Practical Use of Financial Reporting for SMEs: Why It Matters

For many small and mid-size businesses, financial reporting is something that happens to them rather than something they actively use. The accounts get produced once a year for the accountant. The P&L gets reviewed when the bank asks for it. The balance sheet is something the auditors need.

This approach is understandable — running a business is demanding, and finance often feels like a compliance function rather than a decision-making tool. But it is also expensive. SMEs that only look at their financials retrospectively are making pricing decisions, hiring decisions and investment decisions without the information that would make those decisions better.

Financial reporting does not need to be complex to be useful. This article covers what the core reports actually tell you, how SMEs can use them practically, and why the reporting challenge changes when a business grows across multiple entities.

Automate NCI calculations across all your entities.

BrizoConsol handles non-controlling interest automatically — no manual adjustments required.

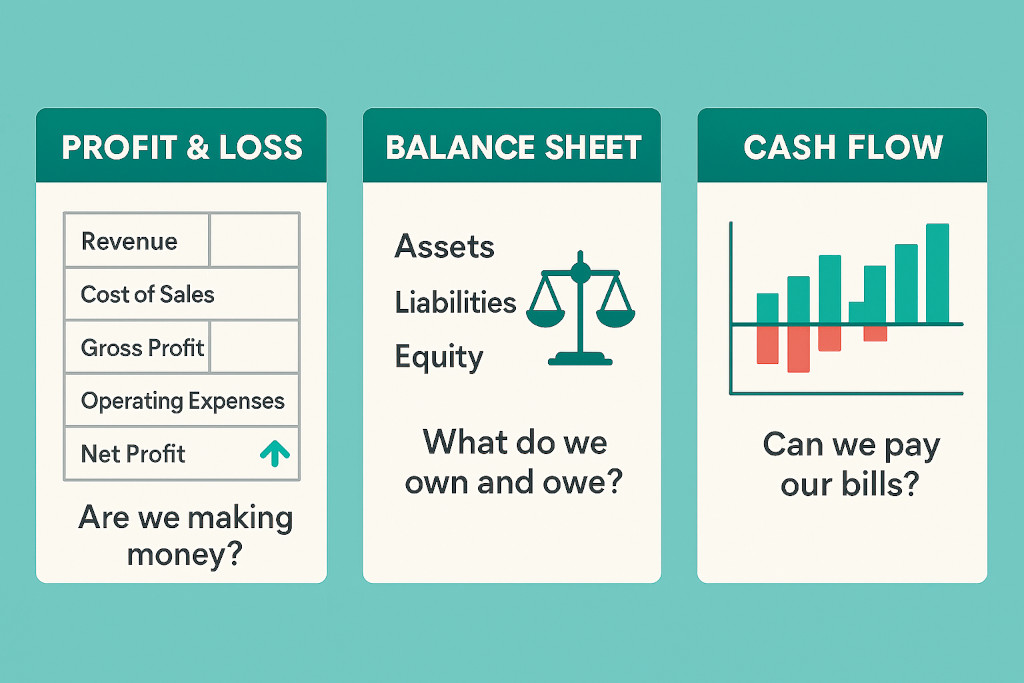

The Three Reports Every SME Actually Needs

Most accounting systems produce dozens of reports. For practical decision-making, three matter most:

Are we making money? – Profit & Loss (P&L)

Shows revenue, costs and profit over a period. The most-read report in most businesses — but most useful when read against a comparison period, not in isolation. A P&L without a prior-month or prior-year column tells you what happened; a P&L with comparisons tells you whether it is better or worse than expected.

What do we own and owe? – Balance Sheet

Shows assets, liabilities and equity at a point in time. Often neglected by SMEs until they need a loan or an investor looks at the business. In practice, the balance sheet is where you spot whether receivables are growing faster than revenue (a collections problem), whether debt is creeping up, and whether the business is building or eroding its equity base.

Can we pay our bills? – Cash Flow Statement

Shows cash in and cash out, separated into operating, investing and financing activities. A profitable business can still run out of cash — it happens when customers pay slowly, when inventory ties up working capital, or when a large investment drains the bank account before the return arrives. The cash flow statement is the report that stops surprises.

Are we on track? – Budget vs Actual

Not a statutory report, but arguably the most practically useful for SMEs with a plan. Comparing actuals against budget each month converts your financial reports from a record of what happened into a conversation about whether the business is on the trajectory you intended — and what to do if it is not.

How SMEs Should Actually Use These Reports

The shift from compliance reporting to decision-support reporting is less about producing different reports and more about asking different questions when you read them. Here is how the same set of reports serves different business decisions:

| Business decision | Report to read | What to look for |

|---|---|---|

| Should we hire another person? | P&L + Cash Flow | Is Gross Profit growing faster than operating expenses? Does the cash position support an additional salary for 6 months while productivity ramps? |

| Can we afford a new office or equipment? | Balance Sheet + Cash Flow | What is the current debt level? What would the cash impact be month by month? Does the asset purchase change the debt ratio in a way that affects existing facilities? |

| Are our prices right? | P&L — Gross Margin | Is Gross Profit Margin holding, compressing or improving over time? If margin is falling while revenue is rising, the business is growing into lower-margin work. |

| Is this business ready to raise finance? | All three reports — 2–3 years of history | Revenue trend, profit consistency, debt-to-equity ratio, working capital position, quality of receivables. Lenders and investors read all three together. |

| Which part of the business is most profitable? | P&L — segmented by product, service or entity | A single combined P&L hides which revenue streams are carrying the others. Segmented reporting shows where the margin actually comes from. |

The monthly review habit: Set aside 30–45 minutes each month to read your P&L, balance sheet and cash position with last month’s figures beside them. Most business-critical signals — margin compression, receivables creeping up, expenses outpacing revenue — show up as gradual trends that are invisible in a single month but obvious across six.

