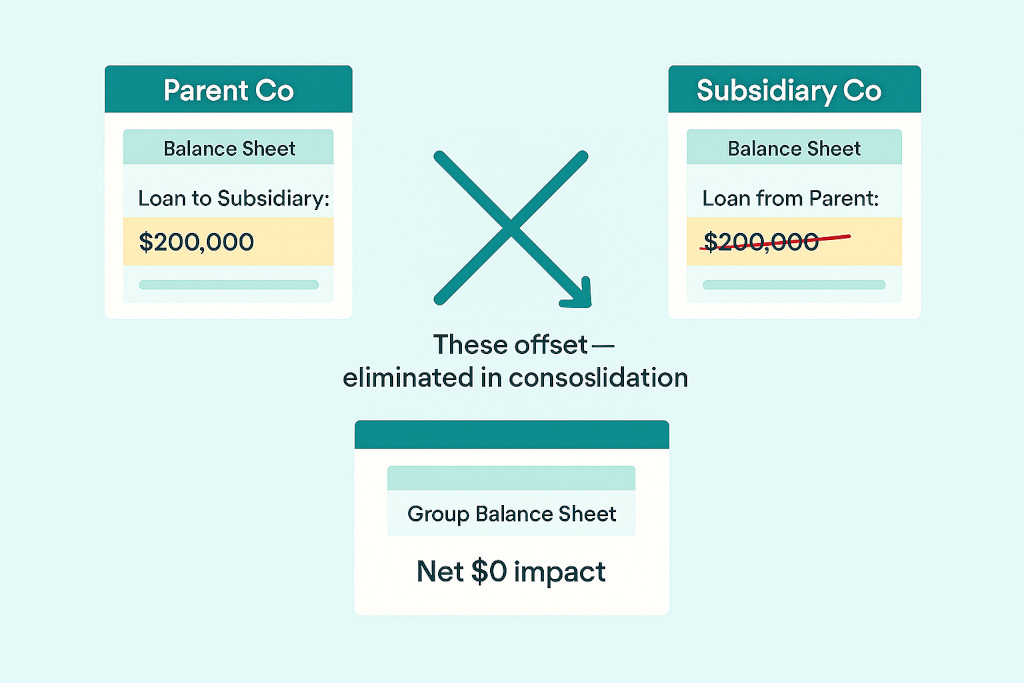

Intercompany Loan Elimination

📋 Scenario: Intercompany LoanParent Co has advanced a $200,000 loan to Subsidiary Co, which is currently outstanding. $12,000 of interest has accrued during the year (6% p.a.) and has been charged by the parent to the subsidiary but not yet paid.

Parent Co books:Loan to Subsidiary $200,000 (asset) | Interest Receivable $12,000 | Interest Income $12,000

Subsidiary Co books:Loan from Parent $200,000 (liability) | Interest Expense $12,000 | Interest Payable $12,000

Elimination Entry — Loan Principal

Journal Entry 3 — Intercompany Loan Elimination

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Loan from Parent (Subsidiary Co) | $200,000 | Subsidiary Co | |

| Loan to Subsidiary (Parent Co) | $200,000 | Parent Co | |

| Total | $200,000 | $200,000 |

Elimination Entry — Accrued Interest

Journal Entry 4 — Intercompany Interest Elimination (P&L)

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Interest Income — Intercompany | $12,000 | Parent Co | |

| Interest Expense — Intercompany | $12,000 | Subsidiary Co | |

| Total | $12,000 | $12,000 |

Journal Entry 5 — Intercompany Interest Accrual Elimination (Balance Sheet)

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Interest Payable — Intercompany (Subsidiary Co) | $12,000 | Subsidiary Co | |

| Interest Receivable — Intercompany (Parent Co) | $12,000 | Parent Co | |

| Total | $12,000 | $12,000 |

Intercompany Management Fee Elimination

📋 Scenario: Management FeeParent Co charges Subsidiary Co a management fee of $60,000 for the year ($5,000/month). The full amount has been paid and is not outstanding at year end.

Parent Co books:Dr Intercompany Receivable / Cash $60,000 | Cr Management Fee Income $60,000

Subsidiary Co books:Dr Management Fee Expense $60,000 | Cr Intercompany Payable / Cash $60,000

Management fee eliminations are among the most common intercompany elimination entries for holding-company structures. The parent charges subsidiaries for shared services — finance, HR, legal, IT — and each subsidiary records the charge as an expense. Without elimination, the group income statement includes both the fee income (inflating revenue) and the fee expense (inflating costs).

