US GAAP Consolidation: A Practical Guide to ASC 810 for Multi-Entity Groups

A UK-based professional services group acquired a 60% stake in a US software business and immediately discovered a problem its auditors had not anticipated: the acquisition triggered a US GAAP reporting obligation for the US entity, while the rest of the group continued to report under IFRS. The group’s finance director assumed that consolidation worked the same way under both frameworks — you own more than 50%, you consolidate. What she encountered instead was ASC 810, US GAAP’s consolidation standard, with its Variable Interest Entity model, its specific non-controlling interest presentation rules, and its treatment of potential voting rights that differs in material ways from IFRS 10. The group spent three months working through the differences with its US auditors before the first compliant consolidated accounts were filed.

This article sets out what US GAAP consolidation under ASC 810 actually requires, how it differs from IFRS consolidation, and what finance teams need to know when producing consolidated accounts that comply with US GAAP.

What ASC 810 Covers and Why It Matters

ASC 810 — Consolidation — is the primary US GAAP standard governing when and how one entity must include another in its consolidated financial statements. It applies to any entity preparing financial statements under US GAAP, whether a US-domiciled public company, a US subsidiary of a foreign group, or a private entity with US GAAP reporting obligations to its investors or lenders.

Stop building consolidations in spreadsheets.

BrizoConsol automates multi-entity consolidation — setup in minutes, reports the same day.

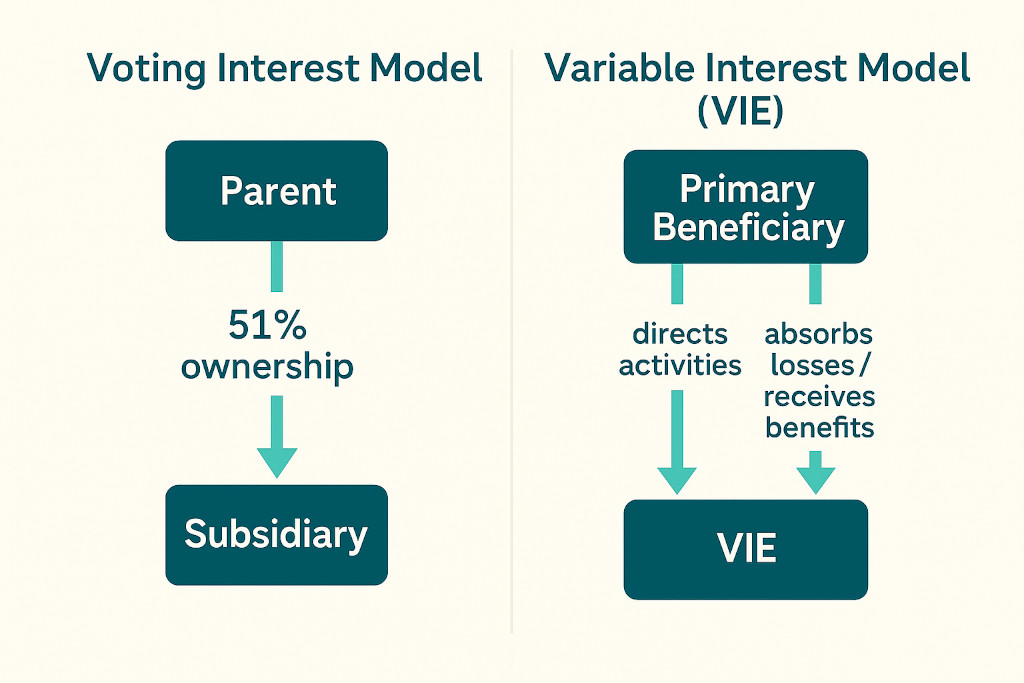

The standard establishes two distinct consolidation models, each with its own assessment criteria:

1. The Voting Interest Entity (VOE) ModelThe default model. An investor consolidates an investee when it holds a majority of the voting rights — typically more than 50% of the outstanding voting shares. This is broadly analogous to the control model under IFRS 10, though the detailed assessment differs.