The Mistake Most SMEs Make with Their Financials

The most common reporting mistake in SMEs is not producing bad reports — it is producing accurate reports and not reading them. Accounts that arrive a month after the period closes, reviewed briefly and filed, are not supporting any decisions. By the time they arrive, the month they describe is already history and the business is operating on instinct for the current one.

The second most common mistake is reading reports without context. A net profit of $60,000 this month is good or bad depending on whether the budget was $50,000 or $90,000, whether last month was $40,000 or $80,000, and whether the business employs 5 people or 50. Absolute numbers without comparisons do not tell you anything actionable.

⚠️ Profitable does not mean cash-positive. One of the most dangerous misconceptions in SME finance is treating a strong P&L as evidence of a healthy cash position. Revenue can be recognised before it is collected. Costs can be deferred. A business showing strong net profit while its receivables balloon and its bank balance falls is heading toward a cash crisis — and the P&L alone will not show it. Read the cash flow statement alongside the P&L every month without exception.

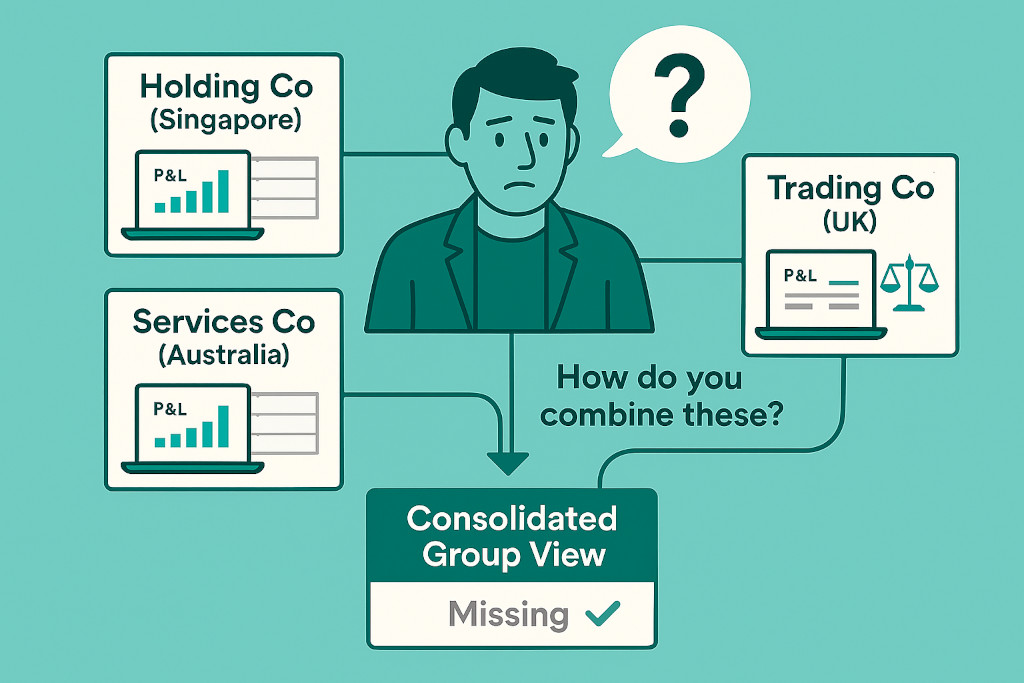

When Financial Reporting Gets Harder: The Multi-Entity Challenge

Many SMEs reach a point where they operate through more than one legal entity. This happens naturally — a holding company and a trading subsidiary, a second entity set up for a new geography, a joint venture, a property-owning company sitting alongside the operating business. Each entity has its own accounts. Each is in its own accounting system. Each is accurate for its own purposes.

But none of them answers the question the business owner or CFO actually needs to answer: how is the whole group doing?

Combining entity-level reports manually — exporting from each system, adjusting for different chart-of-accounts structures, removing intercompany transactions so they do not double-count, translating currencies if entities are in different countries — is the point where financial reporting for SMEs becomes genuinely difficult. Many groups at this stage stop doing it properly, which means the people running the business are making strategic decisions without an accurate picture of the whole.

The consequences are predictable: a director who thinks the group is profitable because the trading entity is profitable, while the holding company is accumulating intercompany debt that the consolidated balance sheet would reveal. Or a cash position that looks comfortable at entity level but is concentrated in one geography while another entity is running short.

What Good Group Reporting Looks Like for an SME

Good group reporting for a multi-entity SME does not require an enterprise finance system or a dedicated consolidation team. It requires three things: a consistent structure for mapping each entity’s accounts to a common view, a reliable way to remove intercompany transactions, and a reporting layer that produces consolidated P&L, balance sheet and cash flow on a monthly basis without a manual rebuild each time.

For SMEs on Xero, QuickBooks, MYOB or Zoho Books, this is exactly the problem that consolidation software solves. Rather than exporting from each system and combining in a spreadsheet, the software connects directly to each entity’s accounting system, maps accounts automatically, handles intercompany eliminations, and produces a consolidated set of reports on a live basis.

The result is that the business owner or CFO has the same monthly reporting discipline for the group that each entity has for itself — and the decision-support value of financial reporting scales with the business rather than being lost at the point where it becomes most needed.

For SMEs running multiple entities on Xero, QuickBooks, MYOB or Zoho Books: BrizoConsol connects directly to each entity’s accounting system and produces consolidated P&L, balance sheet and cash flow reports — with intercompany eliminations applied automatically. No spreadsheet exports, no manual adjustments, no month-end rebuild.