Elimination Entry — Management Fee

Journal Entry 6 — Intercompany Management Fee Elimination (P&L)

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Management Fee Income — Intercompany | $60,000 | Parent Co | |

| Management Fee Expense — Intercompany | $60,000 | Subsidiary Co | |

| Total | $60,000 | $60,000 |

Where the fee is accrued but not yet paid at year end, an additional balance sheet entry is required to eliminate the intercompany payable and receivable — identical in structure to Journal Entry 2 above, with the relevant intercompany fee balances substituted.

Intercompany Dividend Elimination

📋 Scenario: Dividend Paid by Subsidiary to ParentSubsidiary Co declares and pays a dividend of $80,000 to Parent Co (its 100% owner) during the year.

Parent Co books:Dr Cash $80,000 | Cr Dividend Income (from Subsidiary) $80,000

Subsidiary Co books:Dr Retained Earnings / Dividends Declared $80,000 | Cr Cash $80,000

Intercompany dividends require particular care. From the group’s perspective, no income has been generated — the parent has simply received cash from an entity it owns, which is an internal movement. If not eliminated, the parent’s dividend income inflates consolidated profit even though the group has not earned anything from an external party.

Elimination Entry — Intercompany Dividend

Journal Entry 7 — Intercompany Dividend Elimination

| Account | Dr | Cr | Entity |

|---|---|---|---|

| Dividend Income — Intercompany | $80,000 | Parent Co | |

| Dividends Declared (Retained Earnings) | $80,000 | Subsidiary Co | |

| Total | $80,000 | $80,000 |

Where a subsidiary is not wholly owned — say Parent Co owns 75% of Subsidiary Co — the dividend elimination covers only the parent’s share (75% × $80,000 = $60,000). The remaining 25% represents the non-controlling interest’s share and is handled separately as part of the NCI allocation. For a full walkthrough of how non-controlling interest is calculated in group consolidation, see our guide on calculating non-controlling interest in financial consolidation.

Summary: All Four Types at a Glance

| Transaction Type | P&L Entries to Eliminate | Balance Sheet Entries to Eliminate | Common Pitfall |

|---|---|---|---|

| Intercompany Sales | Revenue ↓ & Cost of Sales ↓ | Intercompany receivable & payable | Forgetting unrealised profit in closing stock |

| Intercompany Loan | Interest income ↓ & Interest expense ↓ | Loan asset & loan liability; interest accruals | Missing accrued interest that hasn’t been paid |

| Management Fee | Fee income ↓ & Fee expense ↓ | Fee receivable & fee payable (if accrued) | Fees partially accrued, partially paid — splitting timing incorrectly |

| Intercompany Dividend | Dividend income ↓ & Dividends declared ↓ | Dividend payable & dividend receivable (if declared but unpaid) | Including NCI share in the elimination when there are minority interests |

What Happens to These Entries in Your Accounting Software

Most accounting platforms — Xero, QuickBooks, MYOB, Zoho Books — do not produce elimination entries automatically. Each entity runs its own books and records its side of the transaction. When it comes to consolidation, someone needs to gather each entity’s trial balance, identify every intercompany transaction, post the offsetting entries, and verify that intercompany receivables agree with intercompany payables before the elimination can be made.

In practice, this means at least one of two things: a consolidation spreadsheet maintained manually, or a dedicated consolidation platform that automates the process.

BrizoConsol connects directly to Xero, QuickBooks, MYOB, and Zoho Books via API and identifies intercompany transactions using entity relationship definitions and account mappings set up during onboarding. Elimination journal entries are suggested automatically for each period — including the P&L and balance sheet sides — and applied to the consolidated figures without manual calculation. Every elimination is logged with a timestamped audit trail, so auditors can trace every adjustment back to the underlying transactions in each entity’s accounting system.

For a broader overview of how financial consolidation software handles the full range of eliminations, adjustments, and reporting, see our guide on intercompany eliminations: a practical guide for multi-entity groups.

Stop posting elimination entries by hand

BrizoConsol identifies intercompany transactions across your connected entities and generates elimination journal entries automatically — with a full audit trail. Connect directly to Xero, QuickBooks, MYOB, or Zoho Books. No CSV exports.Start Free Trial