2. The Variable Interest Entity (VIE) ModelApplied when the investee’s equity at risk is insufficient to finance its activities without additional subordinated financial support — or when equity holders lack the characteristics of a controlling financial interest. The entity with the power to direct the VIE’s activities and the obligation to absorb its losses (the “primary beneficiary”) must consolidate it, regardless of ownership percentage. This model has no direct IFRS equivalent.

The VIE model is one of the most significant practical differences between US GAAP vs IFRS consolidation. Under IFRS 10, control is assessed based on power over relevant activities, exposure to variable returns, and the ability to use power to affect those returns. The VIE model introduces a separate assessment path that can require consolidation where IFRS would not — and vice versa.

The Two Consolidation Models Under ASC 810

The Voting Interest Entity model

Under the VOE model, the consolidation assessment is straightforward in most cases: hold more than 50% of the voting shares, consolidate. The complexity arises in edge cases — where voting rights are non-proportional to economic interest, where kick-out rights held by non-controlling shareholders effectively override the majority holder’s control, or where substantive participating rights give minority shareholders veto power over significant decisions.

For a straightforward parent-subsidiary structure where the parent holds 60% or more of the voting equity and has no unusual governance arrangements, the VOE model produces the same consolidation outcome as IFRS 10. The differences emerge in the detailed accounting: how non-controlling interest is measured, how changes in ownership percentage are handled, and how the consolidation adjustments are presented.

The Variable Interest Entity model

The VIE model was introduced after the Enron collapse, specifically to address structures designed to keep entities off-balance-sheet by engineering ownership percentages below the voting-control threshold. Under ASC 810, an entity is a VIE if any of the following conditions exist:

- The total equity at risk is not sufficient to permit the entity to finance its activities without additional subordinated financial support

- As a group, the holders of equity at risk lack the power to direct the entity’s activities that most significantly affect its economic performance

- The equity holders lack the obligation to absorb the entity’s expected losses

- The equity holders lack the right to receive the entity’s expected residual returns

Where an entity is determined to be a VIE, the primary beneficiary — the entity that has the power to direct the VIE’s most significant activities and the obligation to absorb losses or the right to receive benefits — must consolidate it. Ownership percentage is irrelevant; a 20% holder can be required to consolidate a VIE, while a 51% holder may not be the primary beneficiary.

Practical note: VIE assessments are required on initial involvement with a potential VIE and must be reassessed when facts and circumstances change. Many groups with structured finance arrangements, joint ventures, or special-purpose entities will encounter the VIE model even if their primary consolidation is straightforward.

US GAAP vs IFRS Consolidation: Key Practical Differences

For finance teams that work across both frameworks — or that are consolidating US entities into an IFRS group — the following differences are the most practically significant. For a broader overview of standards comparison, our guide to US GAAP vs IFRS key differences in financial reporting covers the full landscape.

| Area | US GAAP (ASC 810) | IFRS (IFRS 10) |

|---|---|---|

| Primary consolidation model | Voting interest model (majority ownership) + VIE model | Control model (power + variable returns + ability to use power) |

| VIE / special purpose entities | Separate VIE model with primary beneficiary assessment | Assessed under IFRS 10 control model; no separate VIE framework |

| Non-controlling interest (NCI) measurement | Fair value (full goodwill) or proportionate share — accounting policy choice per acquisition | Fair value (full goodwill) or proportionate share — accounting policy choice per acquisition |

| NCI in the balance sheet | Presented within equity, separately from parent’s equity | Presented within equity, separately from parent’s equity |

| Changes in ownership (no loss of control) | Treated as equity transactions — no gain or loss recognised in income | Treated as equity transactions — no gain or loss recognised in income |

| Potential voting rights | Only currently exercisable rights considered | Substantive potential voting rights considered even if not currently exercisable |

| Investment entities exception | Investment entities measure subsidiaries at fair value rather than consolidating | Similar exception under IFRS 10 for investment entities |

The potential voting rights difference is worth highlighting. Under IFRS 10, a 45% holder with warrants that are exercisable in the future may be assessed as having control if those warrants are substantive. Under ASC 810’s voting model, only currently exercisable rights are considered. This can produce different consolidation conclusions for the same structure, depending on which framework applies.

US GAAP Consolidation in Practice: A Worked Example

Consider a straightforward US GAAP consolidation scenario: a US parent company (ParentCo) owns 75% of a US subsidiary (SubCo). The remaining 25% is held by a minority investor. Both entities report in USD under US GAAP. During the period, SubCo sold goods worth $200,000 to ParentCo, which ParentCo has since sold on to third parties.

| Item | ParentCo (USD) | SubCo (USD) | Eliminations (USD) | Consolidated (USD) |

|---|---|---|---|---|

| Revenue — third party | 1,800,000 | 600,000 | — | 2,400,000 |

| Revenue — intercompany | — | 200,000 | (200,000) | — |

| Cost of sales — third party | (1,100,000) | (480,000) | — | (1,580,000) |

| Cost of sales — intercompany purchases | (200,000) | — | 200,000 | — |

| Operating expenses | (320,000) | (180,000) | — | (500,000) |

| Net income before NCI | 180,000 | 140,000 | — | 320,000 |

| Attributable to NCI (25% of SubCo) | — | — | — | (35,000) |

| Attributable to ParentCo shareholders | 285,000 |

Illustrative US GAAP consolidation worksheet. Intercompany sales and purchases eliminated in full; NCI allocated 25% of SubCo net income. Figures simplified for illustration.

Two points from this example are worth emphasising. First, the intercompany sale of $200,000 is eliminated in full from both revenue and cost of sales — the consolidated accounts show only transactions with third parties. Second, the non-controlling interest receives 25% of SubCo’s net income ($140,000 × 25% = $35,000), which is presented separately in the consolidated income statement and deducted before arriving at the income attributable to ParentCo’s shareholders.

The NCI calculation is one of the most commonly mishandled items in group consolidations under both US GAAP and IFRS. Our guide to how to calculate non-controlling interest in financial consolidation covers the mechanics in detail, including the fair value and proportionate share measurement options.

“Under US GAAP, the question ‘should I consolidate this entity?’ has two distinct answers depending on which model applies. Getting the model wrong means either consolidating something you shouldn’t, or leaving something material off the balance sheet.”

How BrizoConsol Supports US GAAP Group Reporting

For groups with US GAAP reporting obligations — whether a US parent consolidating US subsidiaries, or an international group that needs to present subsidiary accounts under US GAAP for investors or lenders — BrizoConsol provides the consolidation infrastructure that handles the mechanical work.

BrizoConsol connects directly to Xero, QuickBooks, MYOB and Zoho Books via live API. For US entities running QuickBooks, the connection is direct — no CSV exports, no manual data assembly. The platform then handles:

- Automatic intercompany eliminations — intercompany sales, purchases, loans, management fees and dividends are identified and eliminated automatically, with a full audit trail on every adjustment. The $200,000 intercompany sale in the example above would be eliminated without manual journal entries.

- Non-controlling interest calculations — NCI is allocated at the correct ownership percentage across the consolidated income statement and balance sheet. Where ownership percentages differ between entities, each is calculated separately.

- US GAAP tagging — BrizoConsol supports IFRS, US GAAP, UK GAAP and Local GAAP tagging at the framework level, allowing groups that report under multiple frameworks to maintain separate presentations without duplicating the underlying data.

- Multi-currency consolidation — for US GAAP groups with foreign subsidiaries, ASC 830 (Foreign Currency Matters) requires translation of foreign-currency statements using the current rate method, with CTA recognised in other comprehensive income. BrizoConsol applies the correct exchange rates and posts the translation adjustment automatically.

For finance teams approaching US GAAP consolidation for the first time — particularly those coming from an IFRS background — the framework difference is primarily in the assessment of what to consolidate, not in the mechanical consolidation process itself. Once the consolidation scope is determined and the entities are connected, the elimination, translation, and NCI calculations work the same way. You can see how financial consolidation software handles that mechanical layer regardless of the reporting framework applied.